Fewer, Clearer Medicare Part D Choices

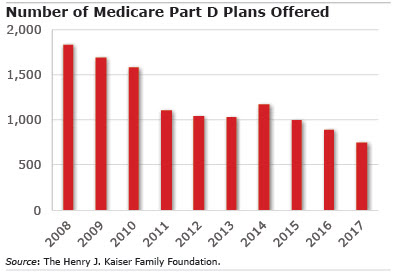

A decade ago, the nation’s Medicare enrollees had more than 1,800 different prescription drug plans to choose from. In the 2017 open enrollment that started on Oct. 15, that number dropped to just 746.

A decade ago, the nation’s Medicare enrollees had more than 1,800 different prescription drug plans to choose from. In the 2017 open enrollment that started on Oct. 15, that number dropped to just 746.

News of higher Part D drug plan premiums and out-of-pocket costs in 2017, estimated in a new report by the Henry J. Kaiser Family Foundation, will not be welcome by the nation’s older population. But Squared Away also wanted to know whether fewer plan options are good or bad for consumers.

“It’s good in the sense [federal] efforts are bearing fruit in giving people options that are more distinct from each other than in the past,” said Juliette Cubanski, Kaiser’s associate director of Medicare policy. At the same, she said, retirees “still have a lot of choice in this marketplace.”

The number of plans has shrunk steadily for a variety of reasons since the 2006 inception of the prescription component of Medicare, known as Part D. In the early years of the program, plans started disappearing amid consolidation among insurers and pharmacy benefits managers, she said. More recently, a few Part D plan providers have pulled out of the market.

But Cubanski said recent reductions in the number of plans were primarily by federal design. In 2011, the Centers for Medicare and Medicaid (CMS) stepped in and began requiring insurers that offered more than one Part D plan in a region to make sure the differences among their plans were clear and distinct to Medicare beneficiaries.

Driving the regulation, she said, was that “people weren’t able to differentiate between their plans.” In theory, having more options should be good for consumers if it spurs competition among providers and potentially reduces premiums. But research has shown that people are only confused when they have too many health plan choices and are more likely to make costly mistakes.

The new regulation went so far as to state that CMS might ask an insurer to “withdraw a [Part D] formulary in which no meaningful differences can be demonstrated.” In the wake of this regulation, insurers are more likely today to offer just two plans per region rather than the three plans offered in the past, Cubanski said.

Picking the right Part D plan is crucial at a time of surging prices for prescription drugs, particularly specialty drugs. Seniors taking multiple medications are vulnerable to rising prices, yet Medicare is barred by law from negotiating drug prices on their behalf.

Average Part D premiums increased from $37 per month in 2015 to $39 in 2016. In addition, plans charge copayments or deductibles.

A couple more dollars per month “doesn’t sound like a lot of money,” Cubanski said, “but it came after several years of a flat trend in the average premium or even some decreases.”

In 2017, Kaiser estimates monthly premiums will increase to more than $42, and annual prescription deductibles are expected to rise from $182 in 2016 to $195 in 2017.

To stay current on our Squared Away blog, we invite you to join our free email list. You’ll receive just one email each week – with links to the two new posts for that week – when you sign up here.

Comments are closed.

Boy, where to start with this one? I’ve run hundreds of “drug reviews” using the Plan Finder tool at http://www.medicare.gov. This is a very reliable source on costs, though not 100 percent foolproof. Everyone with a Part D drug plan needs to run an annual review. A good agent will do this for you, otherwise get online and run it yourself. What you learn can potentially save you thousands of dollars.

The plans themselves ALL follow a basic blueprint on plan design and coverage limits. Where they vary and where costs can escalate most is whether your drug is “on formulary” or not. Even if “on formulary” costs between plans can still vary dramatically for the same drug.

Picking the best or lowest cost option is thus a very subjective process for each person. You also need to pay attention to what pharmacy is used, as some Part D plans further differentiate costs between “preferred” network pharmacies and “standard” pharmacies.

The biggest “mistake” in drug plan choice is having a drug that is not covered by the plan formulary. You pay ALL costs for drugs not on formulary, even at Catastrophic level, unless you’ve gained a formal “exception” from the plan. Only about 30 percent of all exception requests are granted, from info I’ve seen.

Saying drug costs are not negotiated is a misnomer. While Medicare itself does not directly negotiate drug costs, as the article points out, cost are instead negotiated by the plans themselves. Since the plans must be approved for sale by CMS, the plans in effect do this for Medicare.

One reason premiums are rising is not mentioned in the article. Specifically, the Initial Coverage Limit for 2017 rises to $3,700, up $390 from the 2016 limit of $3,310. This is the amount you can spend on drugs before reaching the “donut hole” gap.

The article also places too much emphasis on effects of rising premiums. The key for each person’s decision should NOT be guided solely on premium or deductible. These are simply not enough information for an informed decision.

The operative number is “total estimated costs” which includes plan premium + deductible if any + co-pays + costs in the donut hole gap (if reached) + costs at the Catastrophic level. The Plan Finder tool will calculate this for you with a list of your medications.

Btw, you do NOT have to open an account on the Medicare website to run this…you can bypass that and go straight to a drug plan search.

I hope this is helpful to you or someone you know.

Already got notice that Part D premium with Express Scripts will be $36/month in 2017 with $400 deductible and co-pays. Medicare should be allowed to negotiate drug prices.