Can Service Providers Convince More Small Firms to Offer 401(k)s?

The brief’s key findings are:

- Professional service providers – e.g., accountants, bankers, advisors – are trusted partners who can help convince small firms to offer retirement plans.

- However, many may unintentionally reinforce misperceptions about plan costs and administrative burdens, making adoption seem out of reach.

- Analysis of new survey results shows that the providers with the most success:

- are familiar with simple low-cost plan options;

- describe plans as a tool to boost recruitment and retention; and

- provide hands-on guidance to help firms set up a plan.

Introduction

The retirement plan coverage gap, which undermines the financial security of millions of U.S. workers, is driven by the lack of plans among small employers. Despite various efforts by policymakers across several decades to develop affordable and simple plans, many small businesses still overestimate the cost and administrative burden required to offer a plan, perceiving adoption as out of reach. The question is whether professionals – such as accountants, lawyers, financial planners/advisors, etc. – can encourage more small firms to offer retirement plans.

To answer this question, this brief – which is based on a recent study – reports on a survey of individuals who provide professional services to small businesses.1 The goal of the survey was twofold: 1) to assess the providers’ knowledge of the cost and administrative burden of retirement plans; and 2) to identify strategies that encourage plan adoption among small firms.

The discussion proceeds as follows. The first section highlights the role that professional service providers play for small businesses. The second section provides an overview of the survey participants. The third section reveals providers’ knowledge of the small business retirement plan ecosystem, costs, and plan options. The fourth section explores strategies that are more likely to lead to small business adoption of a retirement plan.

The final section concludes that service providers with higher plan adoption among clients are more aware of the low-cost, simple plans that are available. Such providers also frame retirement plans as a key recruitment and retention tool and take a hands-on approach to successfully guiding clients through the setup process. In addition, they are more likely to recommend specific plan options. The bottom line is that providers can help expand plan adoption among small businesses, but many of them overestimate the costs and burdens of offering a plan, potentially reinforcing small business misperceptions.

Professional Service Providers for Small Firms

At any given time, only about half of U.S. private sector workers participate in an employer-sponsored retirement plan – mostly because their employer doesn’t offer a plan – and few workers save without one. This coverage gap, which undermines the retirement security of the nation’s workers, is driven by small employers.

An earlier survey of small firms and retirement plans – jointly conducted by the Center for Retirement Research at Boston College, the Employee Benefit Research Institute, and Greenwald Research – found that many firms overestimate the financial and time costs required to offer a plan, and that better awareness of lower-cost plan options and tax credits could help move the needle on the coverage gap.2 Existing educational efforts, though, have had limited success.3

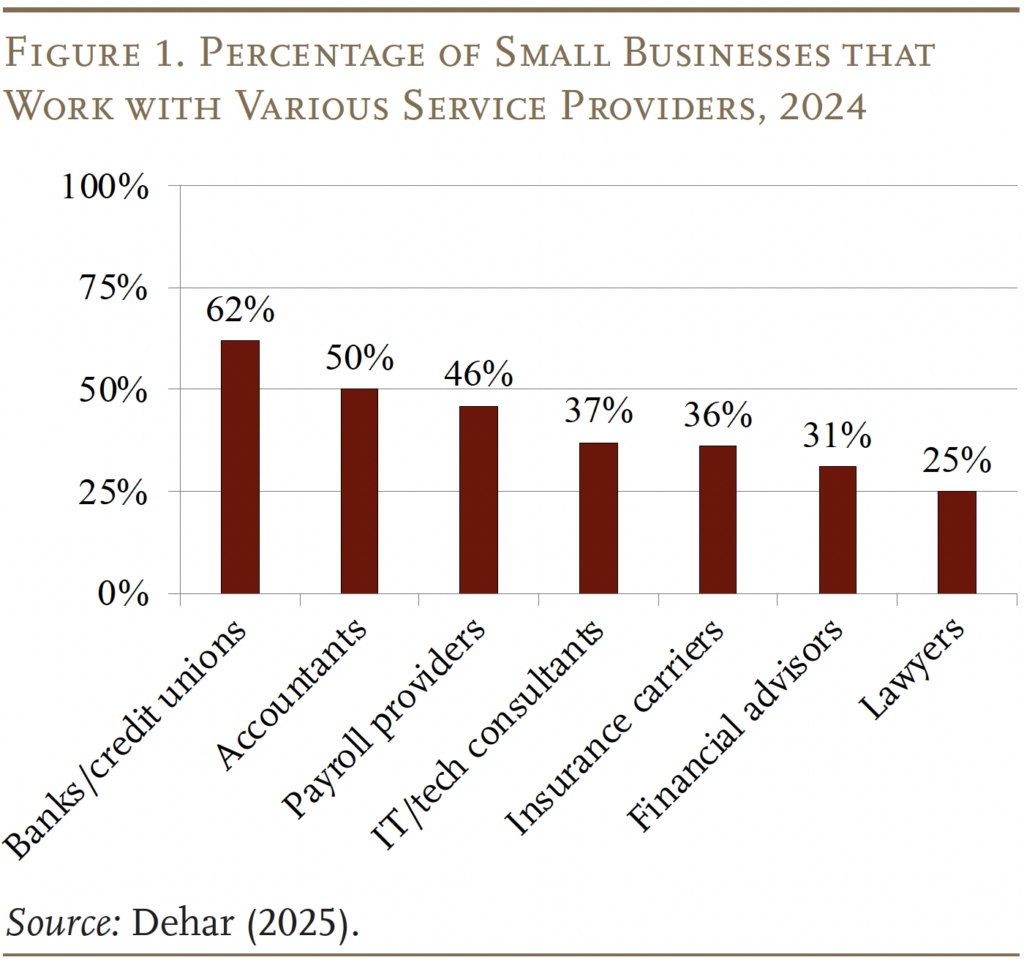

One potential channel to help small employers overcome misperceptions is through professional service providers (i.e., accountants, lawyers, financial advisors, bankers, or HR consultants). According to a recent survey by Gusto, many small firms work with at least one of these providers (see Figure 1) and often build long-standing business relationships with them.4

These professionals are often viewed as trusted and knowledgeable sources and may be able to help guide small businesses on their financial decisions.5

The 2025 Small Business Service Provider Survey

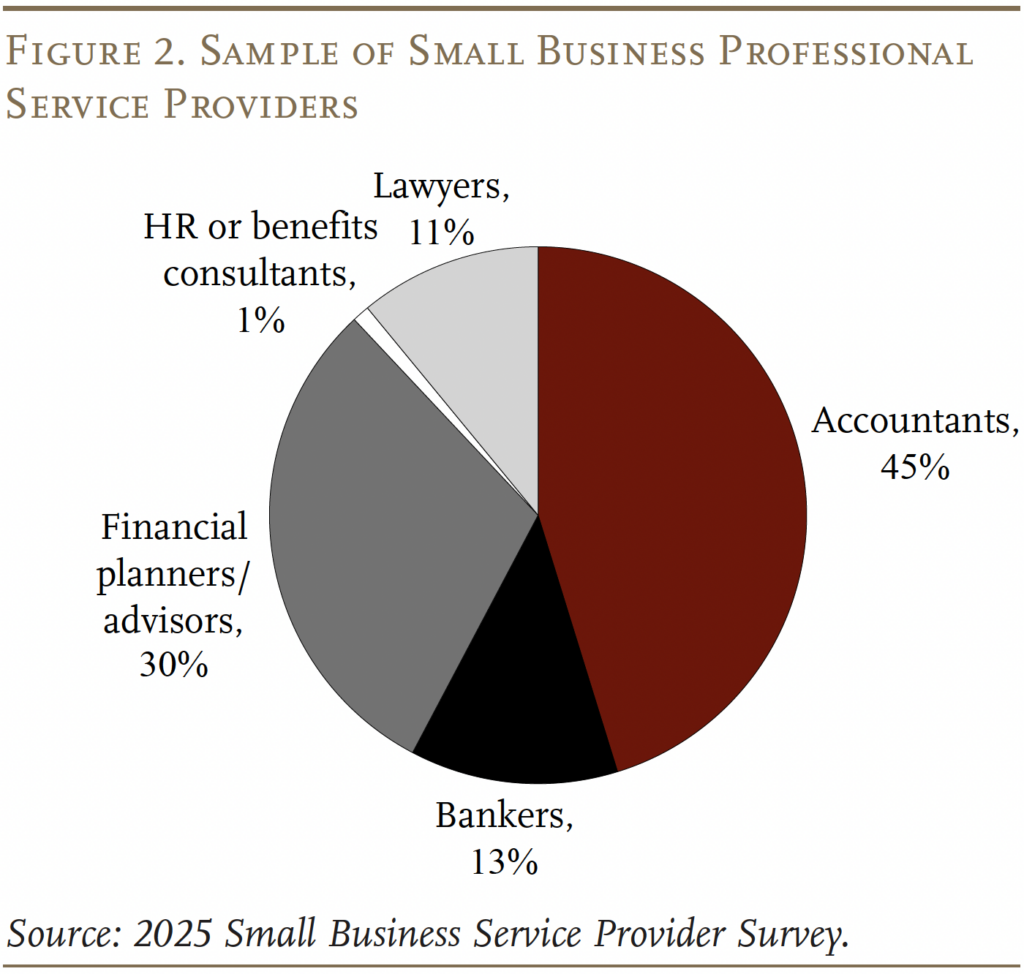

The new survey was conducted between September and October 2025 and included 506 providers who have at least five clients that are small businesses and who might be involved with helping them set up a retirement plan.6

The respondents covered several types of providers: 45 percent were accountants, 30 percent financial planners/advisors, 13 percent bankers, 11 percent lawyers, and the remaining small portion were HR or benefits consultants/providers (see Figure 2).

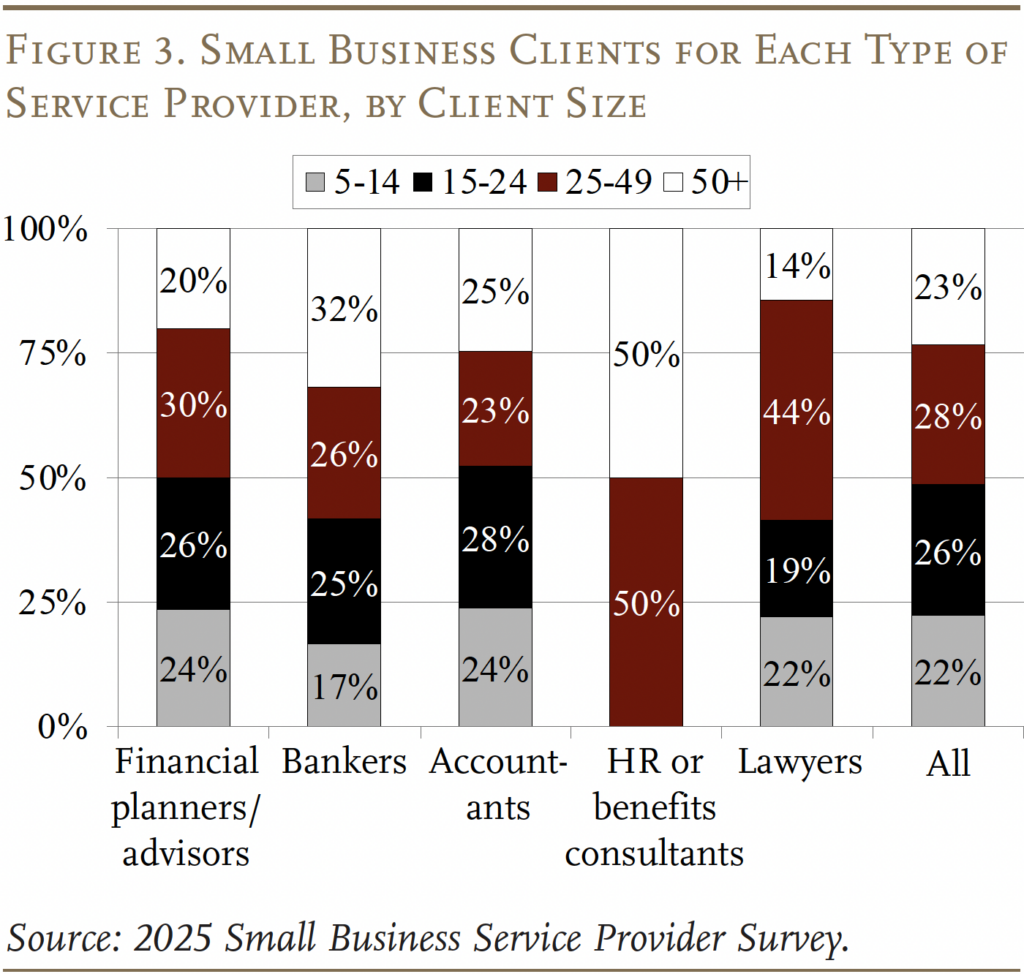

For most of the providers, employers with less than 25 employees account for about half their clients, and those with less than 50 employees constitute the bulk (see Figure 3).

Over half of service providers have worked with their small business clients for an average of 5 years or more, and over a third have done so for over 10 years, indicating a relationship of trust.

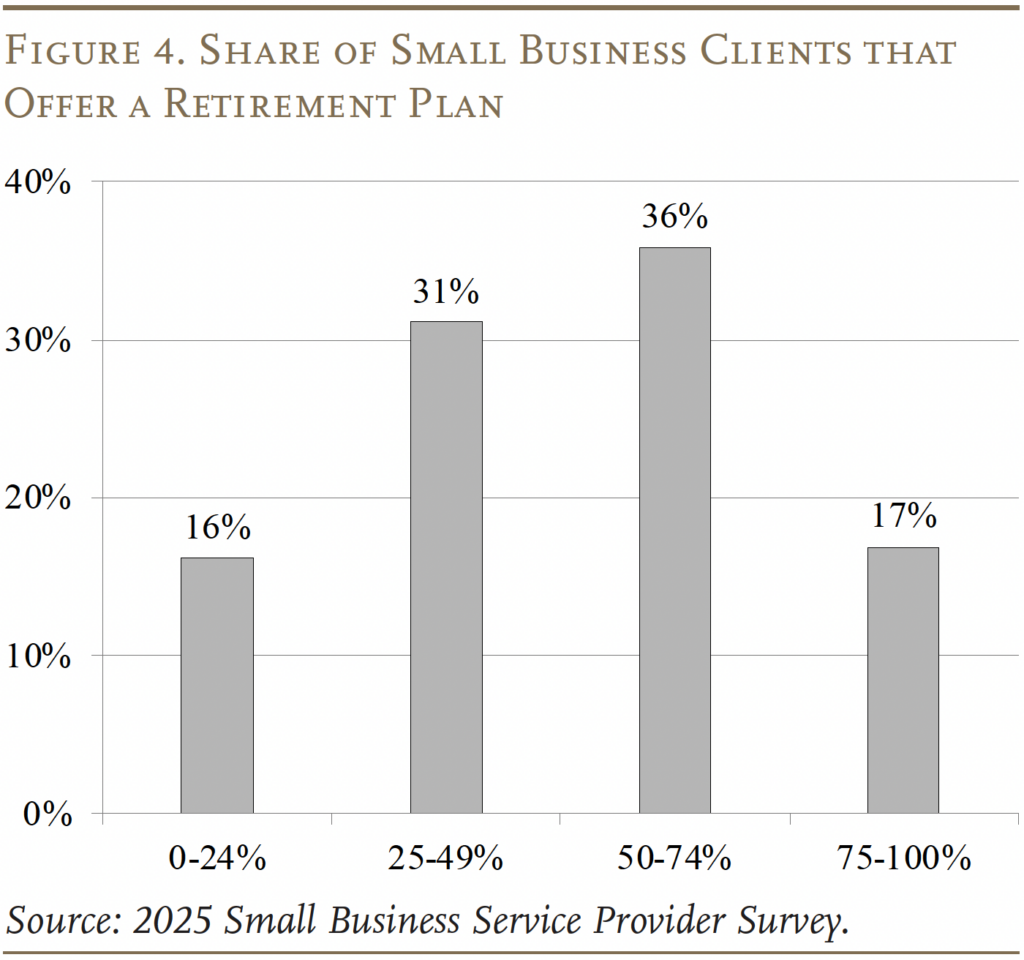

Among the service providers, the share of their small business clients that offer a retirement plan varies widely (see Figure 4). Seventeen percent of providers report that virtually all (75 percent or more) of their small business clients offer a retirement plan. At the other extreme, 16 percent say that less than a quarter of the small employers they work with have a plan.7 The remaining two-thirds of respondents fall in between.

Given the wide dispersion in the share of clients with a retirement plan, a key question is the extent to which providers with a large share of clients with plans differ from those with a small share, in terms of: 1) their knowledge of retirement plans; and 2) the strategies they use to promote these plans to their clients.

Knowledge of Plan Adoption and Administration

Helping small businesses evaluate whether to offer a retirement plan and navigate the complexities of setup and administration requires considerable knowledge about plan options. While our sample of service professionals support small businesses with a wide range of functions, most are not experts in retirement.

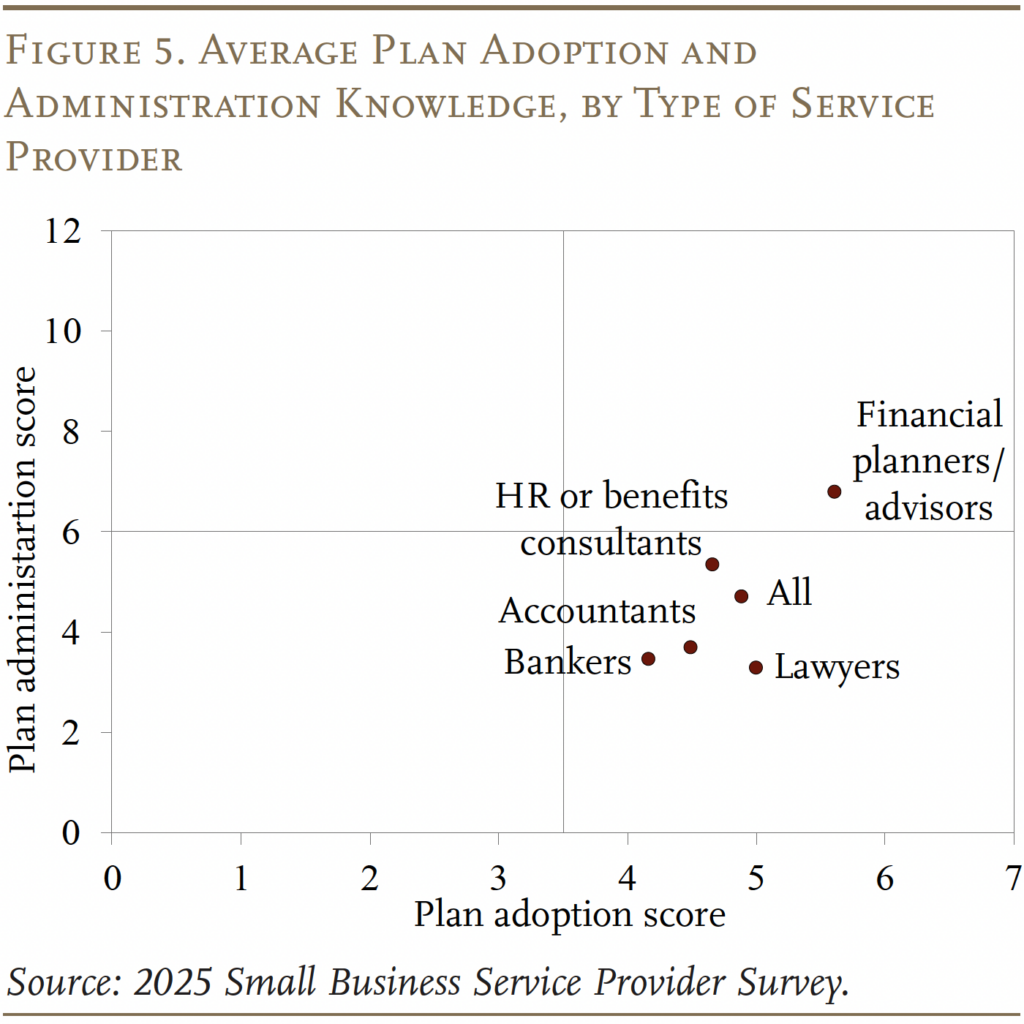

That said, the survey included questions about two broad areas related to retirement plans: 1) plan adoption (e.g., tax credits and match requirements); and 2) plan administration (e.g., the time and financial cost involved). Respondents were given a score from 1 to 7 for plan adoption knowledge (7 = the highest) and 1 to 12 for plan administration knowledge. The average scores, by service professional type, are shown in Figure 5. While most service providers are fairly knowledgeable about plan adoption, only financial planners got more than half of the plan administration questions correct.

Among the plan administration topics, respondents were most likely to miss the question on investment selection. About 35 percent of them thought that an employer must always select and manage the investments in a plan lineup. In reality, employers never have to manage the investments, and many plans offer a pre-set lineup of investment options.

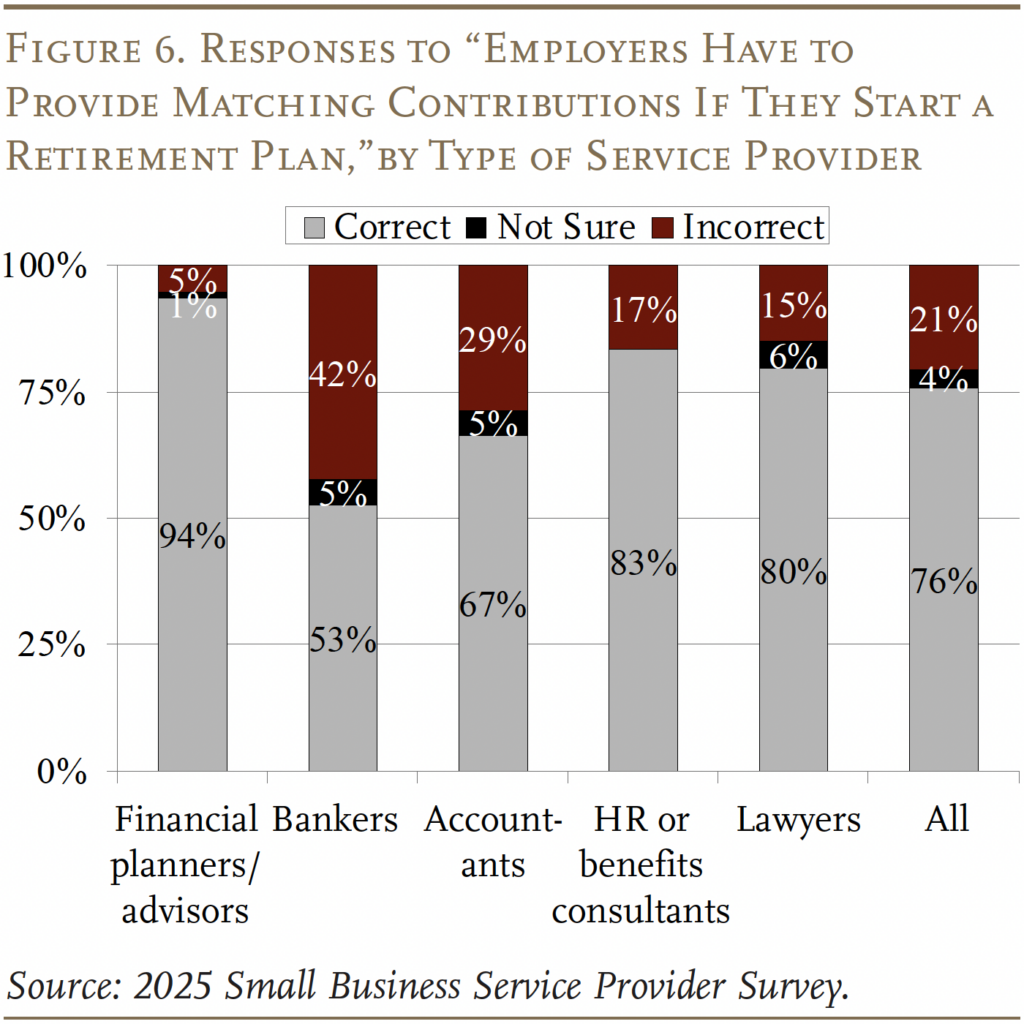

In terms of whether matching contributions are mandatory, most service providers knew that employers do not have to offer a match, but 42 percent of bankers and 29 percent of accountants thought that matches are required (see Figure 6). Even more concerning, one-quarter of bankers and one-fifth of accountants thought that only businesses with 50 employees or more could even offer a retirement plan.

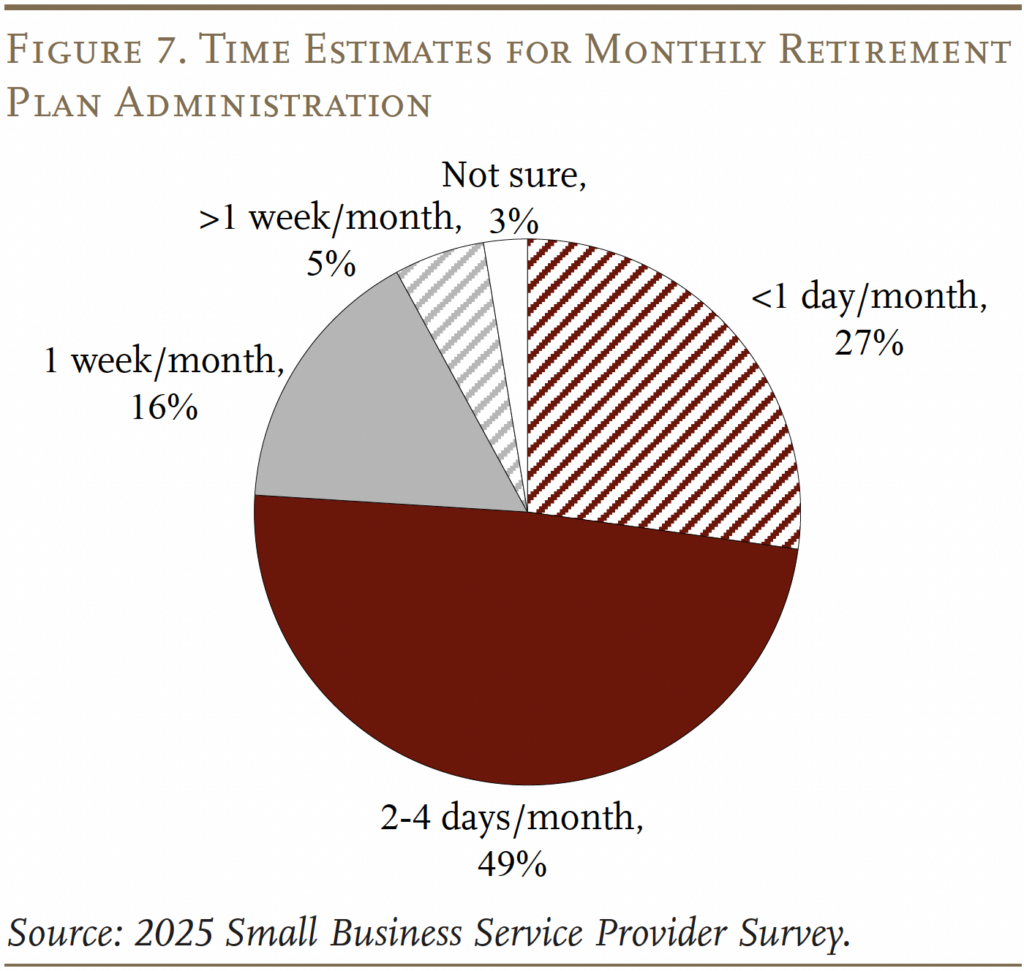

In addition to misperceptions about eligibility and requirements of offering a retirement plan, service providers also have broader misperceptions about how much time and money it would cost for small businesses to operate a plan. A full 70 percent of providers thought that, after a plan has been set up, it would still take several days to a week or more every month to manage a plan (see Figure 7). In fact, managing a retirement plan should only take a few hours a year after it is initially set up.8

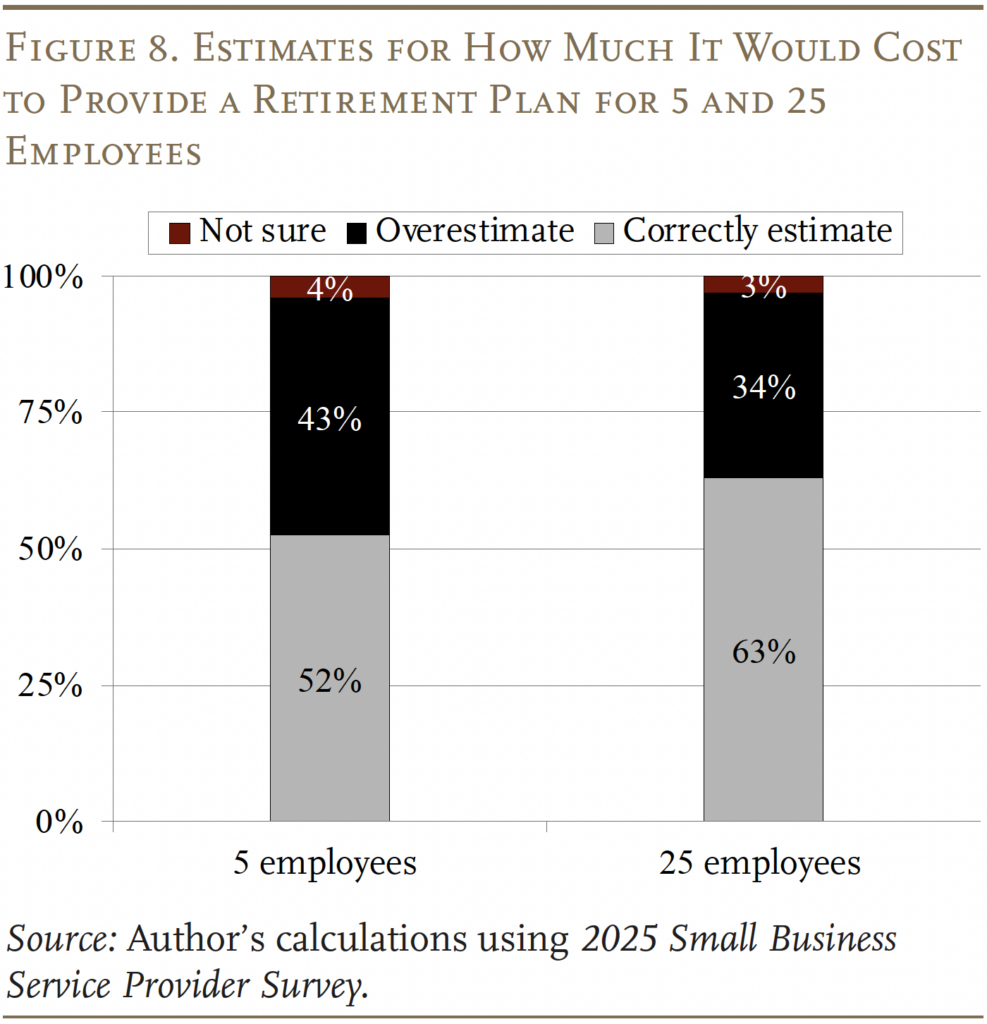

Not only do most service providers overestimate the time it takes to administer a plan, but many also overestimate the cost of offering a plan. Several 401(k) providers show options where annual employer costs would be less than $2,000 for a firm with 5 employees, and less than $3,000 for a firm with 25 employees.9 These costs are also before any tax credits. In contrast, almost half of service providers overestimate the cost of offering a plan (see Figure 8). Over 40 percent believe it would cost more than $5,000 per year for a firm with 5 employees, and at least a third believe that it would cost over $10,000 for a firm with 25 employees.10 The shares of accountants, bankers, and lawyers who overestimate costs are much higher.

These time and cost misperceptions among service providers can really hinder their clients from starting a retirement plan. Thus, not only small employers themselves could benefit from better information on retirement plan options, but so could many of their providers – particularly bankers, accountants, and lawyers.

Strategies that Encourage Retirement Plan Adoption

While correcting misperceptions is an important step, it is only one part of the equation of expanding coverage. We also examined whether the specific strategies used by service providers – such as framing retirement plans as a hiring solution or offering more guidance to small employers – are successful in encouraging clients to offer a plan. Using a simple linear regression, it is possible to see whether specific strategies are associated with higher plan adoption.11

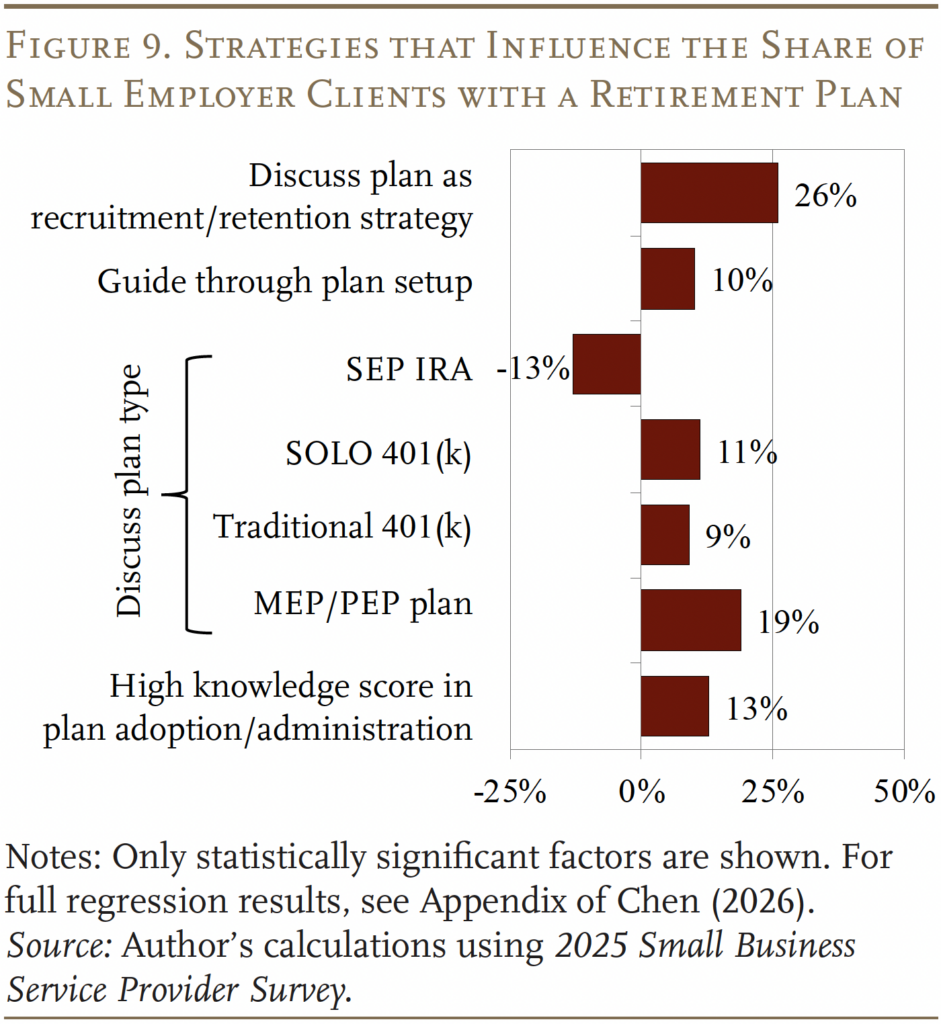

The strategy with the largest impact on plan adoption is framing retirement plans as a tactic for employee retention or recruitment (see Figure 9). Additionally, professionals who adopt a very hands-on approach and guide their clients through the entire process of plan setup tend to have more clients with a plan. Interestingly, successful service providers also tend to discuss certain types of plans with their clients (and not discuss others). Not surprisingly, providers with higher knowledge scores are also more likely to have a higher share of clients with a retirement plan – likely because they are aware of the many low-cost, low-burden plan options that exist.

These results show that framing a retirement plan as a recruitment and retention tool, providing a high level of guidance, and focusing on certain types of plans may help encourage small employers to offer a plan. Additionally, improving knowledge of plan adoption and administration cost details among these service providers can also help.

Conclusion

Professional service providers for small employers are trusted partners in key business decisions and have the potential to play a meaningful role in closing the retirement coverage gap. Yet, many may unintentionally reinforce the same misperceptions about plan costs and administrative burden that deter employers from offering a plan. Improving service providers’ knowledge – particularly accountants, bankers, and lawyers – of the many plan options that limit employer costs and responsibilities could help close the small business coverage gap.

However, improving knowledge is just the first step. What distinguished the providers with a higher retirement plan adoption rate among their clients were two strategies: 1) they framed these plans as a tool for attracting and retaining employees; and 2) they took a hands-on approach and guided their clients through the process of setting up a plan. Successful service providers also tended to steer their clients toward certain plans.

The results suggest that improved knowledge and shifts in framing, as well as more involved guidance, can meaningfully influence whether a small business offers a retirement plan.

References

Chen, Anqi. 2026. “Can Professional Service Providers Help Encourage Small Businesses to Offer Retirement Plans?” Special Report. Chestnut Hill, MA: Center for Retirement Research at Boston College.

Chen, Anqi. 2024. “Small Business Retirement Plans: How Firms Perceive Benefits & Costs.” Issue in Brief 24-7. Chestnut Hill, MA: Center for Retirement Research at Boston College.

Dehar, Ravi. 2025. “Strengthening Small Business Banking Relationships Through Value-Added Services.” Gusto Embedded Blog (March 13). San Francisco, CA.

Drobleyn, Eric. 2023. “How Much Time Does Annual 401(k) Administration Take?” Mobile, AL: Employee Fiduciary.

Endnotes

- Chen (2026). ↩︎

- Chen (2024). ↩︎

- Several government agencies, such as the Department of Labor, Department of Treasury, and Small Business Administration, have conducted educational efforts but they have had little impact on coverage. ↩︎

- Dehar (2025). ↩︎

- Gusto’s survey includes non-financial service providers, such as IT consultants (see Dehar 2025). Our current study focuses on service providers who might be involved in a small firm’s financial decisions. ↩︎

- Greenwald Research fielded the survey, which includes service professionals who advise small business owners, as long as they discuss small business needs rather than just their personal financial needs. ↩︎

- Financial planners/advisors were most likely to report that 75 percent or more of their small employer clients have a retirement plan while bankers were most likely to report that less than half of their small business clients have a plan. For a complete breakdown, see the full study (Chen 2026). ↩︎

- Drobleyn (2023). ↩︎

- For example, a Guideline 401(k) can be as low as $708/year for 5 employees and $1,668/year for 25 employees. Similarly, Human Capital offers 401(k)s for $1,740/year and $2,940/year, respectively. One reason for the perceptions of high costs may be that the service providers mistakenly assume that small employers have to provide safe-harbor plans, which require employers to provide a matching contribution that is immediately fully vested. However, common small employer retirement plans – such as starter 401(k)s, SEP or SIMPLE IRAs, and even PEPs – are not safe-harbor plans. ↩︎

- Even for safe-harbor plans, the cost for providing 5 employees with a 401(k) is roughly $10,000 before any tax credits and under $4,000 after tax credits. The cost for 25 employees is about $45,000 before tax credits and $19,000 after tax credits. These estimates assume average employee salaries of $60,000, average employee contributions of 3 percent with a 100-percent employer match, and a 100-percent participation rate. Given these unrealistically generous assumptions, about 20 percent of bankers and accountants and 30 percent of lawyers still overestimated the cost or responded “don’t know.” ↩︎

- The regressions controlled for retirement plan knowledge and other factors linked to higher adoption rates, such as a service provider’s years of experience, having more small business clients, and being more likely to have clients in industries with higher retirement plan coverage (i.e., professional, technical, and scientific services). ↩︎

Chen, Anqi. 2026. "Can Service Providers Convince More Small Firms to Offer 401(k)s?" Issue in Brief 26-9. Chestnut Hill, MA: Center for Retirement Research at Boston College.