Home Equity Rises. Reverse Mortgages Don’t

The housing market has shrugged off the pandemic, and home prices are rising sharply due to historically low interest rates. The market crash more than a decade ago is a distant memory.

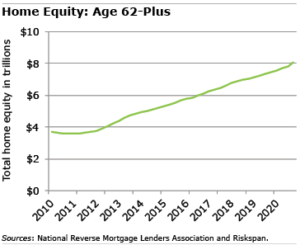

The total value of the equity in older Americans’ homes has doubled since 2010, hitting $8.05 trillion at the end of last year. The irony is that federally insured reverse mortgages, which allow a long-time homeowner to cash in on tens of thousands of dollars of equity, aren’t very popular.

The total value of the equity in older Americans’ homes has doubled since 2010, hitting $8.05 trillion at the end of last year. The irony is that federally insured reverse mortgages, which allow a long-time homeowner to cash in on tens of thousands of dollars of equity, aren’t very popular.

Last year, only 42,000 Home Equity Conversion Mortgages (HECMs) were sold – half as many as in 2010 – according to the U.S. Department of Housing and Urban Development (HUD).

One reason HECM reverse mortgages haven’t caught on, as the Consumer Financial Protection Bureau notes, is that they might not be suitable to homeowners who eventually sell their house. As the loans accrue interest, the “balance is likely to grow faster than their home values will appreciate,” the agency said.

But most retired homeowners never move, and HECMs are one option for people who are short on income. “We accept it as ‘normal’ to spend-down 401(k) funds, yet somehow home equity is sacrosanct,” said Dave Gardner, a former mortgage broker who sometimes handled reverse mortgages. Retirees, he said, should consider this question: “Could you achieve a better result and extend the lifespan of your nest egg with a reverse mortgage?”

To qualify for the loans, borrowers must be at least 62. They can take the reverse mortgage proceeds in the form of a lump sum, line of credit, or monthly payments – or some combination of these.

Curious homeowners can check out the federal government’s new pamphlet, which explains the basics of reverse mortgages. It’s aimed at people who already have the loans but is just as useful for people who are curious about using one themselves.

Before proceeding with any complex financial transaction, however, it’s critical to do due diligence. A reverse mortgage is no different. One protection the federal government has built into HECMs is a requirement that prospective borrowers consult a HUD-approved financial counselor.

Ask the counselor and lender enough questions to have a clear understanding of how the loans work and what the risks are. It’s also important to look for a reputable lender – just as you did for your traditional mortgage.

The amount of equity that can be borrowed is determined by a government formula. HECMs, which are more expensive than traditional mortgages, carry a few different fees: an origination fee for the lender, which is capped at $6,000; upfront and monthly insurance premiums; and the same appraisal and closing costs required for regular mortgages.

But home equity is one of the largest assets retirees own. If you’re struggling to cover your retirement expenses, a reverse mortgage is something to consider.

Squared Away writer Kim Blanton invites you to follow us on Twitter @SquaredAwayBC. To stay current on our blog, please join our free email list. You’ll receive just one email each week – with links to the two new posts for that week – when you sign up here. This blog is supported by the Center for Retirement Research at Boston College.

Comments are closed.

Interesting article. I would be cautious about using 2010 as the date for comparison purposes. Having just come out of the Great Recession at the time, with home valuations not fully recovered, using 2010 as a starting date sets those home valuations at an artificially low (and probably deceptively low) valuation. We recently received our property revaluation (that our county does every three years). Our property valuation has increased by 30% in the past decade. (Using the 2007 valuation as the comparison date however, our property valuation has increased by only 20%. Just a thought…..)

It’s not the home equity that is sacrosanct, it’s the home that is sacrosanct. (The only time I recall hearing my parents “squabble” was when my dad wanted to do this. I recall my mom refusing to sign-off the paperwork & saying, “this is our home, not an investment to borrow against!” That must have made an impact on me. Even today, I don’t include our home valuation in our net worth; yes, the home is sacrosanct.)

This is another financial transaction that does require substantial due diligence. I’m curious about the requirement to consult a HUD-approved financial counselor. If the counselor believes that the client doesn’t understand the reverse mortgage, does the counselor have the authority to disallow the transaction? Or is this consultation simply checking off a box?

Another issue are those fees —> origination fee, upfront premium, monthly premiums, appraisal costs, closing costs, and probably more. Just to borrow against your own home? There must be better, less expensive alternatives.

I think the more people look into this the more they will see the benefits. Your house is considered “wealth” yet to be an asset in my mind, you need access.

Desires to not out live assets, looming & rising healthcare costs, wants to age “at home”, shortages of home health workers will put pressure on many.

Peace of mind couples never make another mortgage payment, “keys” to one’s home “wealth” creating a pool of spendable tax-free dollars they’ve slaved, struggled and saved over the decades, could make anyone, in my mind, sleep better.

The costs/guarantees are not cheap, they guarantee never to lose your home except, for non-payment of taxes, insurance and proper upkeep, may prove valuable to many and in retrospect appear very reasonable compared to selling, monthly payments of P&I or HELOCs that can be frozen.

If history is any guide with proper understanding this will be so popular the costs will have to go up on new loans to pay for the benefits and guarantees.

There is a myriad of great reasons to consider this. As a financial advisor for 25 years my thought it a desperation move was innocently yet completely wrong, they are so much more.

Things do not go as planned, personally having the blessings of affording rehab physically and mentally over the last few years was not fun, yet a God Send. Now is it my mission to help baby boomers, sharing paths to keys unlocking trapped wealth has and will help many. (Yes I am a “Boomer” and we do have a reverse mortgage on our primary residence.)

My opinion, think statute might prove it a fiduciary responsibility of advisors to at least discuss this potential “life ring” with clients.