What Explains the Widening Gap in Retirement Ages?

Alicia H. Munnell is a columnist for MarketWatch and senior advisor of the Center for Retirement Research at Boston College.

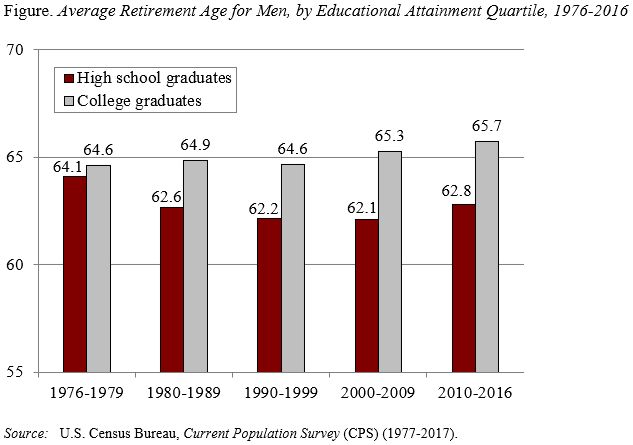

The increase in the average retirement age has been driven by those with more education.

Today, male college graduates retire about three years later than high school graduates (see Figure). While the story is more complicated for women because of the dramatic change in their labor force participation rates over the latter half of the 20th century, the pattern is similar.

A recent study by my colleague Matt Rutledge identifies three factors that have encouraged later retirement – better health, changing labor markets, and Social Security incentives – and shows how these developments have primarily impacted those with a college education.

Health. Health is one of the most important factors contributing to the retirement decision; it certainly is the single most important factor in earlier-than-planned retirement. The problem is that less-educated individuals have not seen the same improvement in health and longevity enjoyed by those with more education. Most of the gains in life expectancy have gone to the better educated, as well as disability-free life expectancy, which suggests that the less-educated also have less remaining work capacity.

Changing labor markets. Two factors related to the labor market have also pushed retirement ages higher in general, but may have a smaller influence on less-educated workers. The movement away from defined benefit (DB) plans has eliminated plan incentives to retire early and the shifting of investment risk to workers encourages defined contribution (DC) plan participants to keep working. But the transition to DCs may have had little impact on less-educated workers, who were less likely to have had DB coverage in the first place.

Meanwhile, the shift from manufacturing to service-sector employment has made jobs less physically demanding in general, which should enable workers to postpone retirement. But working conditions among less-educated individuals remain relatively poor; the less-educated are more likely to report that their jobs involve moving heavy loads, repetitive movements, and needing to stand all or almost all of the time.

Social Security Incentives. Since less-educated households are almost totally reliant on Social Security benefits, one would expect that they would respond most to changing incentives to work longer. Yet in the wake of the increase in Social Security’s Full Retirement Age (FRA), which reduces benefits at any given claiming age, the less-educated workers still make up the lion’s share of early retirees. One important reason is that less-educated workers stand to gain less from these incentives to work longer because of their shorter remaining life expectancy.

In short, although the overall average retirement age has increased by about three years over the last three decades, men with only a high school diploma have seen almost no change for several reasons. First, they have seen less of an improvement in their health and longevity than more-educated workers. Second, they were relatively unaffected by the shift from DB to DC plans and their working conditions still may not be conducive to extending careers. Third, delayed benefits may still not make sense for less-educated workers with shorter life spans.

The fact is, however, that working longer is perhaps the most effective way for Americans to improve their retirement security and should Congress continue to cut Social Security benefits at age 62 (by further increasing the FRA) working longer will become imperative for less-educated workers.