FOLLOW THE BLOG

Filter

Paid Sick Time Wins on Ballots

In last Tuesday’s election, voters in Massachusetts and three cities – Oakland, California, and Montclair and Trenton, New Jersey – approved paid sick time initiatives that benefit working mothers in particular. These election results come on the heels of a slew of similar initiatives approved in the past year covering all or certain groups of workers in California and in San Diego, Washington, DC; Eugene, Oregon; several New Jersey municipalities; and the Tacoma suburb of SeaTac, according to an inventory of sick time laws compiled by the advocacy group, A Better Balance. Mandated paid sick time for employees is growing in popularity but is still unavailable to significant numbers of working mothers, who, the data show, are more often responsib…

November 11, 2014

Taxes and Social Security Progressivity

Social Security’s old-age pensions were designed to replace more of the earnings of retired low-wage workers than of higher-wage workers. But how is this progressivity affected by the federal income taxes paid by all workers and retirees? A study by economists at the Center for Retirement Research, which sponsors this blog, analyzed this complex issue and found that income taxes have not had any real impact on the overall progressivity of the Social Security program. To reach this conclusion, the researchers used the actual experiences of older American households contained in survey data linked to their lifetime earnings. There were several different tax effects to consider. First, the payroll tax that funds Social Security is shared by workers and employers,…

November 6, 2014

5 Signs of Financial Impairment

In a videotaped experiment testing her financial cognition, an elderly woman must prepare three utility bills for mailing. She’s seated at a table holding the bills, along with three filled-out checks, and three envelopes – each with one utility’s name on it. After considerable effort and confusion – checks paired with the wrong bills; bills placed into the wrong envelopes and taken back out – she finally finishes her task. New difficulty carrying out simple financial tasks or understanding financial concepts that were once familiar can be warning signs of cognitive impairment due to aging, early stage Alzheimer’s or other causes, said Daniel Marson, a neurology professor and director of the Alzheimer’s Disease Center at the University of Alabama, Birmingham…

November 4, 2014

Strange Influences on Financial Decisions

It would be nice to think that careful financial planning is behind the critical decision of when to start collecting Social Security benefits. But psychological traits – perhaps impatience or one’s fear of losing money – can also affect whether an individual claims his benefits right at age 62 or waits a few years to increase his monthly income from Social Security. A new study reveals another powerful influence that can jeopardize financial security: how a person’s dollar benefits might appear on the printed Social Security statement. Business professors Suzanne Shu at UCLA and John Payne and Namika Sagara at Duke University tested this on people over age 40, controlling for psychological influences on the research subjects, such as their…

October 30, 2014

How Emotions Meddle with Money

Our 401(k) retirement system requires most workers to save for the future. But it’s difficult to reach this increasingly important goal, because our emotions – overconfidence, pleasure, fear of loss – get in the way. “We believe our own nonsense,” is how Daylian Cane, a professor in the Yale School of Management, explains financial behavior in a new public television program, “Thinking Money: The Psychology Behind our Best and Worst Financial Decisions.” The short video above is taken from the program. Further clouding our judgment are a vast array of consumer products, and the stress produced by how easy it is to purchase them with a credit card swipe and how hard it is to pay off the cards. “Thinking…

October 23, 2014

Fraud Comes with Aging, Mental Decline

Sometimes research seems merely to confirm the obvious. One example is a new study showing that the cognitive decline that naturally comes with aging makes a senior more vulnerable to fraud. This isn’t especially surprising, but it is important. Amid a shortage of solid research about fraud among the elderly, this study provides important insight into how and under what circumstances they are increasingly being taken to the cleaners by scammers. In their study, Keith Gamble at DePaul University and researchers at the Rush University Medical Center used a survey of older Chicagoans known as the Rush Memory and Aging Project, which contains an unusual amount of information about aging, cognition, and financial fraud. In addition to measuring changes over…

October 21, 2014

U.S. Renters “Financially Fragile”

A new report by the FINRA Investor Education Foundation finds “a financially fragile renter population relative to homeowners.” It’s hardly surprising that apartment dwellers who rent are worse off financially than homeowners. It takes money to buy a house. But things got markedly worse for renters after the Great Recession. Millions of homeowners, foreclosed on by their lenders, were thrown back into the market for apartments, driving up rental rates and squeezing all renters. A new FINRA Foundation report, “American Renters and Financial Fragility,” dramatizes the growing rift between the nation’s haves and have-nots through a comparison of owners and renters. Click on “Learn More” below to see a FINRA Foundation chart contrasting the personal financial situation for renters versus…

October 16, 2014

A Thriving Underground Money Culture

Recent immigrants – whether from Mexico, Africa or China – often form groups that regularly contribute to a pool of money. Group members then take turns pulling out $500 or $1,000 in accumulated cash. These savings groups are one aspect of a pervasive underground money culture bustling beneath the surface in U.S. communities of immigrants and other low-income workers. Savings groups are one of four types of “informal” financial arrangements identified in a new report, “An Invisible Finance Sector: How Households Use Financial Tools of Their Own Making.” These arrangements create a strong social commitment to saving typically absent in the formal U.S. banking system. The four arrangements discussed in the report are: Savings groups, also known as lending circles,…

October 14, 2014

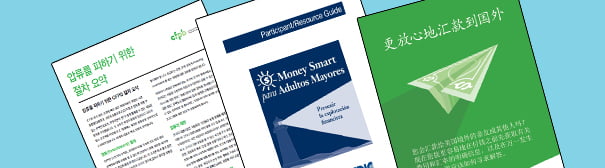

Financial Guides Come in Many Languages

The federal government has added two Spanish-language guides to its multilingual library printed in languages ranging from French to Tagalog, the language of the Philippines. The Spanish guides (previously available in English) – “Money Smart para Adultos Mayores” (“Money Smart for Older Adults”) and “Cómo Administrar el Dinero de Otras Personas” (“Managing Someone Else’s Money”) – teach seniors and their caregivers how to spot scams and frauds and help caregivers to understand their financial duties. They are all free of charge and published by the Office for Older Americans in the Consumer Financial Protection Bureau (CFPB). Other topics also appear in the CFPB’s online table of contents, which permits consumers and financial planners to search by language or by subjects…

October 9, 2014

Videos Critique Active Stock Investing

This is the sixth video featured in a series of seven that are worth watching. The new series, “How to Win the Loser’s Game,” takes viewers on an in-depth tour of the financial industry landscape while managing not to be dull. It includes a history of academic research in the finance field and examines the issue of paying high fees for active investment managers. The big message in the above video has also been covered on this blog: it’s virtually impossible for active managers to consistently outperform the overall market’s return. The solution: buy passive mutual funds and diversify. The evidence presented in the videos, sometimes by academic giants in the field, is compelling. Click here to watch the remaining…

October 7, 2014

Primer: Home Equity → Retiree Income

Americans who are 62 or older had an estimated $3.6 trillion in total equity locked up in their homes in the first quarter of 2014, according to the National Reverse Mortgage Lenders Association. A new primer suggests they should start thinking seriously about using it to generate some extra retirement income. The primer, published by the Center for Retirement Research at Boston College, which sponsors this blog, discusses two ways retirees can use home equity to generate income: by downsizing into a less expensive house or condominium or by taking out a reverse mortgage. Click here to read the booklet online and learn how these strategies work and how much money each can provide. Their pros and cons are detailed…

October 2, 2014

Debit Card Beats Cash as Budgeting Tool

Plastic or paper? Americans have spoken. In 2013, they made $4.1 trillion in purchases on their credit and debit cards, according to the Nilson Report – and that figure keeps marching upward. Some researchers view this as a dangerous trend. Plastic cards, they contend, put distance between a man and his bank account. Without the tactile sensation of handing over one’s hard-earned cash, it’s easy – too easy – to spend money and harder to save. New research out of The Netherlands has an entirely different take on the cash versus plastic debate. The study, based on a detailed Internet survey of nearly 1,500 Dutch people about their financial habits, shows that they view the debit card “as the better…