Social Security’s Real Retirement Age is 70

Alicia H. Munnell is a columnist for MarketWatch and senior advisor of the Center for Retirement Research at Boston College.

The “Full Retirement Age” is lower, but no longer relevant.

Social Security’s retirement age is 70. The simple fact is that monthly benefits are highest at age 70 and are reduced actuarially for each year they are claimed before age 70. This is a relatively new development, which may explain why Social Security’s retirement age is the best kept secret in town. But I think it’s time we told folks. And then we need to clarify what all this talk about raising the so-called Full Retirement Age really means. (These issues are covered in more detail in a new issue brief from the Center for Retirement Research.)

Currently workers can claim their benefits at any time between 62 and 70. But benefits claimed before age 70 are actuarially reduced. That is, benefits claimed at younger ages are lower by an amount that compensates for the fact that they start earlier and will be paid for more years. The goal is to ensure that, based on average life expectancy, people who take a lower benefit early would expect to receive about the same total amount in benefits over their lifetimes as those who wait for higher monthly benefits but start receiving them later. In other words, the claiming age affects monthly benefits but, on average, does not alter total benefits paid over the lifetime.

So, we have a benefit structure that pays full benefits at an age when most people have stopped working. We have set that age at 70. If you claim after 70, lifetime benefits decline, because monthly benefits are not increased for claiming after 70. If you claim before 70, your monthly benefit is significantly lower.

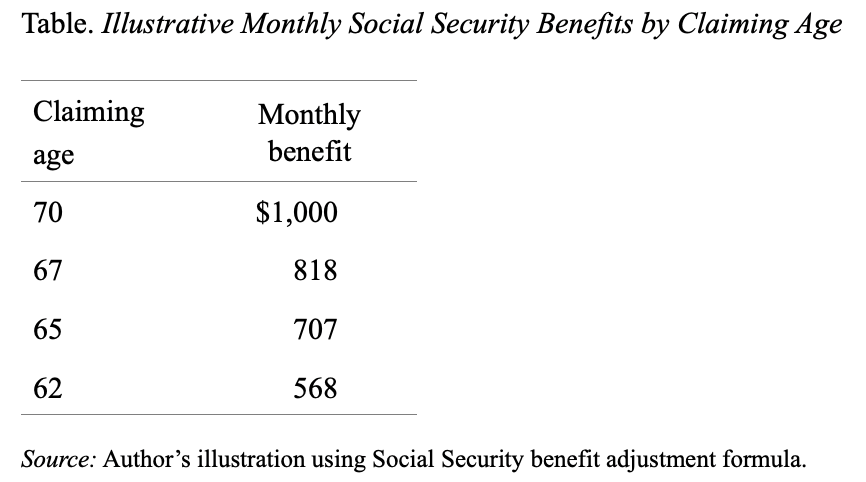

Most people don’t understand how much claiming early reduces monthly benefits. As the Table shows, claiming at 62 instead of 70 cuts the monthly benefit almost in half, from $1,000 to $568. Given that Social Security is a particularly valuable type of income – inflation adjusted and lasts for as long as you live – it generally makes sense to postpone claiming as long as possible to get the highest monthly amount, assuming you are in good health for your age.

If 70 is the age at which Social Security expects most people to retire and at which it pays the highest benefit, what is all this talk about the Full Retirement Age?

Social Security’s Full Retirement Age used to be a meaningful concept. Before 1972, maximum monthly Social Security benefits were paid at 65, and monthly benefits were not increased for claiming later. In 1972, Congress introduced a Delayed Retirement Credit, which increased benefits by 1 percent of the Full Retirement Age benefit for each year of delay. The result was that those who retired later got a little bonus for delaying. But a 1-percent credit did not come close to compensating for the fact that late claimers had to wait and would get benefits over fewer years. In 1983, the adjustment was raised to 3 percent and that percent was increased gradually to 8 percent in 2008. At this point, the adjustment provided by the Delayed Retirement Credit is actuarially fair – that is, it keeps lifetime benefits constant for those who claim after the Full Retirement Age. In doing so, the Delayed Retirement Credit has rendered the Full Retirement Age a largely meaningless concept. It does not describe the age when benefits are first available. That is age 62. It does not describe the age when monthly benefits are at their maximum. That is age 70. It really does not have any meaning in terms of an official retirement age.

This story does not completely wash because a number of specific Social Security provisions are linked to the Full Retirement Age. An earnings test applies before age 66 (the current Full Retirement Age) but not thereafter. Widow and spousal benefits are reduced if claimed before the Full Retirement Age and not thereafter. Workers can claim spousal benefits after their Full Retirement Age and then subsequently claim their own benefits.

But all these provisions are relatively small and do not undermine the basic fact that 70 is the age for full monthly benefits under Social Security. So then, what does it mean that the Full Retirement Age has moved from 65 to 66 and is scheduled to move to 67 for workers born in 1960 or later? And what does it mean to increase the Full Retirement Age beyond the 67 threshold already scheduled under current law? A topic for next time.