Census Tries to Fix Underreporting in Current Population Survey

Alicia H. Munnell is a columnist for MarketWatch and senior advisor of the Center for Retirement Research at Boston College.

Redesign does not dramatically alter overall picture, but collecting asset data could.

Some experts claim that retirees are better off financially than many think, partly because most retirement income from 401(k) plans and Individual Retirement Accounts (IRAs) is not captured in the Census Bureau’s widely-used Current Population Survey (CPS), Annual Social and Economic Supplement. In the extreme, the Internal Revenue Service reported about $229 billion of defined contribution income in 2012, while the CPS reported $18 billion. Such an enormous discrepancy undermines confidence in the survey. Because low-and middle-income households have little in 401(k)/IRA assets, the under-reporting is minimal for these groups; the main problem occurs in the upper quintiles.

Census has responded by testing a redesign to certain income questions in the 2014 CPS, retaining the old methodology for 60 percent of participants and introducing the new procedures for the rest.

Note that reported income from retirement accounts can fall short of potential for two reasons. First, individuals may not withdraw the money available to them. In fact, studies show that most retirees do not withdraw money until their early 70s when they become subject to the IRS’ required minimum distribution rules. Second, the income that individuals actually do withdraw may not be captured by the survey. Census efforts have focused on the second problem.

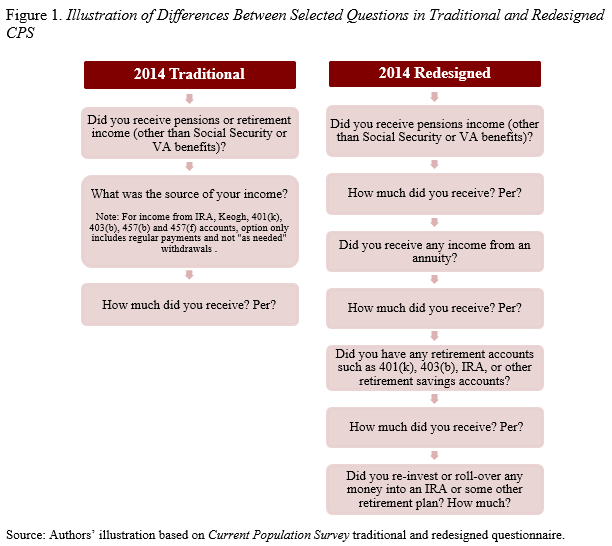

The redesign asks about pension and retirement income from retirement accounts separately, whereas the old procedure combines questions about receipt of pension and retirement income. The redesign also asks about withdrawals and distributions from 401(k) and other retirement accounts that are not limited to “regular income.” In addition, respondents over 70 are instructed to include any “distributions [they] have been required to take” and follow-up questions on whether withdrawals were rolled over or reinvested help exclude rollovers from income calculations. (For details, see Figure 1 below for a somewhat simplified explanation.)

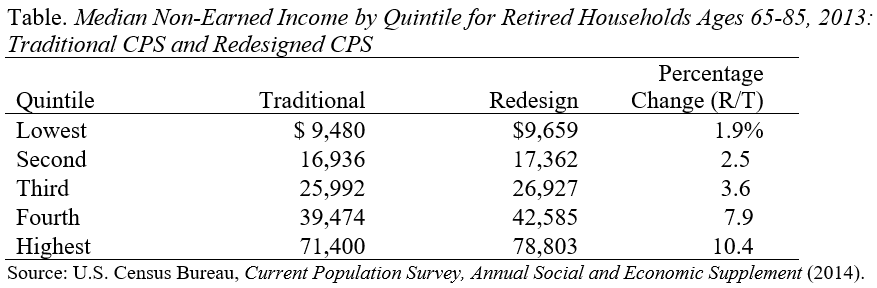

The redesign resulted in higher levels of retirement income – a 1.9 to 3.6 percent increase for the bottom three quintiles and a 7.9 to 10.4 percent increase for the top two quintiles (see Table). The new version of the survey is undoubtedly more accurate. And while the redesign significantly increases income in the top two quintiles, it does not change the basic picture for the typical household.

The 2015 CPS adopted the redesign for all respondents. The redesign, however, still focuses only on income and asks about assets in 401(k) retirement accounts only if respondents do not know how much interest or dividend income they receive from these accounts. Thus, the questions do not try to address “potential” income. A question about assets in 401(k)/IRA plans seems much easier to answer than one targeting income. Having asset data would also make it possible to estimate “potential” defined contribution income, which may become an increasingly relevant metric if households fail to draw down their accumulations until the required minimum distribution rules kick in.