401(k) Lawsuits Are Surging – Here’s What It Means for You

Alicia H. Munnell is a columnist for MarketWatch and senior advisor of the Center for Retirement Research at Boston College.

Lawsuits may lead to lower fees, but may also stifle innovation.

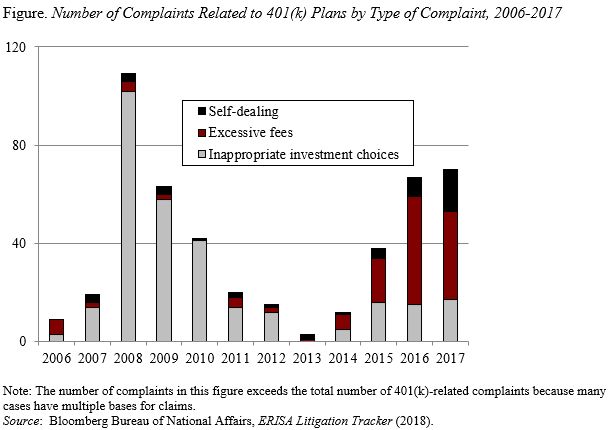

401(k) litigation – which had declined after the Great Recession – has surged again recently (see Figure). Over 100 new 401(k) complaints were filed in 2016-17 – the highest two-year total since 2008-09. A recent study explores the causes and potential consequences of this litigation.

The extensive litigation in the 401(k) area reflects the Department of Labor’s (DOL) approach to regulation. The agency is charged with enforcing the Employee Retirement Income Security Act of 1974 (ERISA), which governs 401(k) plans. But instead of issuing specific guidance on how plan fiduciaries should act – such as providing concrete factors to consider in determining whether fees are reasonable – it has tended to “regulate by enforcement” after the fact. While this approach provides the agency with the flexibility to identify emerging issues as they arise and tailor any response to specific circumstances, it also means that fiduciaries are often left to guess at what practices comply with the law.

The 401(k) lawsuits fall into three major areas.

Inappropriate Investment Choices: ERISA does not spell out specifically what type of investment options are appropriate, but rather puts the emphasis on the process of selection. Two fiduciaries could choose the same investment option and face different risks of liability if one followed a prudent decision-making and monitoring process and the other did not. Issues also arise when fiduciaries include the employer’s own stock in its 401(k) plan and that stock performs badly. Most of the suits in the wake of the Great Recession centered on investment choice.

Excessive Fees: Litigation often involves the allegation of excessive investment and/or administrative fees. Similar to the issues regarding inappropriate investment options, ERISA requires that fiduciaries follow a careful, prudent process to ensure that plans pay no more than reasonable fees for necessary services. Fees have been the major source of litigation during the recent resurgence of litigation.

Self-Dealing: In the ERISA context, the term “self-dealing” most often refers to a case in which a plan fiduciary acts in its own best interest rather than serving the plan and its participants. Employers that sponsor ERISA plans can also be held liable for permitting the assets in a benefit plan to “inure to the benefit of the employer.” Self-dealing accounts for only a small share of total lawsuits.

The extensive litigation inevitably has consequences – some good, some not so good, and some unclear.

Greater Use of Passive Investment Options: Plans have been shifting their assets towards more passive investments, at least partially because these investments typically do not pose a risk of significantly underperforming other index funds on performance and fee benchmarks.

Reduction of Asset Class Coverage: Litigation concerns may also have dampened fiduciaries’ appetite to add narrowly-focused investments to their menus. Given the lack of knowledge that most participants have about investing, the gains from not offering such funds in terms of lower fees would likely offset the losses from restricting these options.

Increased Fee Transparency: Greater scrutiny by plaintiff attorneys in 401(k) litigation, combined with the DOL’s 2012 regulation requiring service providers to disclose their fees to plan fiduciaries, have led to increasing fee transparency. Increased transparency has been accompanied by lower fees.

Lack of Innovation: Some experts are concerned that the fear of litigation prevents the use of creative options that may improve participant outcomes – like investment vehicles designed to provide a lifetime income stream when participants retire. After all, offering an annuity option would involve more complexity than passive investments (and thus higher fees) and would require the plan to choose a provider, which itself entails some risk.

In any event, take a look at the study; I think it’s really interesting!