A Major Change May Be in the Works for Your 401(k)’s Oversight

Geoffrey T. Sanzenbacher is a columnist for MarketWatch and a professor of the practice of economics at Boston College. He is also a research fellow at the Center for Retirement Research at Boston College.

Ending ‘regulation by litigation’ may erode some protections for workers.

Most people likely think their employer’s role in providing a 401(k) stops at choosing the provider, match rate, and investment options.

What most workers probably don’t know is that under the law governing 401(k)s – the Employee Retirement Income Security Act of 1974 (ERISA) – employers must administer plans for the “sole benefit” of participants. This role requires employers to do much more than the basics. For example, employers must ensure that the fees charged by providers are reasonable and the investment options are diversified, while avoiding conflicts of interest like forcing employees to buy company stock. Fall short and employers can be sued. In the past, lawsuits happened often. But – for better or worse – that might be changing.

To understand why these changes are important, it’s key to understand that 401(k)s are now the main way outside of Social Security that people save for retirement. Of workers with a retirement plan, over 80 percent have a 401(k) and few people save outside of them. Having a plan with low administrative fees and reasonably priced, well-diversified investment options (e.g., index funds) ensures that as much money as possible remains in those plans. The ability of employees to sue is one way plans are kept in line.

You see, the Department of Labor is charged with creating regulations, offering guidance, and enforcing ERISA, i.e., with making sure that 401(k)s are well run. Historically, the DOL hasn’t done much regulating or offering guidance, instead, ERISA has often been enforced through litigation. For example, when it comes to high fees charged by 401(k) providers, the department hasn’t specifically laid out what fiduciaries must do to ensure that fees are reasonable, but a plan participant will sue their (usually former) employer alleging that their 401(k) provider charged high fees. When the courts decide the case, they effectively rule on what fees are appropriate.

This approach gives DOL the ability to identify issues as they arise in the real world. But some people, including U.S. Department of Labor Solicitor Jonathan Berry, think that this approach may also encourage frivolous lawsuits.

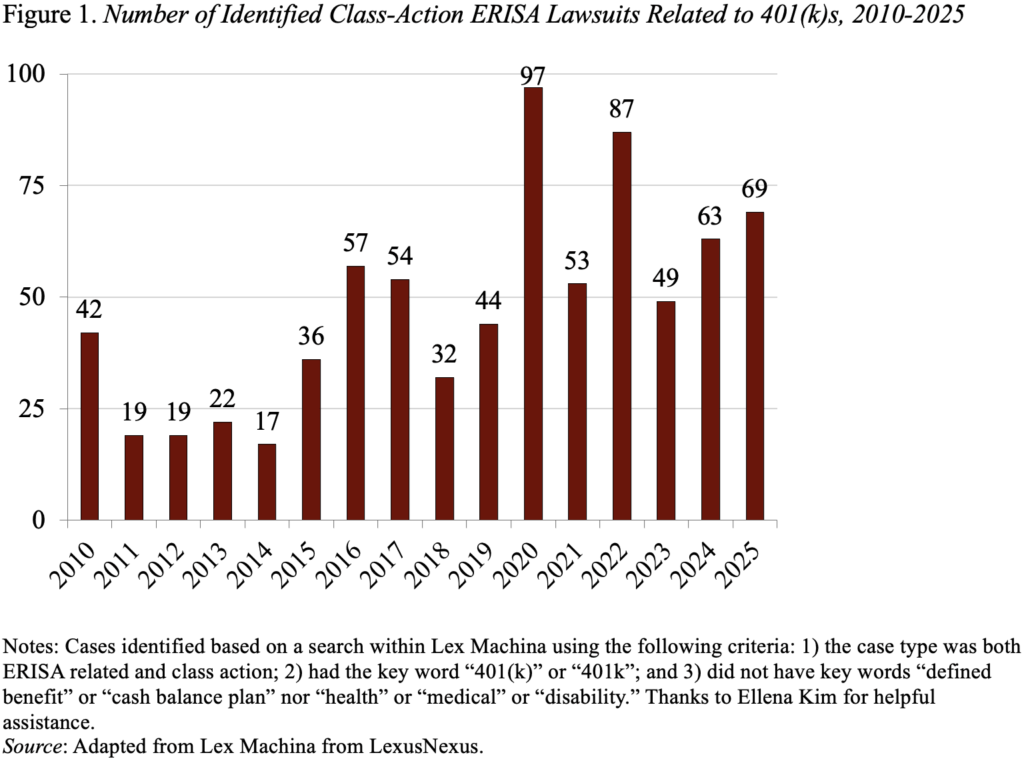

He recently remarked about a DOL brief in support of an employer: “[t]his filing is part of an ongoing effort by the Department to stop regulation by opportunistic litigation.” Given that the DOL may be pushing back on the primary way of ensuring that 401(k)s – including yours – are well run, it is worth asking: “why now,” and “is this a good idea?” As Figure 1 shows, 401(k) lawsuits have been going for a while. The rise in the mid-to-late 2010s was caused by an increase in lawsuits over excessive fees. The most recent uptick from 49 cases in 2023 to 69 in 2025 – which seems to be what upset the DOL – has to do with a drastic increase in lawsuits related to “forfeiture.”

Forfeiture is what happens when an employee leaves their employer before matched contributions are vested. That money is returned to the plan and it has been common and accepted practice for it to be used to pay the employer’s contributions for other plan members. The new lawsuits allege that this use is not in the best interest of plan members and benefits employers, reducing their payments. Instead, plaintiffs argue that the money should go to pay for plan administrative fees.

This type of lawsuit was very rare until recently. When I wrote about 401(k) litigation in 2018, we didn’t even mention forfeiture lawsuits. In 2025, there were over 40 of them. In the case of forfeiture, I can see DOL’s frustration. Most plan documents explicitly lay out that the current approach is one way that forfeitures can be used. Plus, guidance about pensions dating back to before 401(k)s even existed has said that using forfeitures to pay employer’s costs was appropriate.

In 2023, the IRS even proposed regulation for 401(k)s saying the same thing. These lawsuits seem to be looking for trouble with no obvious benefit to employees. After all, if employers must stop using forfeitures to pay their share of contributions, they may simply reduce their matches. With respect to forfeiture, trying to stop these lawsuits is a good idea.

But, more generally, I hope the DOL takes a measured approach to its pushback. It’s a bit unclear whether forfeiture is unique, or whether DOL will pull back in other areas. The assistant secretary of labor for the Employee Benefit Security Association (broadly in charge of ERISA), Daniel Arnowitz, has also indicated a desire to end “regulation by litigation” but without any mention of forfeitures specifically. The department should certainly support lawsuits where losses to employees are obvious. For example, past lawsuits have accused employers of offering expensive “retail” classes of investments instead of taking advantage of “institutional” pricing. In this case, had there not been a lawsuit, employees would clearly end up paying higher fees than needed.

The department should continue to support any lawsuit encouraging fee transparency, particularly because they seem to be effective. Finally, the DOL should avoid allowing alternative investments like crypto to proliferate into 401(k)s – a goal expressed by President Trump in a 2025 Executive Order – without either providing guidance on those assets’ (often expensive) fees or supporting litigation. The recent era of lawsuits has been marked by a gradual decline in the fees charged by 401(k) providers to employees, which is likely due to the litigation.

In short, pushing back against some of the more recent wave of lawsuits seems prudent. But the DOL shouldn’t completely throw away what, to date, has been its main way of ensuring that employers manage 401(k)s responsibly. The quality management of all of our retirement savings depends on it.