How High School Finance Courses Fail

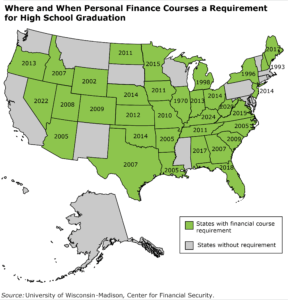

In more than 30 states, completing a personal finance course is required for a high school degree.

In more than 30 states, completing a personal finance course is required for a high school degree.

The requirement started gaining traction around the country in 2005, despite the long-running debate about whether the courses even work.

A new study gets at whether high school instruction is effective by asking a fresh question: do the finance classes make people feel better about their situation – and feeling better about one’s finances is an indication things are, in fact, improving.

This departs from past studies focused on objective measures like credit scores and past-due loans.

The researchers find that high school courses have generally been a positive development: adults who grew up in states that require the courses do, in fact, feel better about their finances compared to people from states lacking a requirement.

But what’s interesting in this study is that a group of disadvantaged Americans feel worse off for having taken the courses: high school graduates who didn’t go on to college. Rather than helping them manage their financial challenges, the classes are only making things worse.

Before examining the reason for this, consider how the researchers measured the feeling of well-being. They used recent data from a series of questions asked by the FINRA Investor Education Foundation: Do you feel you have control over your money? Could you afford an unexpected expense? Do you have a sense of achieving your financial goals?

Most important, FINRA asked, do you have the financial “freedom to make choices that allow a person to enjoy life”? FINRA’s survey was conducted in 2018, but this question is relevant in the COVID-19 recession. Enjoying life is essentially the flip side of having financial stress, which is currently very high among low-income workers without college degrees.

The researchers argue that adults with no more than a high school diploma who’d taken the personal finance classes feel worse, because the classes delivered a “harsh dose of reality” that can “make economically vulnerable people more aware of their precarious financial situation.”

More than a third of U.S. families couldn’t come up with $400 in an emergency, and improving financial literacy is one piece of tackling this complicated problem.

Based on their findings, the researchers said the best way to help the people who need it most is to design high school courses with practical strategies to meet their needs, given their scarce resources. The classes might focus, for example, on juggling bills and understanding taxes and the costs associated with parenting.

“The financial issues of non-college-going young adults warrant special attention,” they concluded.

Squared Away writer Kim Blanton invites you to follow us on Twitter @SquaredAwayBC. To stay current on our blog, please join our free email list. You’ll receive just one email each week – with links to the two new posts for that week – when you sign up here. This blog is supported by the Center for Retirement Research at Boston College.

Comments are closed.

Read Helaine Olen’s Pound Foolish to understand what personal finance education is really all about.

What’s the reason some states, in particular MA, do not have these requirements?

Thanks for your work.

John

I can’t say for sure why Massachusetts doesn’t have such a course requirement. But I can take an educated guess, because my husband was a high school biology teacher in Boston.

Since the advent of standardized testing, the tests are the No. 1 priority. Teachers don’t have enough time to teach what’s on the test. My husband could barely get through all of the high school biology information he knew would be on the test. That meant he didn’t cover, for example, climate science – in a biology class!

This isn’t a full answer but, he believes, an important part of it.

Thanks for the question.

You link to a piece published by the Center for Financial Security at UW Madison, authored by Jeremy Burke, J. Micheal Collins, and Carly Urban.

Readers might be interested in attending a webinar on October 6th at 12PM CST when Dr. Urban will be presenting her research on “Does State Mandated Financial Education Affect Subjective Financial Well Being”.

Here is a link: https://cfs.wisc.edu/2020/09/17/webinar-registration-now-open-does-state-mandated-financial-education-affect-subjective-financial-well-being/

The bigger question is does our educational system need a complete overhaul? The history is that a liberal arts (diverse) education prepares the young mind to choose a path in life. Might a practical approach as espoused in the article not be more beneficial where skills that everyone needs are addressed and ingrained work better? Then have “professional” and “technical” schools later?

Liberal arts courses can open the mind to poetry and other interesting subjects but do not provide the necessities of life.

Nor do liberal art courses necessarily expose the mind to life struggles others face and which may arise in one’s own life (pandemic, etc.). They may be mind opening, and as a history class, may prevent future errors. Yet, what should the basis of high school education be?

Is there a course like critical reading skills? A basic money course? As a substitute teacher in a high school, I was appalled at the lack of critical reading skills. When writing departmental reports for the US Department of Labor, the instructions were, “Never lie, but never make it sound bad.”

We need to rethink what we teach.

Using https://www.amazon.com/Pound-Foolish-Exposing-Personal-Industry/dp/159184679X I was left with a long list of finance books to potentially buy on Google.

A reality check says no one has a crystal ball about the future or investing. Investing means living within one’s means and letting others who are trained and work 24/7 in the industry try to figure which risk is lower and which promise is more sure of being greater than the risk. A gamble. I held a 5,000,000 Deutschmark bill in my hand which was nearly worthless when issued. In the 1970s inflation in Argentina was so rampant you bought something to barter with before inflation ate your paycheck.

We need to learn to budget and not live beyond our means and plan for the future using the fish theory of safety in numbers – having more than one financial advisor all of whom charge a percentage of around 1% so they gain as you do. Being charged a percentage means it cost the same to have one or many. Let them worry and watch over each other. Doesn’t eliminate risk but lowers chances of total collapse. Still, when all else fails, who will be there to help? Those you were kind to and helped in your life.

Money comes and money goes is what I taught my kids. Be kind. Started WITH $2,500 and twice saw drops of over $300,000 a year. Came out ahead in the long haul based on what I describe above.

Not rocket science. Live within your means, work hard, be kind. Tried to teach this, but no one wanted to listen to a form setter on a concrete crew. This can be taught in high school. Kids are not dumb. They too can be millionaires if you teach them values to live within their means and to be kind (true wealth).

I think it’s a positive that those without money are enlightened to better their situation. It’s the ones who whistle past the financial graveyard year after year, not saving a dime yet sending postcards from the Bahamas every other year, who wind up in big trouble in their 50s and 60s. Better to be shocked young than old.

I suggest comparing Illinois with Texas since the former started in 1970 and the later in 2007. Compare by year. Measure something concrete. I suggest 401k participation, debt on credit cards, late fees, net worth.

If nothing else, the students should be taught enough math that they understand compound interest. Interest is their friend when they’re putting money into savings or retirement (especially if there’s a company match), and their deadly enemy when they’re running up a credit card balance.

Just knowing that they should pay their bill in full each month would save them a lot of grief.