Trump Accounts for Newborns Are Nothing But a Diversion

Alicia H. Munnell is a columnist for MarketWatch and senior advisor of the Center for Retirement Research at Boston College.

Take a look at this state to see what a serious effort looks like.

With time on my hands, I was thinking about becoming the world’s greatest expert on Trump Accounts. On reflection, why should anyone spend more time on these accounts than the administration?

The lore is that these accounts, in their final form, were tossed into the One Big Beautiful Bill Act late in the game, with no expert oversight. If true, the product certainly reflects the process.

For those of you who have moved on, let me remind you of the details. Trump Accounts are a new savings account for children under age 18 that allows parents and employers to contribute up to $5,000 per year (indexed for inflation) on a tax-favored basis until the child turns 18. Money in these accounts must be invested in a low-fee index fund of primarily U.S. equities. In a separate initiative, the legislation established a pilot program whereby the federal government pays $1,000 into a Trump Account for babies born in the years 2025 through 2028. At 18, the child can withdraw the money.

The problem is that Trump Accounts further complicate our already-complex savings account system. We have at least 11 different tax-advantaged savings vehicles, with different rules, limitations, and regulations. Moreover, Trump Accounts are structured as a bizarre mix of Traditional and Roth IRAs, but with additional restrictions, such as virtually no ability to withdraw money before age 18. As such, Trump Accounts really do not provide any additional incentive to save. Anyone saving for a child’s education would use a 529 account, which offers more flexibility and tax benefits. Rather, the main attraction is the $1,000 initial deposit from the federal government.

And who is going to receive this $1,000? Those eligible are children born between Jan. 1, 2025, and Dec. 31, 2028, who are U.S. citizens with a valid Social Security number.

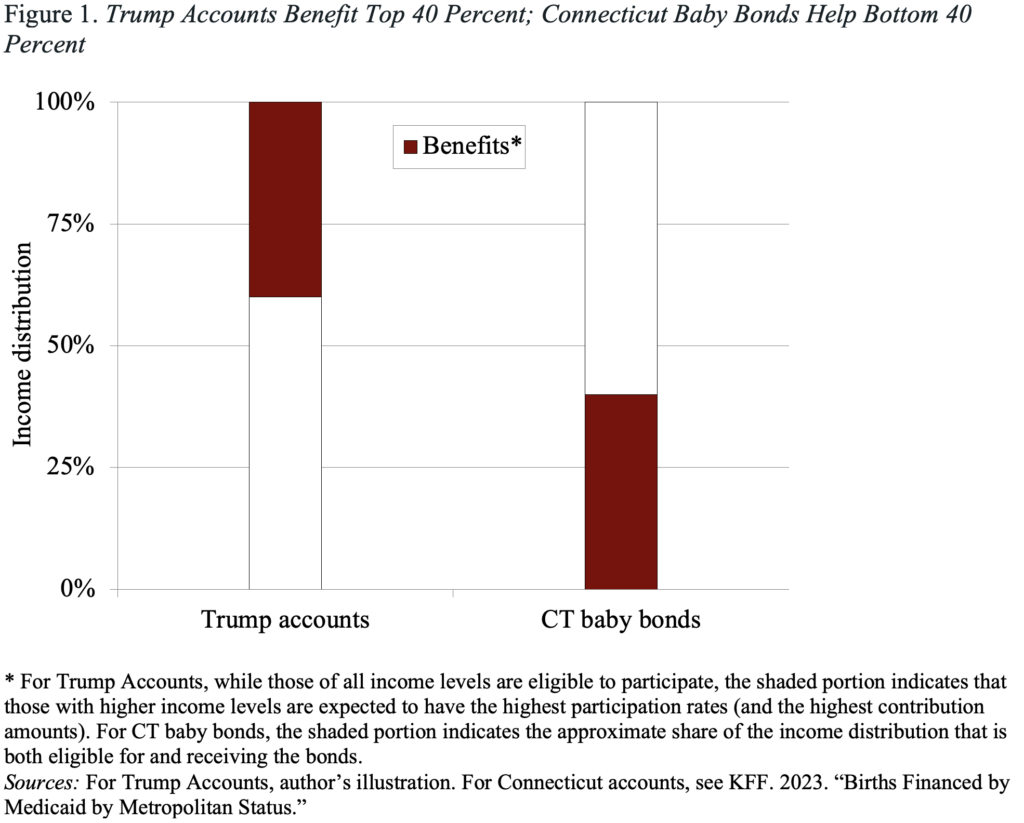

To sign up, parents or other adults must use IRS Form 4547, which means that many low-income households, who pay no federal income taxes, will not apply because they are less likely to interact with the IRS or have knowledge of this benefit. More generally, an extended literature shows that opt-in procedures, where individuals have to take the initiative, produce low levels of participation. An oft-cited example is Maine’s Alfond Grant program, which invests $500 in a scholarship account in Maine’s 529 plan. This program enrolled only 40 percent of qualified newborns until 2013, when it shifted to automatic enrollment. Under current arrangements, it’s reasonable to think that the Trump $1,000 payments will go to the top 40 percent of the income distribution.

In contrast, consider Connecticut’s Baby Bond program, which started in 2023 and is designed to narrow the wealth gap by directly investing in children from low-income families. To do this, the state automatically contributes $3,200 for each child born in Connecticut whose birth is covered by Husky Health, the state’s Medicaid program. The funds are invested by the Office of the Treasurer and can be withdrawn at age 18 to purchase a home in Connecticut, pay for higher education, invest in a Connecticut business, or contribute to a retirement account. Roughly 40 percent of births are covered by Medicaid. (See Figure 1.)

Of course, Connecticut’s program – like any real-life effort – is not perfect. Establishing eligibility based on Medicaid coverage means that many financially insecure households may be excluded. The amount, while substantially more than the federal contribution under the Trump Accounts, may not be enough to make a big impact. It could also be fragile politically – the costs occur today, but the benefits will not be evident for more than a decade. More generally, programs for poor people are always at risk. Perhaps – if such a program were enacted at the federal level – the brilliant idea of targeting Medicaid coverage could be combined with some opt-in option, perhaps with smaller stipends. Allowing taxpayers to see the program as universal might ensure longer-term support.

The bottom line is that the Trump Accounts are nothing more than a diversion from effectively helping lower-income households, and other people are out there doing meaningful stuff.