Aussie Employer Mandate Fuels Saving

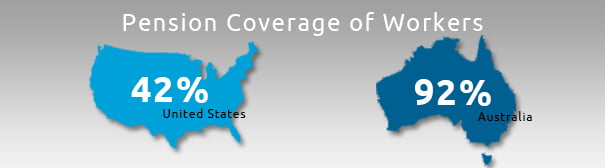

Consider this: 92 percent of Australian workers have 401(k)-style plans, while less than half of Americans have any kind of pension coverage on their current job.

This yawning disparity exists, because the Australian government requires employers to contribute 9 percent of each worker’s earnings to a personal account, which participants invest much like a 401(k). Under reforms to Australia’s system, employer contributions will rise gradually until 2020 – to 12 percent.

Even though Aussie employers are mandated to make the contributions, economists argue, the money ultimately comes from workers – through lower wages. But U.S. workers, left on their own, have proved to be poor savers, and the fact remains that putting the onus on employers to ensure that retirees have something in savings is working better than our catch-as-catch-can system.

“Australia has been extremely effective in achieving key goals of any retirement income system,” concluded a new report by the Center for Retirement Research, which supports this blog.

In numerous comparisons of pension coverage in industrialized countries, Australia ranks high. An October study by Mercer ranked it No. 3 worldwide and the United States No. 9. [Denmark came out on top.] A more recent index, compiled by a Boston money management firm, put the United States at No. 19 out of 20 – Australia was No. 11.

Australia’s system is hardly perfect. Since its federal pension program is means-tested, Aussies can game the system by retiring in their 50s and living off of their retirement savings so they receive a bigger federal pension at 65. And Australia’s 401(k)-style system is plagued with the same issues that impact U.S. employees: a poor understanding of the intricacies of investing.

Australians are permitted to contribute to their employer-based accounts, known as Superannuation Funds, but only 20 percent do, according to the Center’s report. It may appear that Australians are also poor savers, but that’s not the way to think about it. Saving is not as critical for them as it is for Americans, since the employer mandate drives asset accumulation.

Evidence the mandate works can be found in the growth of Australians’ total retirement assets. Asset growth, as a percentage of Australia’s gross domestic product, has surged 46 percent over the past decade, compared with 29 percent for the United States.

A true comparison between the U.S. and Australian retirement systems requires a more complete picture. For instance, Australia’s federal Age Pension differs from Social Security, because the benefits are concentrated among low- and middle-income retirees – some wealthy Australians do not receive any Age Pension. Social Security has a progressive benefit structure too, but all Americans who pay in will receive a monthly benefit check when they retire.

Australia’s success raises this question about U.S. pension reform: Would it be easier for Congress to overcome the corporate lobby and pass an employer mandate or put the mandate on individual employees, many of whom who don’t like being told what to do?