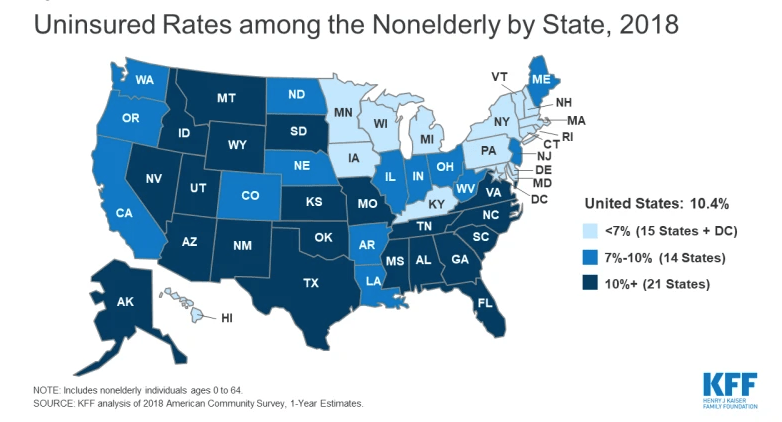

State Uninsured Rates All Over the Map

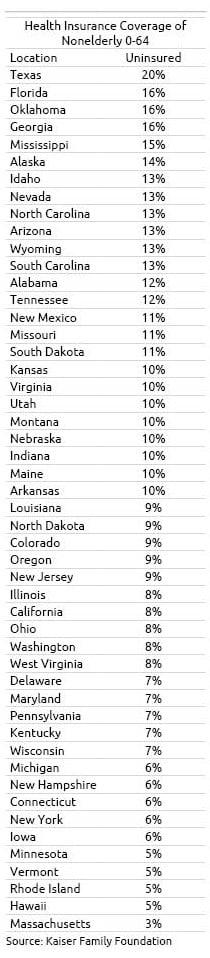

A decade after the passage of the Affordable Care Act, about one out of every five Texans under age 65 still do not have health insurance. Georgia, Oklahoma and Florida are close behind.

The contrast with Hawaii, Minnesota, Michigan, and New Hampshire is stark – only about one in 20 of their residents lacked insurance in 2018, the most recent year of available data, according to the Kaiser Family Foundation’s annual roundup of insurance coverage in the 50 states.

Despite this glaring disparity, the share of Americans lacking coverage has dropped dramatically across the board, including in Texas. Texas’ uninsured rate fell from 26 percent in 2010 to 20% percent in 2018. This translates to nearly 5 million more people with health insurance. (Large populations of undocumented immigrants in states like Texas can push up the uninsured rate.)

States that had fairly broad coverage even prior to the Affordable Care Act’s (ACA) 2010 passage didn’t have as far to fall. For example, Connecticut’s uninsured rate is 6 percent, down from 10 percent in 2010.

One upshot of these two trends is that the disparity between the high- and low-coverage states has shrunk. Certainly, the strong job market gets credit for reducing the ranks of the uninsured. But millions of Americans who don’t have employer insurance have either purchased a policy on the insurance exchanges or gained coverage when their state expanded Medicaid to more low-income residents under the ACA.

For example, just two years after Louisiana’s 2016 Medicaid expansion, the uninsured rate had fallen from 12 percent to 9 percent.

But the initial benefits of the ACA seem to have played out. The U.S. uninsured rate increased slightly, from 10 percent to 10.4 percent between 2016 and 2018.

The share of people who are underinsured is also rising, the Commonwealth Fund found in a recent analysis.

One big source of underinsurance is rising deductibles in employer health insurance. People are counted as under-insured if their out-of-pocket costs, excluding premiums, exceeds 10 percent of their income, making it difficult to pay for medical care out of their own pockets.

Middle-income people who purchase ACA coverage are also underinsured. The deductibles on the standard silver plans are very high – several thousand dollars – in many states. Yet middle-income workers may earn too much to qualify for the generous tax subsidies available to low-income workers under the program.

Squared Away writer Kim Blanton invites you to follow us on Twitter @SquaredAwayBC. To stay current on our blog, please join our free email list. You’ll receive just one email each week – with links to the two new posts for that week – when you sign up here. This blog is supported by the Center for Retirement Research at Boston College.

Comments are closed.

I wonder what happened in 2016 that might have caused the uninsured rate to climb…(spoiler – it was sabotage of the ACA)

Prior to the ACA, about 85 percent of the population had medical coverage. Adding 5 percent came at high cost from disruption of existing benefits, compliance with new rules, complex systems for determining and processing “subsidy” levels etc. It would have been easier and less costly to simply expand eligibility for Medicaid, while avoiding stirring up a hornets nest of resentment and opposition that continues to this day.

To protect against “pre-existing conditions” an amendment to HIPAA would work, specifically by adding “portability” of benefits to the individual marketplace. HIPPA already protected those enrolling in group plans, porting from one group to another and porting from group to individual coverage. What HIPAA left out was portability from individual plan to individual plan. Should the ACA be deemed unconstitutional, Congress can remedy this gap by amending existing law to provide protection for all.

Contrary to popular belief (echoed endlessly by the political class) they were already protecting people against “pre-existing conditions” before the ACA.

States like my home state of Maryland already had laws requiring “guaranteed issue” of coverage for employer groups of all sizes. Maryland also had a HIPAA conversion plan protecting those leaving an employer group plan needing individual coverage.

In many ways, what we had in Maryland was a better system than the raft of problems that followed in the wake of the ACA.

Prior to ACA there were about 50-52 million people with a pre-existing condition that would not have been covered before ACA. Prior to ACA states were allowed to decide whether or not they required health insurance companies to cover pre-existing conditions(13 states did). As per these 2 links.

https://www.thebalance.com/obamacare-pre-existing-conditions-3306072

https://www.kff.org/health-reform/issue-brief/mapping-pre-existing-conditions-across-the-u-s/

2013 US population of 316 million x .85 is an estimated 265.2 million covered. Add the 50 million you cite and you’re right at 316 million. Appears we have no argument here.

However, even if 50-52 million had pre-existing conditions, it doesn’t mean all would be denied access to coverage, thanks to protections under HIPAA.

Title 1 of HIPAA extended “portability” of coverage and protection against “pre-existing conditions” for members of group insurance plans and those “porting” from one group to another. A secondary element required similar protection for those who elected and exhausted COBRA and needed individual market plans. Left out was portability within and between individual market plans, themselves.

This was not a perfect system, requiring plans to issue a “HIPAA Certificate” aka “Certificate of Creditable Coverage” used to satisfy any limits another plan or state may impose on pre-existing conditions. But again, this problem could be cured by amendment to HIPAA to extend it’s protections to all plans; the ACA wasn’t the only way to do so.

HIPAA was passed in 1996 under Clinton and stemmed from Hilary Clinton’s efforts on behalf of healthcare reform. It also created today’s privacy rules and laid the groundwork for electronic record keeping we now take for granted. Likewise, should the ACA be repealed, many ACA provisions will find their way into whatever replaces it. Even Republicans now voice support for pre-existing condition protections.

https://en.wikipedia.org/wiki/Health_Insurance_Portability_and_Accountability_Act#Title_I:_Health_Care_Access,_Portability,_and_Renewability

According to Kaiser, re ACA, the uninsured rate was higher than 15%.

http://files.kff.org/attachment/Issue-Brief-Key-Facts-about-the-Uninsured-Population