Housing, Health Are 1/2 of Elderly’s Costs

How will your spending change once you retire? Will you be able to afford your needs? Will healthcare drain your budget?

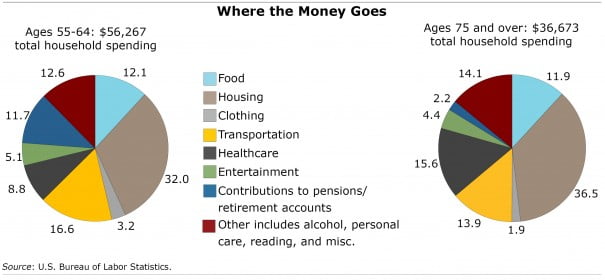

The U.S. Bureau of Labor Statistics (BLS) provides some clues in its data on the spending patterns of older Americans. The pie charts below show the percentage of total household budgets in 2014 that went to everything from housing to entertainment for two older age groups.

The two age groups selected highlight how spending changes between one’s final years in the labor force (ages 55-64) and retirement (the over-75 group). (Note: a household’s age is determined by the age of the individual who responded to the survey.)

The pie charts tell part of the story. Here’s what the BLS report adds to our understanding of spending among older Americans:

- Housing. Nearly 70 percent of elderly homeowners over age 75 have paid off their mortgages, while only a third in the 55-64 group have. But there are other costs associated with homeownership, such as maintenance. And a large minority of older people are renters. The upshot: housing gobbles up about one-third of older households’ yearly budgets, regardless of their age.

- Healthcare. The share of the 75-plus elderly population’s total spending that goes toward health care (15.6 percent) is nearly double that of the younger group (8.8 percent).

- Food. Age 75-plus households spend about 12 percent of their budgets on food – and so do people 55-64. But since the elderly households have smaller budgets in total, their food spending is significantly less – $4,349 per year – than the $6,800 spent at ages 55-64.

- Clothing and transportation. More 55-64 households are still dressing for, and commuting to, their jobs. Their spending on clothes and transportation – both in dollars and as a share of total expenditures – is substantially higher than spending by the 75-plus group.

- Retirement. A big difference between the two age groups examined here is that many people between 55 and 64 are still contributing to Social Security and retirement accounts. The over-75 group contributes very little, though elderly people who continue to work must pay payroll taxes like everyone else.

To read the BLS report, click here.

To stay current on our Squared Away blog, we invite you to join our free email list. You’ll receive just one email each week – with links to the two new posts for that week – when you sign up here.

Comments are closed.

How are you handling the other taxes paid by these groups? Is the $56K and the $36K net of state, federal and other taxes like property taxes? Your info above add up to 100% ????

Regardless of the motives, the market is still ripe for purchasing houses in the U.S. Our parents’ generation would have been horrified by the notion of banks lending money to people who could not afford to pay it back if the interest rate rose. This was a time when a mortgage was difficult to get – for my first house (in 1978) I had to wait six months for a mortgage calculated on three times my salary (most lenders would only give two-and-a-half). Things seem to be a bit different now, but are they any better?

Joe- great question.

Below is the link to the BLS report. As you will see, the pie charts are based only on household expense and do not include taxes. (Though for some reason they do include Social Security payroll tax as an expense.)

Here’s the link if you’d like to read more: http://www.bls.gov/opub/btn/volume-5/spending-patterns-of-older-americans.htm