Why Do Workers Still Yearn for a Traditional Pension over a 401(k)?

Alicia H. Munnell is a columnist for MarketWatch and senior advisor of the Center for Retirement Research at Boston College.

A closer look at the Boeing negotiations only makes the question more puzzling.

Boeing workers recently accepted the company’s third offer. The agreement does not include reopening the Boeing defined benefit pension plan, which was cited as the major reason that the union rejected the second offer. Even though the strike is over, I find the fact that reopening the pension plan played such a prominent role in the negotiations really interesting.

After decades of thinking about retirement plans, my conclusion is that coverage is the major issue. A lifetime of participation in any type of employer-sponsored plan virtually ensures a secure retirement. In my view, the 401(k)/DB debate is a diversion.

Yet, the reopening of the pension plan was clearly important to Boeing workers. I can think of two reasons that might be the case: 1) the assumption that the employer pays for benefits under a defined benefit plan while the worker pays for 401(k) benefits; or 2) the compensation package under the Boeing defined benefit plan would have been higher than that resulting from the 401(k) arrangement.

No economist can accept the notion that the employer contribution to a defined benefit plan is an “add-on” that costs the employee nothing. Rather, the employer decides on a bucket of money that it can pay in total compensation – wages, health insurance, retirement etc. – and then allocates it among the various components to create the most desirable package. If employees make clear they want more employer contributions to a defined benefit plan, they will over time receive less in wages, health care, or other benefits. In other words, the employee pays regardless of whether retirement benefits are provided through 401(k)s or defined benefit plans.

The second issue requires comparing lifetime compensation with Boeing’s defined benefit plan and its 401(k) arrangement. The exercise proceeds in two steps, first comparing retirement income and then lifetime compensation under the two arrangements. The agreed-upon contract included provisions for both the defined benefit plan and for the 401(k):

- Defined benefit plan: In 2015, Boeing ended all benefit accruals for current and future hires, but some active workers still have credits in the plan. Boeing will increase the dollar per credited service (i.e., service earned before 2015) for all active workers from $95 to $105.

- 401(k) plan: Boeing will increase the employer matching contribution from 50 percent of the first 8 percent of an employee’s contributions to 100 percent. In addition, the company will make a supplementary 4-percent employer contribution program available to all employees (currently, it is only for those hired after 2015).

My colleagues JP Aubry and Yimeng Yin constructed a spreadsheet for workers at two salary levels based on the following assumptions:

- Salary: Growth 3% per year.

- Age: Starting at 35 and ending at 65.

- 401(k): Total contribution 20% (8% employee, 8% employer match, and 4% employer supplement).

- Defined benefit: Dollar per credited service $150 (reflecting a continuation of the growth in the credited amount between 2009 and the new contract).

- Rate of return: 6% and 4%.

- Annuitization of 401(k) balances (for comparability to defined benefit payment) based on immediateannuities.com.

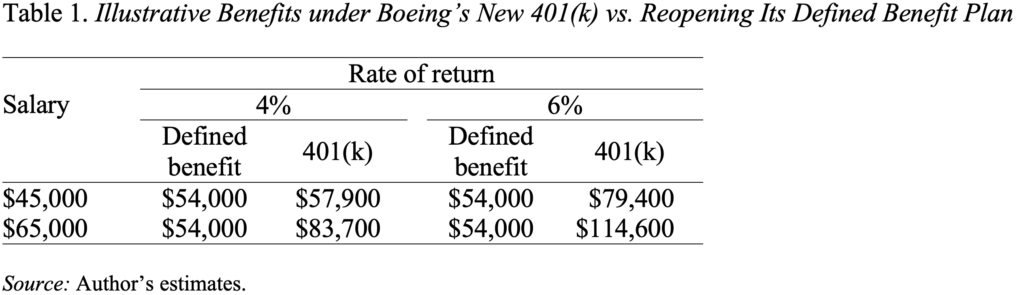

You can see the results for retirement income in Table 1. The pattern should not be surprising since the portion of compensation going to retirement is quite different under the two arrangements – 20 percent with the 401(k) and, say, a normal cost of 16 percent with the defined benefit plan. With more of the compensation going to retirement, retirement income in the case of the 401(k) is significantly higher.

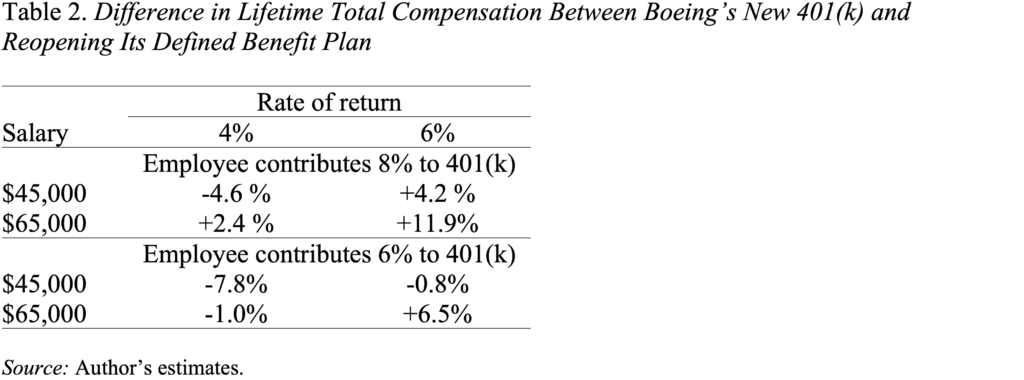

But that’s not the end of the story. Yes, retirement income would be lower under the defined benefit plan, but take-home pay would be higher. In fact, one would expect total compensation to be roughly the same under the two regimes because the employer views their wage and benefit package through the lens of total compensation. Indeed, our calculations confirm that the present discounted value of lifetime compensation is roughly equal under the two retirement arrangements. With a base case of $45,000, a 6-percent return, and the full 8-percent employee 401(k) contribution, the 401(k) plan is 4.2 percent better; drop that return to 4 percent and the results reverse (see Table 2). While the precise outcome varies with the salary, return, and contribution assumptions, the differences remain relatively small.

In my view, the exercise supports my sense that the way retirement income is provided – 401(k) plan versus defined benefit plan – is not that important. The big issue is whether employees have a retirement plan at work; without a plan, people simply do not save. It’s still not clear to me that – given inflation risk and a mobile workforce – traditional defined benefit plans trump 401(k)s.