How to Calculate Tax Expenditures for 401(k) Plans

Alicia H. Munnell is a columnist for MarketWatch and senior advisor of the Center for Retirement Research at Boston College.

As noted in last week’s blog post, contributions to 401(k) plans are treated favorably under the federal personal income tax. The government does not tax either the employee or employer contributions to these plans or the investment earnings on the contributions until the monies are withdrawn in retirement. In addition, deferral shifts income to a time of life when people have less income and thereby face a lower tax rate. This treatment significantly reduces the lifetime income taxes of those employees with 401(k)s and costs the Treasury money. The question is how much?

The calculation involves comparing the present discounted value of taxes collected from saving within a 401(k) plan to how much would have been collected if the saving were done outside. Several pieces of information are needed: the amount contributed to 401(k)s, the rate of return earned on investments, the rate used to discount future values to the present, the length of time the money is held in the 401(k), and the average marginal tax rate before and after retirement.

Assume that the rate of return equals the discount rate and that, for the moment, all income is taxed at the same rate. If contributions to 401(k)-type plans – hereafter referred to simply as 401(k) plans – are $280 billion, contributors are age 45, the money is withdrawn at 75, the nominal rate of return is 6 percent, and the average marginal tax rate is 25 percent, the tax expenditure for 2010 would be $73 billion.

This initial estimate is too high, because the value of tax preferences for 401(k) plans depends on the tax treatment of investments outside the 401(k) plan. In fact, the maximum rate on realized capital gains and dividends is 15 percent. The following exercise assumes that the one-third of 401(k) assets held in bonds is taxed at 25 percent and the majority of the two thirds held in equities is taxed annually at 15 percent (the remaining portion is taxed only once at withdrawal at age 75 at 15 percent).

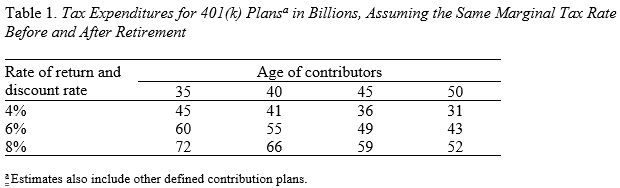

As shown in the Table 1 below, the fact that realized capital gains and dividends are subject to lower rates reduces the value of the tax expenditure. Assuming a 6-percent return and contributors are age 45, the tax expenditure falls to $49 billion.

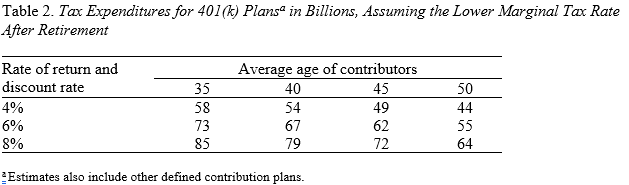

One more factor needs to be taken into account – namely, for a given tax structure, taxpayers may face a lower marginal rate in retirement than when working. Assuming the average marginal rate for 401(k) participants drops from 25 percent to 20 percent, the tax expenditures for different contributor ages and rates of return are shown in Table 2.

One could argue that tax rates are going to have to increase in the future so taxpayers may not see lower rates once they stop working; in this case, focusing simply on the value of deferral reported in Table 1 may be more reasonable. But if lower rates are included in the calculation, the tax expenditure in the case where contributors are age 45 and the rate of return and discount rate are 6 percent was about $62 billion in 2010.