401(k) Balances Increased Very Little in the Last 10 Years

Alicia H. Munnell is a columnist for MarketWatch and senior advisor of the Center for Retirement Research at Boston College.

Auto enrollment without auto escalation of default contribution rate is part of the problem.

Every year, Vanguard puts out a comprehensive report “How America Saves” that summarizes the statistics for the defined contribution plans that the company administers. Vanguard tends to administer larger plans, so the plans are better designed than average and participants have higher incomes. In other words, it presents the best face of the 401(k) system.

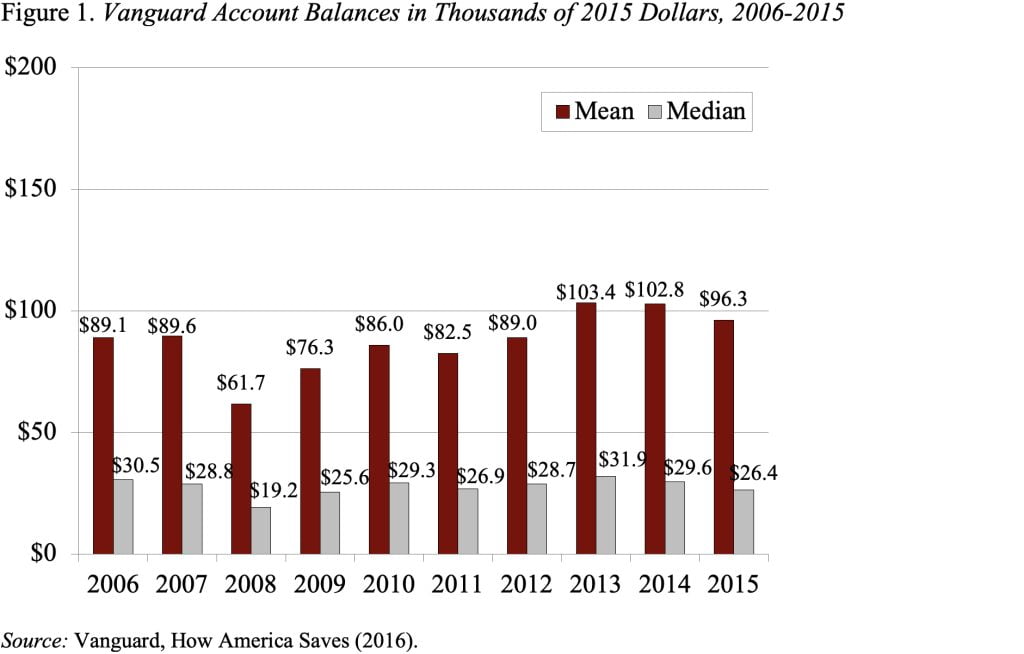

My focus here is account balances. In 2015, the average account balance was $96,300; the median was $26,400. Between 2014 and 2015, the average account balance was down 6 percent and the median down 11 percent.

This decline was attributable to three factors. The first is the rising adoption of auto-enrollment, which increases participation but also produces smaller balances. That is, more people save, but – because employees are typically enrolled at a default contribution rate of 3 percent – the accumulations are small. Second, markets were essentially flat in 2015, with the average one-year participant return equal to -0.4 percent. Third, Vanguard’s business mix was changing in that new firms moving over to Vanguard had lower account balances.

While Vanguard’s explanation for the decline in average and median balances between 2014 and 2015 alleviates concerns about the short-run performance of the 401(k) system, a longer-run perspective raises troubling questions. Figure 1 shows average and median balances for the last ten years in 2015 dollars. In terms of medians, 2015 is actually lower than 2006. This pattern could well reflect the expansion of auto-enrollment where a 3-percent default rate creates many small accounts. The fact that the average account balance in 2015 was only $7,200 higher than that in 2006 is more of a concern, since a relatively small number of large accounts affects this number. However, this pattern could be explained by the age distribution of the participants since the percentage of young participants, who have small balances, has increased over time.

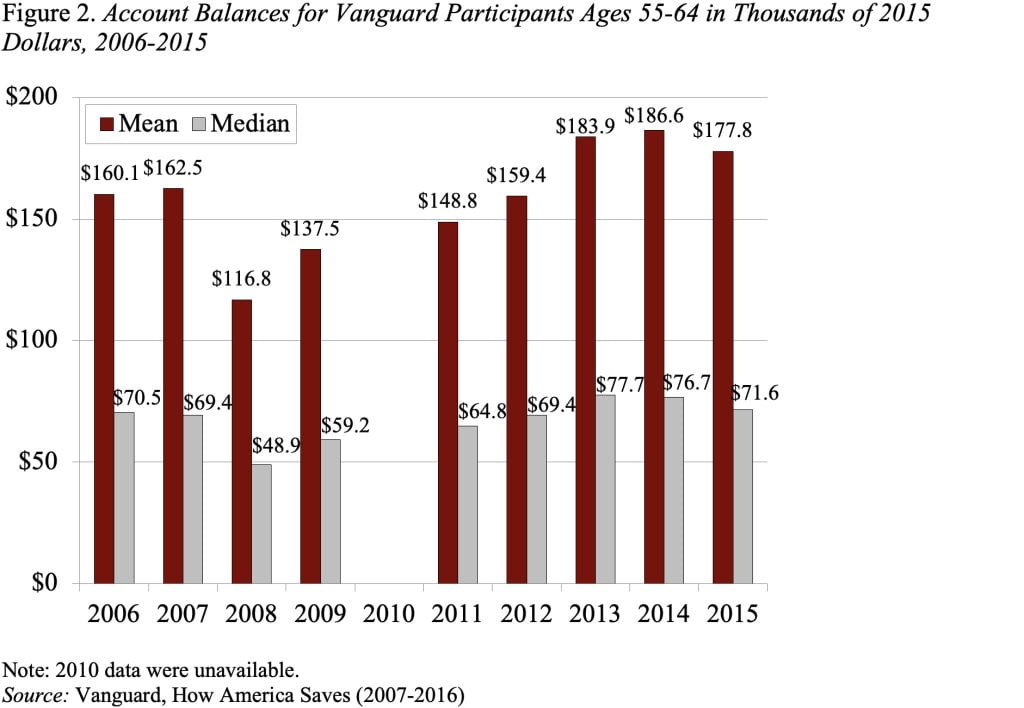

To get away from the impact of more young participants, it’s useful to look at balances for those ages 55-64, a group approaching retirement. As one would expect, these balances are roughly twice as large as those for the participant population as a whole (see Figure 2). But the pattern is quite similar; 2015 balances are only slightly higher than those in 2006.

The data on balances suggest that we have not made a lot of progress in terms of 401(k) saving. And Vanguard balances are probably higher than average given that it administers a large number of big plans. On the other hand, many people approaching retirement have moved some 401(k) balances over to Individual Retirement Accounts (IRAs). In 2013, the date of the latest Federal Reserve Survey of Consumer Finances, the median 401(k)/IRA holdings of working individuals with a 401(k) approaching retirement (55-64) were $100,000. So the picture is somewhat less bleak than the Vanguard data alone would suggest. But bleak, nevertheless.

The one immediate policy implication suggested by these numbers is that auto-enrollment without auto-escalation may well do more harm than good. If people are auto-enrolled at a 3-percent contribution rate, they are likely to stay with that rate. They may be worse off than if they were allowed to enroll at a later date on their own with an average contribution rate. My preference is to make auto-enrollment and auto-escalation mandatory for all 401(k) plans, starting at a default contribution rate of 6 percent and rising gradually to 10 percent.

Clearly changes are needed if 401(k) plans are going to be an effective savings mechanism.