Annuities Are Coming to More 401(k) Plans. Should Workers Embrace Them?

Geoffrey T. Sanzenbacher is a columnist for MarketWatch and a professor of the practice of economics at Boston College. He is also a research fellow at the Center for Retirement Research at Boston College.

The Trump administration wants more annuities in your 401(k). Here is why it might be a mixed bag.

When economists say that they have a puzzle, they don’t mean the kind with 1,000 pieces. Instead, economists are puzzled by things that don’t line up with their theories of how the world should work. One prominent example is the so-called “annuity puzzle.”

Since at least the 1960s, economists have theorized that most people should annuitize a portion of their wealth by handing it to an insurance company in exchange for a monthly, lifelong payment. Yet, despite the theoretical value of these contracts in insuring against outliving one’s wealth, people very rarely buy annuities. This hesitance stems from two sources. One is simple inertia – finding a provider can feel overwhelming. Second is something called “loss aversion.” Basically, people are afraid to give up the wealth they already have for a product that may be worthless should they die soon after purchasing it. Enter the Trump Administration, which for better or worse is trying to push lifetime income products into more 401(k) plans.

This push has two prongs.

The first prong is to reduce the litigation threat often surrounding those who offer these products. Litigation is a risk with annuities because they typically have higher fees that could trigger a lawsuit, as well as lower average returns. To this end, the Department of Labor (DOL) proposed a rule in March 2026 clarifying a 401(k) sponsor’s fiduciary responsibility for these products. The rule states that if the sponsor ensures that the asset’s benefit is in line with its fees, then it has done its duty (i.e., shouldn’t be sued). The DOL is also pulling back more generally from supporting litigation brought against 401(k)s.

The second prong is to clarify that these products can serve as a default investment option. At the end of 2025, the DOL wrote an advisory opinion saying that an asset with an annuity component could serve as a default in workers’ 401(k) plans if it is selected and monitored appropriately. Given the primacy of 401(k) accounts in Americans’ retirement savings plans and savers’ tendency to stick with defaults, it is important to think about whether these changes are a good idea. After all, shifting from a world where 401(k) savings are available as a large lump sum that can be used in emergencies to one where they provide a smaller, but permanent, stream of income is a big change.

I tend to support increased access to annuities as part of a prudently selected menu of investments. And reducing the fear of litigation is one thing that experts think could serve this purpose. Indeed, the 2026 DOL proposed rule has been lauded by some as encouraging the adoption of annuities. I’m doubtful.

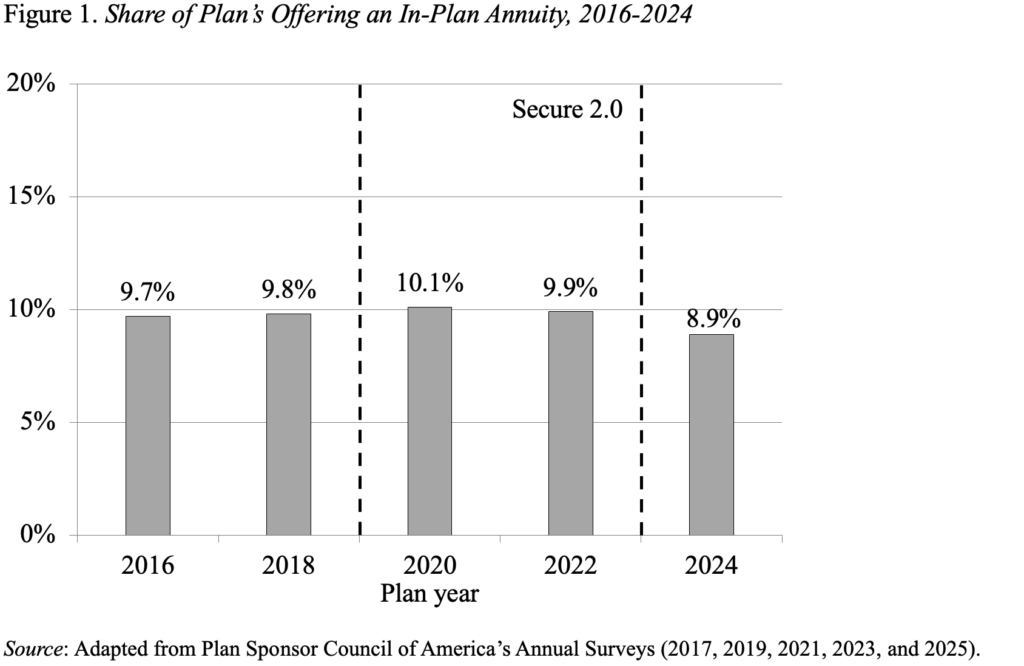

Consider the impact of two recent pieces of retirement legislation, Secure 1.0 and Secure 2.0, passed in late 2019 and late 2022, respectively. While both these laws contained provisions to make offering annuities in 401(k) plans easier, the needle hasn’t moved…at all. Figure 1 shows the share of plans offering an in-plan annuity since 2016 according to the Plan Sponsor Council of America’s Annual Survey.

To the extent a change happened, it was down not up. For optimists looking for more annuity products in 401(k) plans, the bright side is that both Secure Acts focused incrementally on the participant side of low annuity take-up. The Secure Acts’ only relaxation on the litigation front offered protection if an annuity provider went out of business. Perhaps the Trump Administration’s focus on reducing the threat of litigation due to high fees will move the needle.

On defaulting people into annuities, I am a bit less enthusiastic.

Defaults have a lot of power – the investment option that someone starts with is likely to be the one that they stick with. Annuities may make sense for workers at jobs that are very stable and unlikely to result in small balances that need to be ported across employers. But despite changes implemented by the Secure Acts, portability of 401(k) assets in annuities remains complex. For example, unlike assets like index funds, many annuities have a surrender fee that could be triggered when transferring savings from one provider to another at a job switch.

Plus, workers in these more mobile jobs also tend to have lower incomes. As my colleague Alicia Munnell recently pointed out, these workers may be better off holding onto their accounts to use as emergency savings instead of receiving a small monthly payment from an annuity.

Given that lifetime income products are likely to have both higher fees and lower returns than more traditional defaults like index funds and target-date funds, it is worth ensuring that only those workers who would benefit most from these costs end up in these assets. A default doesn’t seem like the best way to achieve this end. And it might not be easy to parse out which employees would be best suited for these products. For example, those who are likely to stick around in the job a long time are better candidates for annuity products than those who may move around frequently. But at hiring, identifying long-term employees is difficult.

In the end, I think that the Trump Administration’s push to get more money into 401(k) plans is a mixed bag. Reducing the fear of litigation to get these assets on plan menus makes sense even if it is a bit quixotic. Once on the menu, I would rather workers be allowed to make their way to these assets with some education as to their value.

Then again, what I would really like to see is the government ensuring Americans have access to a stable source of lifetime income by fixing the Social Security program’s finances. Maybe the real “annuity puzzle” is why this seems to be so darn hard.