Do Married Couples Coordinate Their Retirement Savings?

The brief’s key findings are:

- Employer 401(k) matches vary in generosity, so couples can get the most bang for their buck by prioritizing the more generous match.

- But, about 1 in 5 couples leave employer matching money on the table by failing to coordinate their contributions – forgoing $760 per year, on average.

- Half of forgone matches appear to be accidental; the other half reflect deliberate choices related to low marital commitment and/or misperceptions about how assets are treated in divorce.

- These findings suggest that employers and financial advisors could boost couples’ savings by alerting them to the value of coordination.

Introduction

Over two-thirds of U.S. private sector workers have access to a 401(k) or similar employer-sponsored retirement plan; and over four-fifths of these plans offer an employer “match” – an additional contribution that depends on how much the employee saves.1 Employer matches are among the most attractive incentives for retirement saving, offering workers an immediate return on their contributions. Yet because match schedules vary across employers, spouses in the same household often face different financial incentives for saving. Our recently published study in the American Economic Review, co-authored with Lucas Goodman, asks: do married couples efficiently allocate their retirement contributions across their retirement accounts?2 The answer matters because the most influential economic models of household decision-making assume that couples do coordinate, and because the failure to do so can meaningfully reduce the retirement wealth they accumulate.

Our key finding is that one in five couples fails to take full advantage of matching incentives, leaving an average of $757 per year on the table. This inefficiency does not appear to stem from inertia or from confusion about plan rules. Instead, many couples have never considered that coordination could help them and, among those who have, concerns about trust and control over their own accounts often prevent it. These results suggest that: 1) the presumption that households coordinate should be revisited; and 2) financial advisors and employers could help couples better coordinate their retirement savings by simply alerting them to the benefits.

This brief, based on our study, proceeds as follows. The first section describes how we define efficient allocation of retirement contributions and the new dataset we built to test it. The second section presents the results on the prevalence and cost of inefficient allocation. The third section investigates the underlying causes.

What Is an ‘Efficient’ Allocation of Contributions?

Match schedules for 401(k)s and other defined contribution plans vary by both the match rate (e.g., 50 percent, 100 percent) and the match ceiling (e.g., up to the first 6 percent of salary contributed by the employee). Consider a couple where one spouse’s employer matches contributions dollar-for-dollar up to a 3-percent cap, while the other spouse’s employer matches at only 50 cents on the dollar up to 6 percent. Maximizing the match at the couple level (our concept of efficiency) requires the couple to max out the more generous dollar-for-dollar match (i.e., the one with the 3-percent cap) before contributing to the less generous account. Failing to do so means leaving money on the table because the couple could increase their retirement wealth by reallocating any given amount of saving (i.e., without changing their current consumption). In our analysis, we refer to this untapped money as the “forgone match.”

Testing whether couples efficiently allocate their retirement contributions requires a dataset that links spouses together, records each spouse’s contributions, and measures the match schedule offered by each spouse’s employer. No such dataset existed, so we built one.

The employer side of our data comes from the annual regulatory filings of over 6,000 defined contribution retirement plans, covering about 40 million employees. These filings describe plan features, including match schedules, vesting rules, and auto-enrollment provisions. The employee side comes from IRS tax returns, which allow us to link spouses together through joint filings, and from W-2 forms, which report each spouse’s contributions and identify their employer.

By linking these two data sources, we construct a matched employer-employee dataset covering approximately 500,000 couples. Our analysis sample – which is restricted to couples where at least one spouse contributes, at least one has access to a match, and both are fully vested – contains roughly 185,000 couples and spans the period of 2003-2018.

How Common Is Inefficient Allocation?

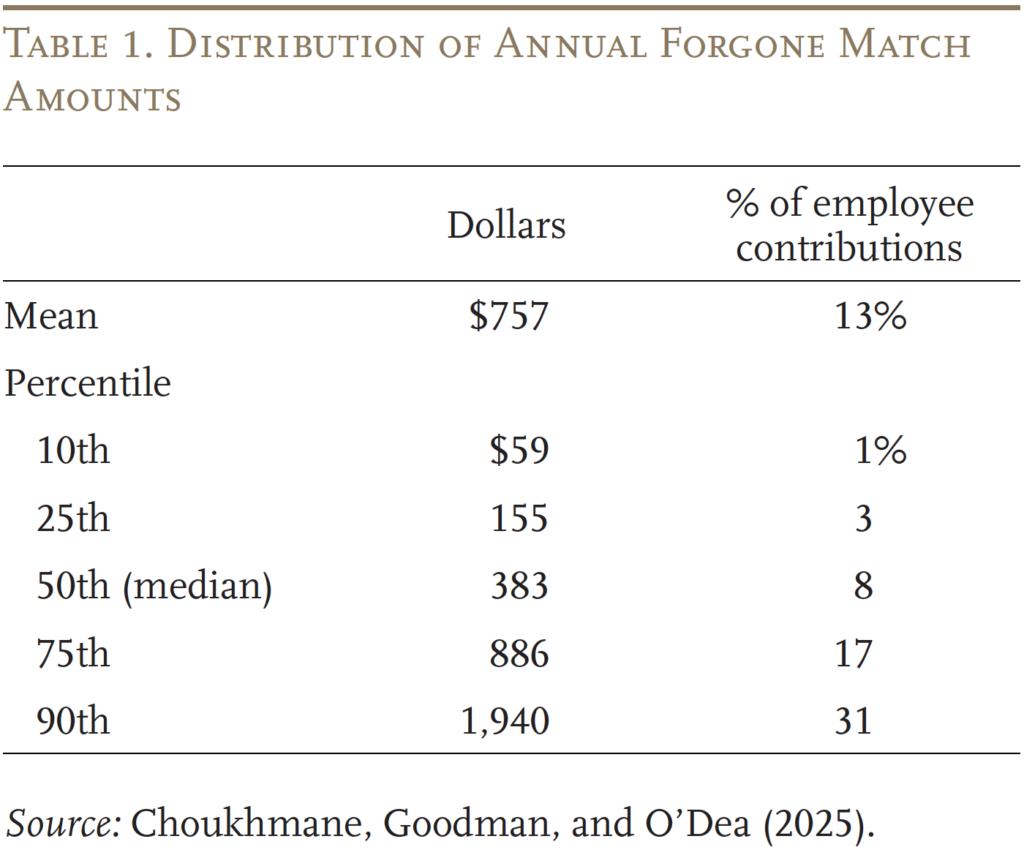

Using our novel dataset, we find that close to one in five couples (19.3 percent) fail to allocate their retirement contributions efficiently. These couples could receive, on average, an additional $757 per year in employer matching contributions (i.e., their forgone match) by simply shifting some of their existing savings from the account of the spouse with the lower match rate to the account of the spouse with the higher one. At the median, the annual cost is $383; at the 90th percentile, it reaches nearly $2,000. These are meaningful amounts: the average annual forgone match represents 13 percent of the couple’s total annual contributions to retirement accounts (see Table 1).

Forgone matches are also persistent and widespread. More than two in five couples with a forgone match still have one seven years later, and forgone matches occur across all income, age, and education groups, though they are somewhat less common among the highest earners and the most educated. The long-run cost is substantial: using a simple simulation calibrated to the patterns in our data, we estimate that the failure to coordinate can reduce retirement wealth at age 65 by an average of about $14,000 for all married couples, and by over $40,000 at the 90th percentile.

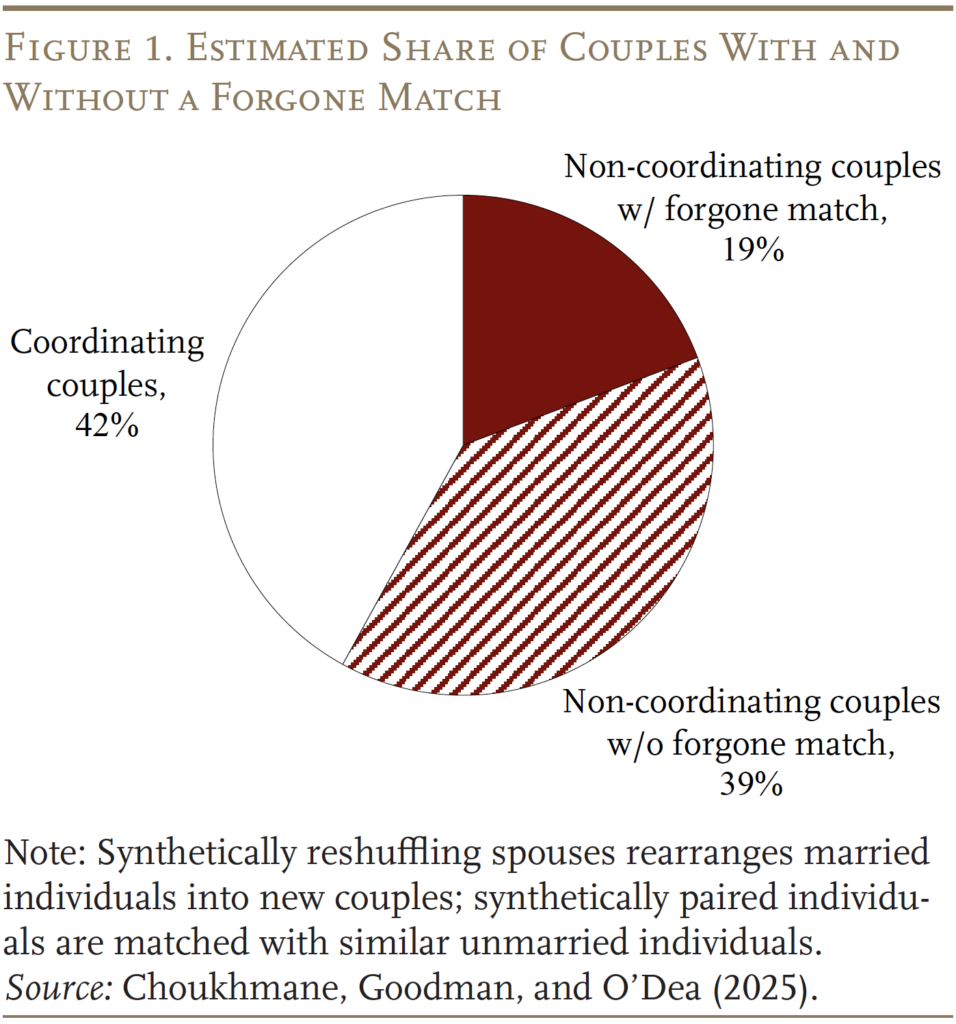

Importantly, focusing on just the couples who end up with a forgone match in our data represents a lower bound for the share of couples that actually fail to coordinate. The reason is that many non-coordinating couples will have no forgone match even if they are acting independently: for instance, if both spouses just happen to be fully exploiting their own employer match. So, to estimate how many couples are actually not coordinating, we construct a synthetic population of non-coordinating couples and estimate the share that have a forgone match.3 This exercise finds that one-third of non-coordinating couples end up with some forgone match. Comparing this number to the 19.3 percent we observe in real couples implies that about 58 percent of real couples (19.3/33.3 = 58) are not actively coordinating their retirement contributions (see Figure 1).

Why Don’t Couples Coordinate?

For the particular setting that we study, coordination should be easier to sustain than for some other financial decisions: the married couples in our sample are relatively well-off, the decision is repeated, and retirement account wealth accumulated during marriage is treated as a marital asset that is equally divided in divorce regardless of which spouse made contributions. Thus, understanding why so many couples persistently fail to coordinate is important both for how economists model household decisions and for any practical efforts to address the problem. We investigate this question using both our administrative data and a custom survey of 1,000 married individuals that asked respondents to divide a given level of savings between hypothetical retirement accounts (for themselves and their spouses) with different match schedules.

Simple Explanations Do Not Fit the Evidence

Using the administrative data, we find that several plausible explanations for non-coordination turn out not to fit the evidence. Inertia, the tendency to stick with a previous decision, is a well-documented force in retirement saving, but it does not explain what we find. Among couples where both spouses actively changed their contribution rates (i.e., were not subject to inertia), the incidence of forgone matches changes only modestly, and the couples are just as likely to move toward inefficiency as away from it. Similarly, auto-enrollment defaults are not the culprit: couples hired under opt-in plans show the same rates of non-coordination as those auto-enrolled. Nor can a simple heuristic of “save equal amounts” explain the results; we find that couples who equalize their contribution rates actually tend to have a smaller forgone match because equal saving mechanically reduces the chance that one spouse oversaves past their match cap while the other saves below their match cap.

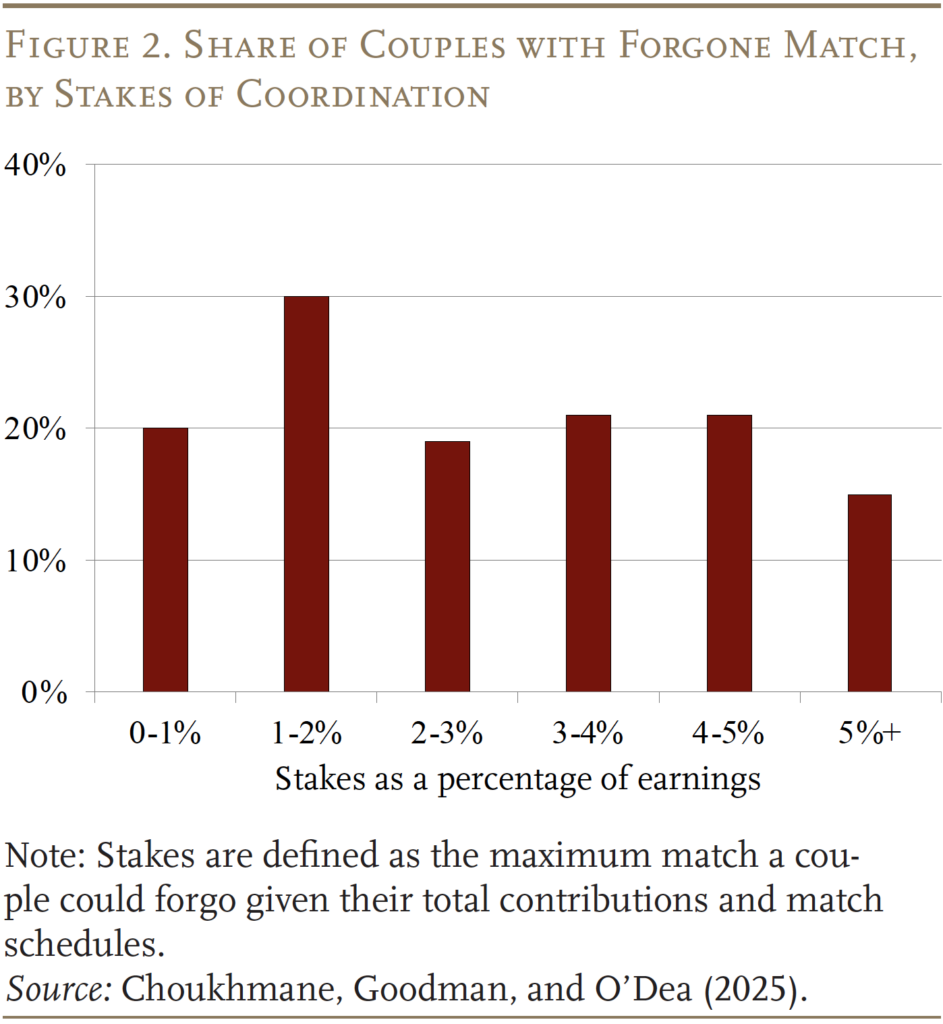

We also test whether rational inattention (the idea that it is not worth paying attention when the stakes are low) can account for our findings. This explanation does not look plausible either: the incidence of non-coordination is essentially flat even as the stakes rise to over $6,000 or 5 percent of household earnings per year (see Figure 2).

Accidental vs. Deliberate Non-coordination

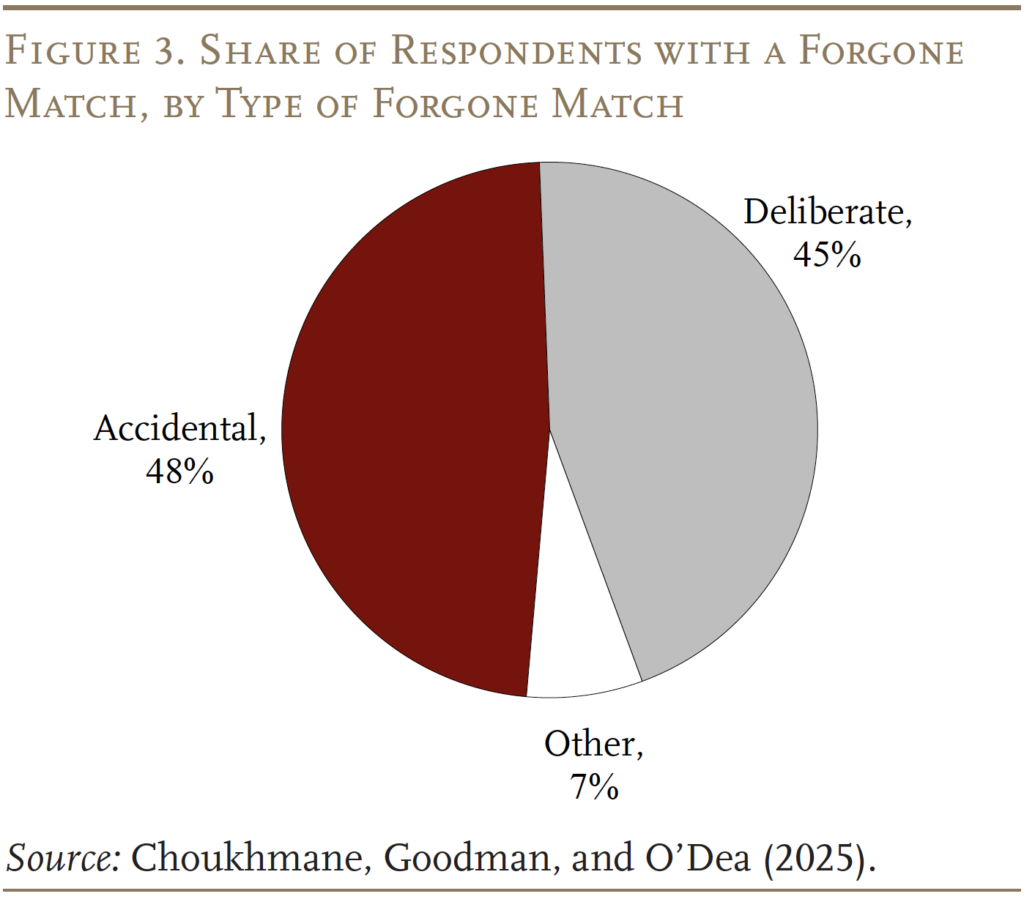

The survey allows us to go further, by asking those who did not allocate efficiently across the hypothetical accounts (40 percent of respondents) whether the choice was accidental or deliberate. The data suggest a significant portion of non-coordination is accidental: almost half of the survey respondents who chose a forgone match said they did not realize it (see Figure 3). This situation is likely explained by two factors. First, many have simply not thought about it – among survey respondents where both spouses have a retirement plan, over one-third reported they had not considered the possibility of gains from coordination.4 Second, financial literacy likely plays a role. In the survey, the incidence of a forgone match fell steeply with measured financial literacy: 64 percent of those answering two or fewer of five financial literacy questions correctly had some forgone match, compared to 25 percent of those answering all five correctly.

At the same time, the survey suggests that some non-coordination is deliberate: 45 percent of the respondents who chose an allocation resulting in a forgone match said that they knew they were doing so. Why would some couples knowingly leave match dollars on the table? Part of the answer appears to lie in the strength of couples’ marital commitment and, relatedly, in what couples think might happen in a divorce.

In our administrative data, proxies for marital commitment predict the likelihood of a forgone match. For example, couples who subsequently divorce are more likely to have a forgone match before the divorce; couples with a joint bank account before marriage, a mortgage, or children are less likely. Additionally, the incidence of a forgone match falls with the length of the marriage.5 At the same time, our survey suggests that many couples have misperceptions about divorce law. Across all U.S. states, retirement account wealth accumulated during marriage is a marital asset, so it is divided on divorce independently of which spouse made the contributions. Yet in our survey, over one-third of respondents believed they would keep their own retirement accounts in a divorce.6 And, these respondents were substantially more likely than others to deliberately forgo a match in the hypothetical experiment.7 For many of them, contributing to a spouse’s account felt like ceding control over those funds.8

Conclusion

Our findings have implications for both theory and practice. For the modeling of household decision-making, the widespread inefficiency we document challenges the common assumption that couples achieve efficient outcomes each period and suggests a greater role for non-cooperative models of the household. For policy and practice, the results point to a concrete and (perhaps) fixable problem. Much of the non-coordination we document appears to be accidental, driven by a failure to recognize that gains from coordination exist, compounded by low financial literacy and misperceptions about divorce law. Simply alerting couples to the potential benefits of coordinating their contributions could lead many of them to recover the forgone match. Employers could incorporate household-level thinking into financial wellness programs, and financial advisors working with married clients could make coordination of retirement contributions a routine part of planning. The broader lesson is that even among affluent, educated couples facing a simple and repeated financial decision with large stakes, coordination inside the household cannot be taken for granted.

References

Arnoud, Antoine, Taha Choukhmane, Jorge Colmenares, Cormac O’Dea, and Aneesha Parvathaneni. 2021. “The Evolution of US Firms’ Retirement Plan Offerings: Evidence from a New Panel Data Set.” Working Paper NB20-14. Cambridge, MA: National Bureau of Economic Research.

Choukhmane, Taha, Lucas Goodman, and Cormac O’Dea. 2025. “Efficiency in Household Decision Making: Evidence from the Retirement Savings of US Couples.” American Economic Review 115(5): 1485-1519.

Internal Revenue Service. 2024. “Population Files 1996-2022.” Washington, DC: U.S. Department of Treasury.

U.S. Department of Labor, Employee Benefits Security Administration. Annual Return/Report Form 5500 Series of Plan Years, 2003-2018. Washington, DC.

U.S. Department of Labor, Bureau of Labor Statistics. National Compensation Survey, 2025. Washington, DC.

Endnotes

- U.S. Department of Labor, National Compensation Survey (2025) and Arnoud et al. (2021). ↩︎

- Choukhmane, Goodman, and O’Dea (2025). ↩︎

- We calculate the prevalence in two engineered samples of synthetic couples that are similar to real couples, but for whom coordination is not possible. For the first sample, we rearrange actual married individuals into synthetic couples matched on observable characteristics. For the second, we randomly pair unmarried individuals who resemble the population of married workers. The prevalence of forgone matches was similar for both. ↩︎

- The household dimension of the decision is easy to overlook because retirement plans are individually managed and sponsored by one’s own employer. Consistent with this fact, the administrative data show that couples who work for the same employer are less likely to have a forgone match compared to couples who face identical match schedules but work at different firms. ↩︎

- These patterns hold conditional on a rich set of controls for household earnings, contribution levels, and plan characteristics. ↩︎

- About half of the survey respondents correctly believed that assets in retirement accounts were evenly split, and nearly one-fifth said they did not know how assets would be divided. ↩︎

- A regression analysis using the survey data shows that the belief that assets are not shared in divorce is significantly associated with the likelihood of knowingly making a sub-optimal allocation. This finding holds conditional on a rich set of controls that include respondent demographics, earnings, length of marriage – and, whether they have a mortgage, children, and joint bank accounts. ↩︎

- The narrative explanations that respondents gave were consistent with this interpretation. Three themes recurred. First, a desire for financial independence: one respondent wrote that they did not want to put their money in someone else’s account, “even if it is my husband.” Second, considerations of fairness: several respondents aimed to split contributions equally, regardless of the match incentives. Third, concerns about risk, including the risk of divorce: one respondent explained they would “rather hedge against this and pay a fee of lost money than have none at all if unforeseen circumstances happen.” ↩︎

Choukhmane, Taha and Cormac O’Dea. 2026. "Do Married Couples Coordinate Their Retirement Savings?" Issue in Brief 26-11. Chestnut Hill, MA: Center for Retirement Research at Boston College.