The Stock Market Decline Is Undercutting Retirement Saving

Alicia H. Munnell is a columnist for MarketWatch and senior advisor of the Center for Retirement Research at Boston College.

With equities down 20 percent, participants have lost more than $3 trillion.

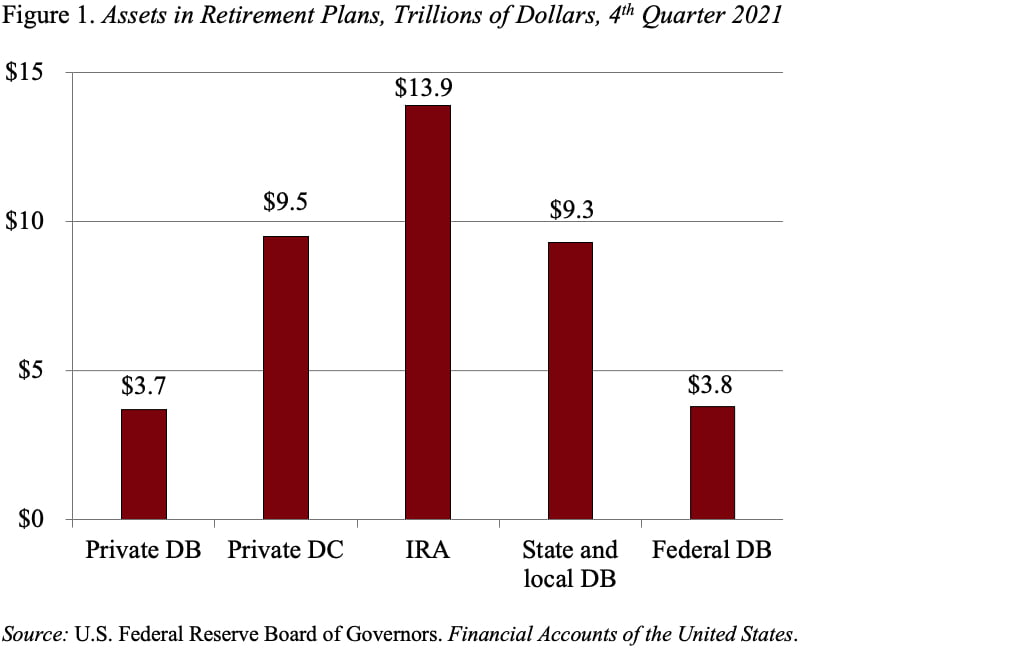

With the S&P 500 down about 20% since the beginning of 2022, it’s useful to consider how it affects the retirement savings of today’s workers. The shift from defined-benefit (DB) plans to defined-contribution (DC) plans in the private sector means that nongovernment workers have the bulk of their retirement saving in 401(k)-type plans or individual retirement accounts (IRAs) (see Figure 1). It’s important to include IRAs in the calculus because they are largely rollovers from 401(k)s. (Most state and local workers continue to be covered mainly by defined-benefit plans.) To the extent that the money in these private sector accounts is invested in equities, workers bear the full risk of stock market fluctuations.

Vanguard reports that 72 percent of the 401(k) plan assets that the company manages was invested in equities in 2020. Given the COVID stock market boom, the percentage might be slightly higher at the end of 2021. My best guess is that the asset allocation for IRAs would be about the same. Thus, a significant portion of retirement assets are at risk.

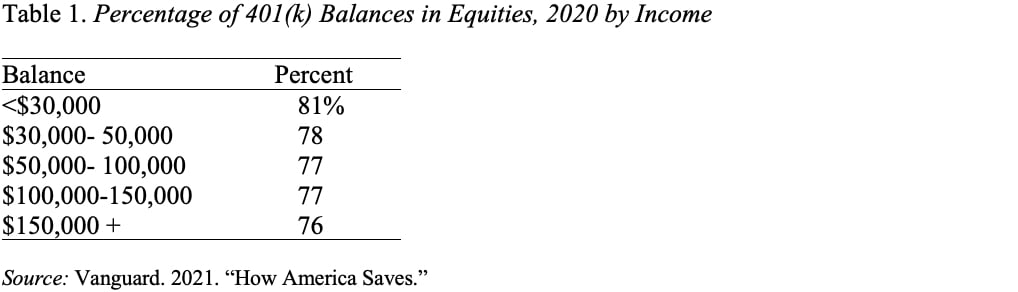

One question is who holds these assets. Again, the data come from Vanguard. In terms of income, it used to be that high-income participants took on more market risk – that is, invested more in equities – than their lower-income counterparts. However, with the rising use of target-date funds and automatic adjustment, lower-income participants actually have a slightly higher share of their assets in equities (see Table 1).

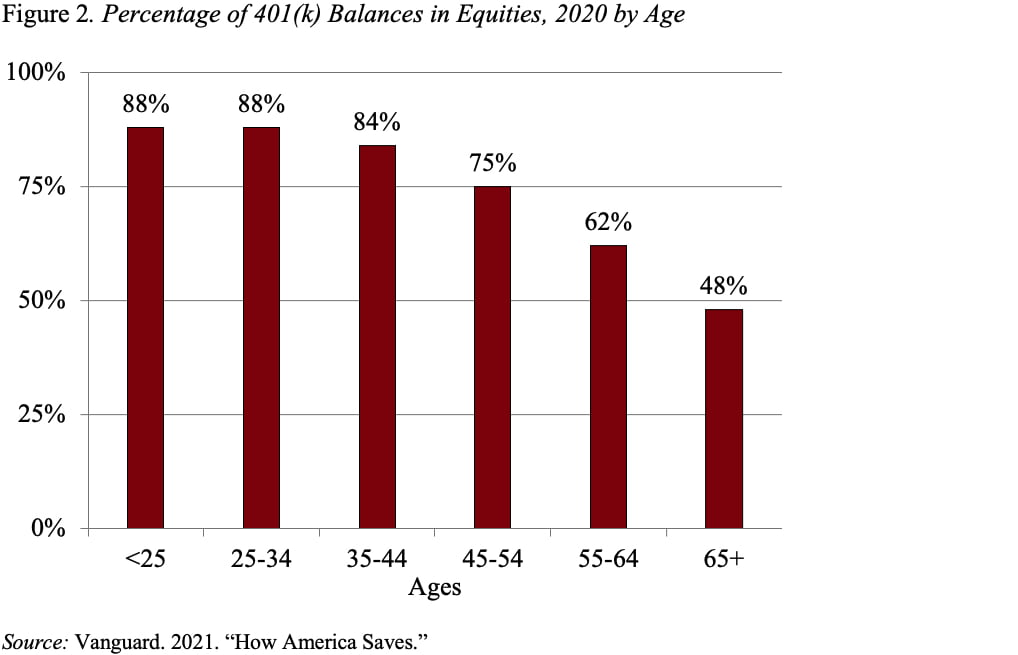

It is also important to understand which age groups are exposed to fluctuations in stock market values. If younger employees hold most of the equities, they would have time to recover and gain back losses before retirement. In terms of age, equity holdings do decline as participants age, but those 65 and older continue to hold almost half their portfolio in equities (see Figure 2). To the extent that these older individuals are forced to draw down their retirement assets, they will not have a chance to recover.

So, how much have people lost in their retirement plans during this market downturn? Assume the markets are down roughly 20 percent since January. Participants would have lost 20 percent of $6.8 trillion ($9.5 trillion x 72%) or $1.4 trillion in their 401(k)s; and IRA owners would have lost 20 percent of $10.0 trillion ($13.9 trillion x 72%) or $2.0 trillion in these accounts. Remember that IRAs are mostly 401(k) rollovers and therefore should be counted in the total.

One could argue that these recent losses are simply wiping out the extraordinary COVID gains, so that participants are not actually worse off than before the pandemic. But it’s human nature for people to feel like prior gains are theirs to keep, so the recent losses are painful.

People – mostly the wealthier – also hold equities outside retirement accounts. In 2021, these holdings amounted to $32.2 trillion. Applying the 20-percent decline means that people have lost an additional $6.4 trillion in direct holdings. These individuals, however, are much less likely to be forced to sell and can wait out the decline to recoup their losses.

We all know that the shift from defined benefit to defined contribution retirement plans has transferred longevity and investment risk from employers to workers. It is easy to forget this fact when the market is booming; hard to ignore when the market tanks.