Social Security’s Reality Check – with a Side of Wishful Thinking

Alicia H. Munnell is a columnist for MarketWatch and senior advisor of the Center for Retirement Research at Boston College.

How demographics and recent tax laws are squeezing Social Security.

This year’s Social Security Trustees Report took a major step towards offering a more realistic assessment of Social Security’s financial status as the Trustees recognized that the fertility rate is not likely to rebound and that lower immigration and the GOP tax law known as the One Big Beautiful Bill Act will further cut revenues.

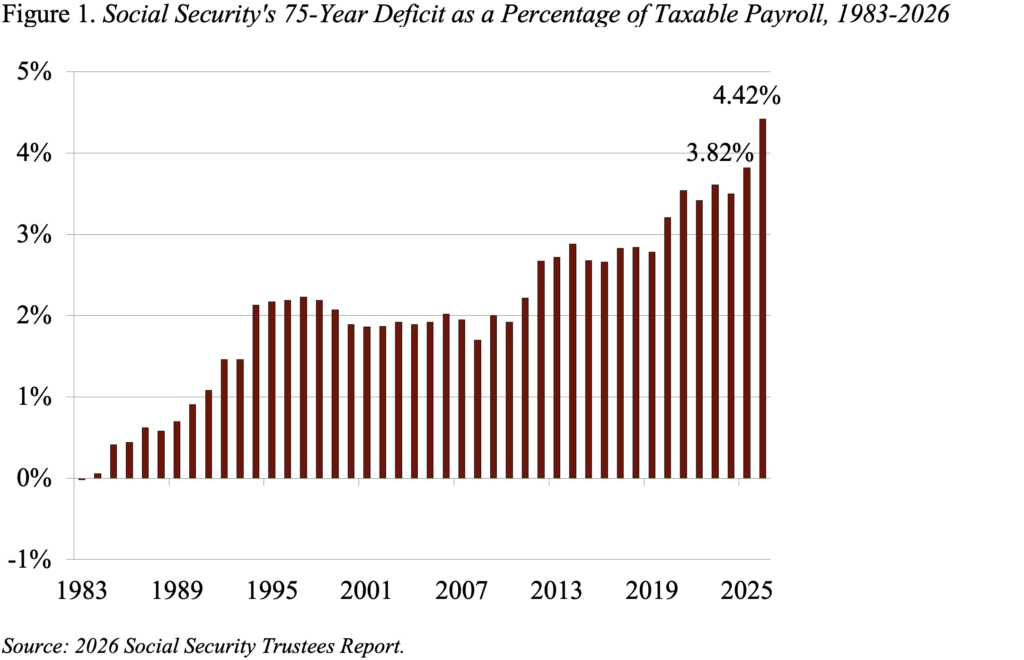

These lower revenues more than explain the increase in Social Security’s projected 75-year deficit from 3.82 percent to 4.42 percent of taxable payroll (see Figure 1). Unfortunately, the Trustees’ “offsetting” assumptions mask the full impact of their important changes. Thus, further deficit increases may be coming.

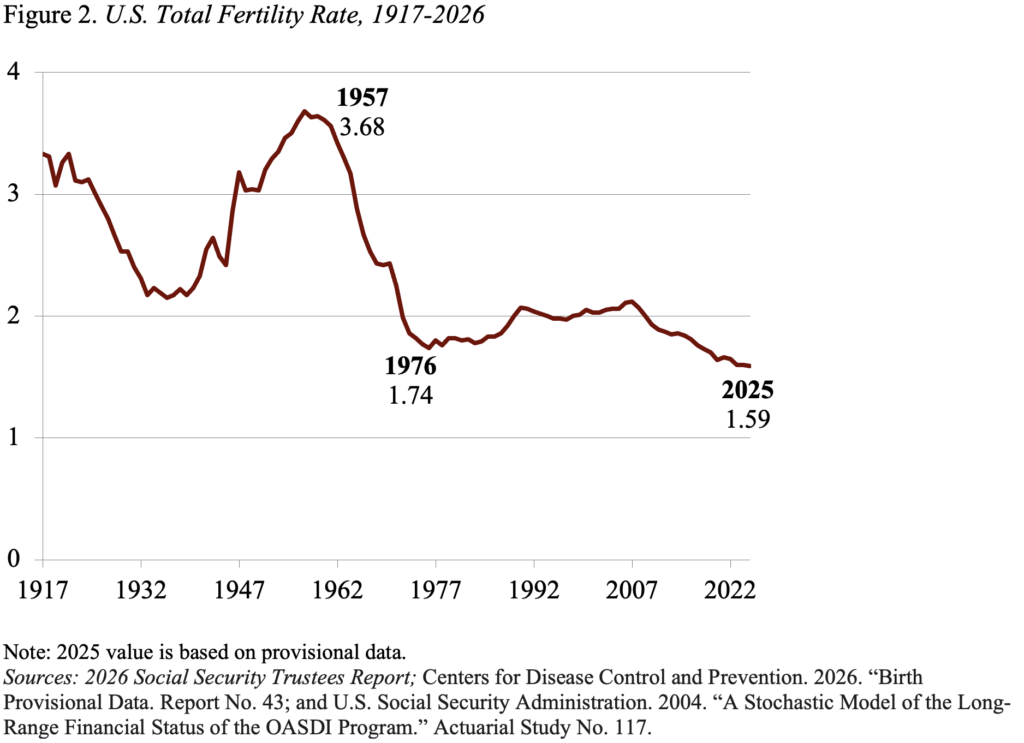

Fertility. The headline from the 2026 Trustees Report is the reduction in the fertility-rate assumption from an ultimate 1.90 children per woman to 1.75 children per woman. Fewer babies means fewer workers contributing to the system. While reducing the fertility rate assumption is a positive step towards presenting a more realistic picture of Social Security’s financial status, the question remains whether the Trustees have cut enough. Three factors suggest they have not: 1) the new assumed fertility rate is well above the current U.S. rate of 1.59 children (see Figure 2); 2) the current U.S. rate is still well above that in other developed countries, suggesting it will drop further; and 3) the Trustees’ assumption is well above that of the Congressional Budget Office (CBO) and the Census Bureau.

Immigration. The adjustments on the immigration side reflect the Trump Administration’s two-pronged initiatives. The first effort is to limit foreigners from coming into the country. While this effort is aimed primarily at illegal immigration, the Administration’s rhetoric and actions – such as barring foreign students – will likely also lead to less legal immigration. The second effort is to get rid of immigrants currently in the United States. Again, while the target is nominally illegal immigrants, news reports suggest some legal immigrants have gotten wrapped up in the effort. In addition, the Supreme Court’s decision in June allows the Trump Administration to move forward with ending Temporary Protected Status for nationals of Haiti and Syria and could affect those from other countries. The impact of fewer immigrants is very much like that of fewer babies – namely, fewer workers to a rapidly growing number of retirees.

The One Big Beautiful Bill Act (OBBBA). The final reason for the lower revenues is the OBBBA. This law made permanent the tax rates and tax brackets originally enacted in 2017. It also increased and made permanent the larger standard deduction of the 2017 Act, and added a temporary additional standard deduction for taxpayers over age 65. These changes reduce taxable income for many Social Security beneficiaries, who will pay less income tax on their Social Security benefits, which will result in lower revenue flowing to the trust fund.

Without any offsetting changes, these three assumptions (plus moving the valuation period and changing the methodology) would have had a very large impact on Social Security’s actuarial balance – reducing it by 0.81 percent of taxable payrolls, compared to the 0.60 percent actually reported. Not unreasonably, the Trustees looked for offsets. The two they landed on were: 1) a productivity improvement, which raises earnings and thereby revenues; and 2) a big increase in mortality, which means that retirees are not going to receive benefits for as many years as assumed in last year’s Report. Unfortunately, the case for neither change is very persuasive, and the Trustees are significantly more optimistic than CBO or Census.

Even with the remaining questions, however, the Trustees take us much closer to having a realistic measure of Social Security’s shortfall. Policymakers must have confidence in the size of the shortfall so that they believe that the changes they make will solve the problem. Defining the shortfall was the first step taken by the so-called Greenspan Commission when it began its deliberations to restore balance to Social Security in 1982.

Despite the larger deficit, the story remains the same. Social Security is the backbone of the retirement system, and Americans know and appreciate that. The changes required to fix the system are well within the bounds of fluctuations in spending on other programs in the past. Congress can fix this system, and it needs to head off a 22-percent cut in benefits in 2032. Numerous options are available on both the revenue and benefit sides to close the gap. All that is needed is the political will.