The Role of Information for Retirement Behavior: Evidence Based on the Stepwise Introduction of the Social Security Statement

Abstract

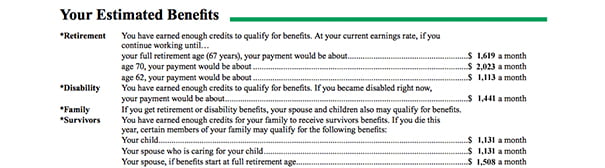

In 1995, the Social Security Administration started sending out the annual Social Security Statement. It contains information about the worker’s estimated benefits at the ages 62, 65, and 70. I use this unique natural experiment to analyze the retirement and claiming decision-making. First, I find that, despite the previous availability of information, the Statement has a significant impact on workers’ knowledge about their benefits. These findings are consistent with a model where workers need to gather costly information in order to improve their retirement decision. Second, I use this exogenous variation in knowledge to analyze the optimality of workers’ decisions. Several findings suggest that workers do not change their retirement behavior: i) Workers do not change their expected age of retirement after receiving the Statement; ii) monthly claiming patterns do not show any change after the introduction of the Social Security Statement; iii) workers do not become more sensitive to Social Security incentives after receiving the Statement. Either, workers are already behaving optimally, or the information contained in the Statement is not sufficient to improve their retirement behavior.

Mastrobuoni, . 2009. "The Role of Information for Retirement Behavior: Evidence Based on the Stepwise Introduction of the Social Security Statement" Working Paper 2009-23. Chestnut Hill, MA: Center for Retirement Research at Boston College.