Housing Bust Still Plagues Pre-Retirees

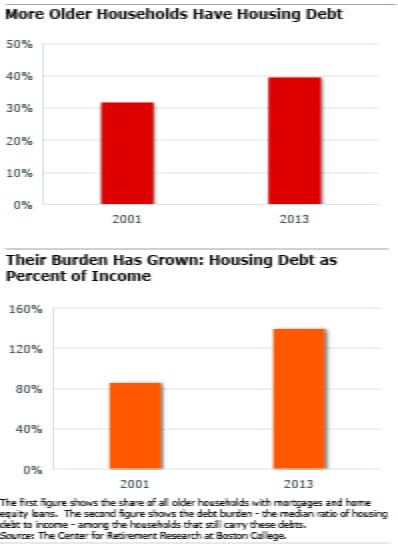

In 2013, almost 40 percent of all households ages 55 and over had not paid off their mortgages, up from 32 percent in 2001. These borrowers were also carrying a lot more housing debt by 2013.

In 2013, almost 40 percent of all households ages 55 and over had not paid off their mortgages, up from 32 percent in 2001. These borrowers were also carrying a lot more housing debt by 2013.

During that time span, the housing boom first encouraged homeowners to borrow against their newfound home equity. Then the 2008 bust hammered house prices from Miami to Seattle, reducing home equity and leaving many people holding relatively large mortgages.

By 2013, these two factors had combined to exacerbate Americans’ poor preparation for retirement, according to a study by the Center for Retirement Research, which supports this blog.

The researchers analyzed the impact of the bursting of the housing bubble on the National Retirement Risk Index (NRRI) through its effect on home equity, the largest store of non-pension wealth for most retirees. The baseline NRRI estimate, using 2013 data from the Federal Reserve’s Survey of Consumer Finances, was that 51.6 percent of working-age households were at risk of having a lower standard of living in retirement. Housing is part of the index, because retirees are assumed to convert their home equity into income by taking out a reverse mortgage.

The 2013 NRRI baseline was adjusted to see what would’ve happened if households had not run up their housing debt during the bubble and if house prices, rather than jump up and then plunge in 2008, had kept up their historic pace of increases since the 1980s. In that case, the researchers found, the share of households at risk would have been 44.2 percent – not 51.6 percent.

In other words, had the housing bubble and subsequent crash not occurred, fewer households would be at risk of having insufficient retirement income.

The middle-class was hardest hit by the crisis, probably because they’re more likely to own homes than people with low incomes and because housing wealth is more important to them than it is to wealthy people.

So what will the 2016 data show in the next Survey of Consumer Finances? In recent years, U.S. house prices have started to really improve, to the benefit of homeowners and retirees. But it’s difficult to predict whether the other factor that has reduced retirement preparedness – more older households with big housing debts – was a boom-time phenomenon or represents the new normal.

As the researchers concluded, “Only time will tell.”

Squared Away writer Kim Blanton invites you to follow us on Twitter @SquaredAwayBC. To stay current on our Squared Away blog, we invite you to join our free email list. You’ll receive just one email each week – with links to the two new posts for that week – when you sign up here.

Comments are closed.

The mortgage deduction is one of the few left to “Pre-Retirees.” It is incorrect to assume that everybody will choose to pay off their mortgage before retirement. Investing more for more years provides the cash flow to carry a low interest rate mortgage.

My dad always felt the way Kevin does, and we argued a lot about his decision to take $100K to invest by using a mortgage refi. Now he is in his 80’s, the “investments” have frittered away, and my parents struggle to pay a heavy mortgage every month. But I am 2 years from retiring now, and am debt free. Tell me, which boat would you rather be in?