How ‘No Tax on Overtime’ Could Impact Behavior in Good Ways – and Bad

Geoffrey T. Sanzenbacher is a columnist for MarketWatch and a professor of the practice of economics at Boston College. He is also a research fellow at the Center for Retirement Research at Boston College.

The One Big Beautiful Bill Act deduction that could encourage bad actors.

Let me start by heading off some angry mail: I’m all for rewarding hard work. But the “No Tax on Overtime” deduction of the “One Big Beautiful Bill Act” (OBBBA) gives me pause. There’s evidence that many more people than expected are claiming the deduction. Understanding the reason for these excessive claims can help policymakers evaluate the law’s impact. Is the deduction having its intended effect – rewarding people for working more? Did poor data on overtime pay before OBBBA lead to incorrect expectations? Or, instead, is this deduction needlessly costing the government money at a time when the interest payment on public debt is at one of its highest levels on record?

I’ll get to how a costly outcome could happen, but first a primer on overtime. At the federal level, overtime pay is governed by the Fair Labor Standards Act (FLSA). The FLSA mandates that when workers exceed 40 hours of work in a week, their pay be 1.5 times their base wage. So, under FLSA, a worker making $20 an hour would be paid $30 once they exceed 40 hours in a week. Beyond FLSA, some states mandate additional overtime (e.g., California double pay beyond 12 hours in a day) and some companies voluntarily offer it (e.g., Costco’s Sunday “premium pay”). For tax purposes, in the past, any overtime earned was like every other dollar.

However, from 2025 through 2028, the OBBBA allows a deduction of up to $12,500 for overtime pay received ($25,000 for joint filers). Importantly – and some argue confusingly – the “No Tax on Overtime” provision only exempts the extra pay. In the example above, the extra $10 earned. So, a worker who put in 50 hours at $20 an hour in base pay would make $1,100 dollars ($20*40 + $30*10) and receive a deduction of $100 ($10*10). The OBBBA also doesn’t include any state- or company-specific overtime.

This structure could exaggerate overtime claims relative to expectations in two ways. First, workers may simply not understand the law, claiming inappropriately their state- or company-specific overtime as tax deductible. Second, by treating overtime pay differently than other dollars earned, the OBBBA encourages workers to manipulate their hours worked – both legitimately and illegitimately.

The legitimate way to get a larger deduction is to work more overtime hours. For workers who already get overtime, it may be straightforward to ask for more. After all, their employers have already shown a willingness to pay extra. And for workers near the threshold, it may be possible to convince employers to add just a little more time. This sort of change in behavior would hardly be terrible. It would generate more income for workers, more output for employers, and more revenue for the government in the form of base-pay taxation.

A recent Center for Retirement Research at Boston College issue brief I wrote examined how many workers might be able to easily gain legitimate tax-deferred overtime by adding a few hours. The study found that nearly three-quarters of hourly workers either get overtime now or could get it by working just a little more. For salaried workers – who can also claim overtime under FLSA – less than 5 percent are likely to be able to legitimately take advantage of OBBBA. This low rate stems from the fact that, under FLSA, employers of workers earning $35,568 or more are allowed to declare most of those employees exempt from overtime.

OK, so a lot of hourly workers and a few salaried workers could work more hours…big deal. But, my brief also looked at ways employers and employees could manipulate pay to allow more “overtime” hours without a change in actual hours worked. I put forward two ways this could happen under OBBBA, one each for hourly and salaried workers.

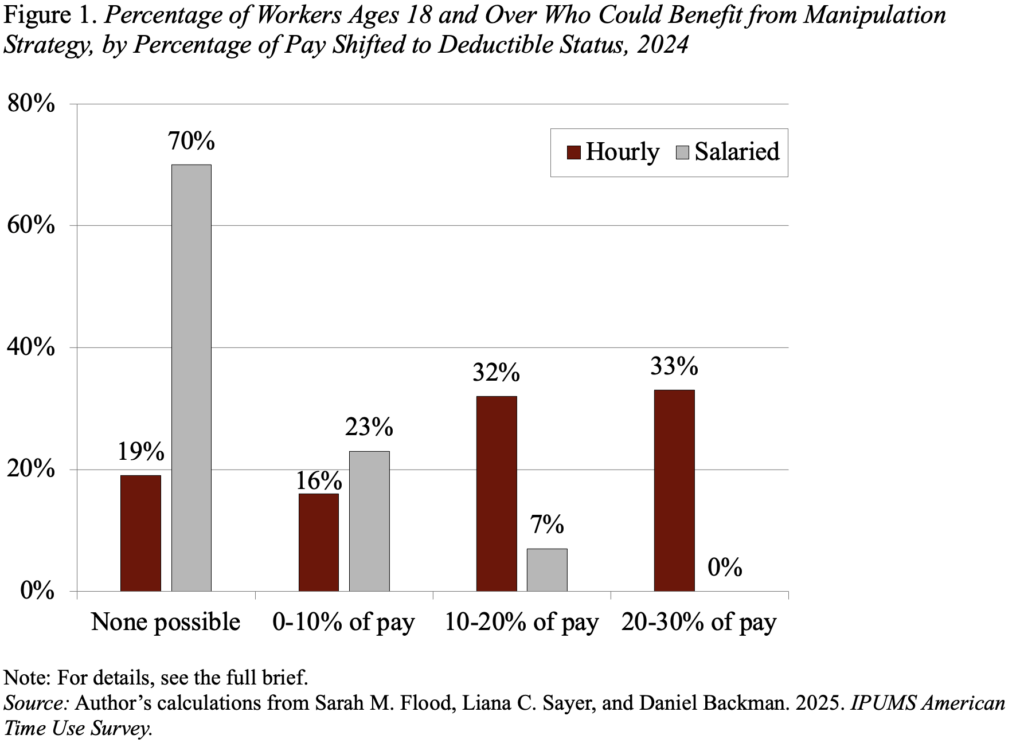

For hourly workers, employees and employers could agree to reduce the worker’s base wage to their state’s legal minimum and make up any difference in compensation through extra hours of fake “overtime.” For salaried workers who already exceed 40 hours a week but were declared exempt from overtime receipt, employers could agree to stop asking for overtime exemptions in exchange for lower base pay. While both these approaches would almost certainly run afoul of labor laws, the OBBBA has introduced a temptation that simply wasn’t there before. Given that the Treasury Department is already seeing excessive overtime claims, it’s worth asking: how common might that temptation be? Figure 1 shows the share of hourly and salaried workers who currently don’t receive overtime that could take advantage of these approaches, grouped by how much of their income they could shift to tax deferral.

The figure shows that over 80 percent of hourly and 30 percent of salaried workers could benefit from the manipulations. Indeed, a third of hourly workers could benefit substantially, shifting 20 to 30 percent of their pay to tax-deferred “overtime.” Taken together, nearly 60 percent of workers could benefit from these strategies.

Is such manipulation likely to happen? Certainly, these strategies would require both employers and employees to break the rules. Then again, the Internal Revenue Service – which will ultimately enforce those rules – has lost a significant amount of its workforce to resignation and cuts during the Trump Administration. With the cost of government debt being as high as ever – and the conflict in the Middle East hardly helping – keeping an eye out for money lost inappropriately to the OBBBA overtime deduction would be wise. If not, it will have to be made up sometime by more honest taxpayers.