Medicare Advantage: Know the Pitfalls

Baby boomers on Medicare are streaming into Medicare Advantage plans, with nearly 18 million people currently enrolled in them.

But a new study identifies pitfalls that might not be obvious to those signing up.

Advantage plans are HMOs or PPOs that provide both basic Medicare Part B coverage and many of the benefits offered by supplementary Medigap insurance policies. But Medicare beneficiaries’ premiums for an Advantage plan plus Medicare Part B coverage are roughly half, on average, of the premiums for a Medigap policy plus Part B.

One reason is that Medigap policies typically cover more out-of-pocket costs. Another is that insurers offering Advantage plans assemble networks of hospitals and physicians to control their costs and reduce customers’ premiums.

But, the researchers point out, Advantage plans frequently limit “access to certain providers and increase the cost for care obtained out-of-network.”

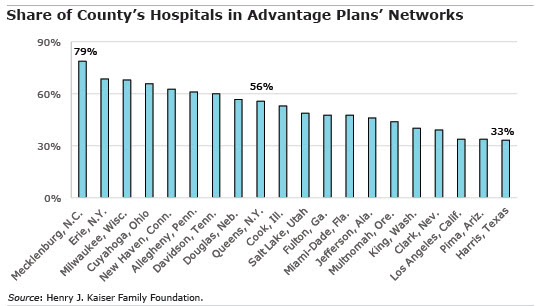

In nearly half of the 20 U.S. counties examined in a new study by the Kaiser Family Foundation, Advantage plans had limited networks of hospitals, potentially increasing consumers’ costs. Further, a large majority of Advantage plans did not include their county’s top-quality, high-cost cancer treatment center in the networks of approved health care providers.

And it can be very difficult to compare access to care and the future out-of-pocket medical costs that will result from a decision to go with an Advantage plan. Costs vary greatly among Advantage plan networks, with coverage often described in complex, incomplete, or confusing insurance plan documents, Kaiser said.

Consumers also face a dizzying array of choices. One example: In Cook County, which includes Chicago, eight difference insurance companies are selling 19 Advantage plans with 10 different provider networks.

Many retirees learn the ins and outs of the network only after they try to access medical care under the plan. The Kaiser report’s key findings provide a roadmap of things consumer should watch for:

- In the following nine counties, all of the Advantage plans had only small or medium-sized hospital networks and excluded at least one-third of the hospitals within their borders: Cook County; Clark County in Nevada (which surrounds Las Vegas); Davidson in Tennessee (Nashville); Harris in Texas (Houston); Jefferson in Alabama (Birmingham); King in Washington (Seattle); Pima in Arizona (Tucson); Los Angeles in California; and Salt Lake in Utah (Salt Lake City).

- There were big disparities in the share of a county’s hospitals included in that county’s plan networks, from 33 percent of Harris County hospitals to 79 percent of Mecklenburg County hospitals (Charlotte, North Carolina).

- The vast majority of Advantage plans had access to an academic medical center either in the county or in an adjacent county.

- Access to National Cancer Institute (NCI) cancer centers was more limited. Of the 20 counties studied, 15 had NCI centers within their borders. But 84 percent of the Advantage plans in these counties did not list the NCI cancer center in their provider network.

- A lack of clarity in online plan documents presents a major issue for cost-conscious consumers – and the lack of explicit mention of cancer centers is a prime example. In Salt Lake County, for example, provider directories in some Advantage plans include the Huntsman Cancer Center, along with its affiliate, the University of Utah medical center. But other Advantage plans list only the university medical center, making it “unclear whether a Medicare beneficiary can assume that coverage of care at the academic medical center includes care at the affiliated cancer center,” the Kaiser report said. The answer “most likely varies across plans.”

- It can also be difficult to ascertain whether other specialty care facilities affiliated with a hospital listed in an Advantage plan network, such as heart, rehabilitation, or women’s care centers, are covered as part of a plan’s provider network.

- HMOs tend to have narrower hospital networks than preferred provider organizations, or PPOs, Kaiser said. But there’s no evidence premiums are affected by whether an HMO or PPO plan has a broad or narrow network.

To read a blog that explained the pros and cons of Advantage versus Medigap plans, click here. To find a State Health Insurance Assistance Program that provides free counselors and help navigating the Medicare maze in your state, click here.

To stay current on our Squared Away blog, we invite you to join our free email list. You’ll receive just one email each week – with links to the two new posts for that week – when you sign up here.

Comments are closed.

Thanks for the post…awesome.

This article quotes someone as saying (inside the single quotes):

“”But, the researchers point out, (public Part C Medicare) Advantage plans frequently limit “access to certain providers and increase the cost for care obtained out-of-network.””

That is the way many — if not all — managed care health plans work…whether you are on Medicare or getting insurance from an employer or buying it yourself (through Obamacare or at full price). There is nothing here unique to Part C of Medicare. What are these researchers trying to investigate in their research: whether HMOs and PPOs work the way they should?

As an insurance agent for 35 years, I refuse to sell these plans for many reasons. No or very little premium sounds great until you need to use them and then you find out why I don’t like them. Co-insurances, deductibles and total out-of-pocket expenses are greater then just paying the premium for traditional Medicare with the supplement. Medicare part B premiums are paid by seniors regardless. In case someone is wondering, I do practice what I sell.

galbert

I assume the math differs everywhere in the country because the private Medigap supplements that you sell are regulated by the states. In Massachusetts, where I live, the combo of Part B and the private Medigap supplement you are selling seniors (plus Part D because a Medigap supplement does not cover self-administered drugs) costs about $2,500 a year more than an equivalent public Part C plan on top of B, even after the typical co-pays. And the Massachusetts Part C plans cover annual physical exams and typically vision testing and/or hearing aids partially, among the many medical services that Medigap plans do not cover at all. Most important of course, public Part C health plans include an annual out of pocket spend limit, something you cannot buy through a private insurer in Massachusetts and the major thing that Medicare lacks.

But every state is different. Maybe you are giving the seniors in your state good advice.

I am a satisfied Kaiser Medicare Advantage patient. When I moved back to California, from North Carolina, I realized the cost savings cited in the article, i.e, combined cost of Medicare C was substantially less than my Medicare supplement and Medicare D premium.

I value the excellent care I receive from Kaiser and the simplicity of essentially having a single payer health insurance.

Each policy proposal intended to improve the care of chronic conditions under Medicare is highlighted here: http://www.healthcaretownhall.com/?p=7985#sthash.H5THVkMJ.dpbs

I know that insurance companies try to seduce you into small co-pays and low premiums. More and more doctors are opting out of those plans and many services are not covered.

If you have straight Medicare with a regular secondary such as BCBS or AARP (NOT HMO) you can see any doctor. If he/she does not accept Medicare, at least you can submit his bill and get some of your $ back.