Two Simple 401(k) Lessons for New College Grads

One of the most fortunate events of my life was my first job after college at the Center for Retirement Research at Boston College (CRR). Not because of the salary — I think I earned less than $40K. What was fortuitous were the early lessons I learned about building toward a secure retirement.

Those lessons boil down to two simple but critically important points I urge you to share with any new graduate:

- Contribute to a retirement plan

- Invest aggressively

Simple, yes — but in a world of financial complexity, these two things do most of the heavy lifting toward long-term retirement planning.

My first project at the CRR was building a game where a fictional character named Sally makes financial decisions at different ages — how to invest, how long to work, and when to take Social Security. One key decision at each stage was how much to allocate between stocks and bonds. We modeled projected outcomes using decades of historical data.

Playing this game with volunteers revealed two consistent findings. First, Sally fared better the more she allocated to stocks early in the game. Over long periods, stocks have outperformed bonds, albeit with tons of variability. The game only allowed decisions every 10 years, which meant Sally couldn’t panic during downturns, and staying invested paid off.

Second, consistent contributions mattered enormously. As we wrote in our findings 20 years ago, because Sally hadn’t accumulated much wealth yet, her annual contributions overshadowed investment returns in driving 401(k) growth early in her career.

Those lessons have stuck with me. I contribute regularly to my 401(k) and keep an all-stock portfolio, even at age 43.

Here’s my message to new grads: I know finances are hard early in your career. You may not be earning much, you likely have student loans, you want to save for a home, and you still want to go out and have fun. These are all competing claims on a small paycheck.

But please contribute to whatever retirement plan your employer offers. If your employer matches your contribution, like most companies do, try to contribute the highest amount that’s matched. The employer match is free money you can’t afford to leave on the table.

And invest aggressively. Worried about geopolitical turmoil, oil prices, or whatever the current fear du jour is? Let it go. Even though it might be terrible for workers and the economy more broadly, one of the best things that could happen to a 20-something investor is a market downturn. Even after the seemingly catastrophic 50-percent drop that occurred during the financial crisis in 2008, the stock market recovered within a handful of years.

The long-term average return on the U.S. stock market is about 10 percent (nominal) per year. Some years will be plus 30 percent and some will be minus 30. But that long-term average includes the Great Depression, the onset of World War II, the stagflation of the 70s, Black Monday 1987, the dot-com bubble, and the 2008 financial crisis.

That’s why I suggest you put as much as you comfortably can into your 401(k) and invest heavily in U.S. and international stock markets. The precise mix – large vs. small cap, value vs. growth, U.S. vs. international – matters less than simply being invested. If you’d rather simplify the decision further, a target-date fund works well. For example, a target 2070 fund currently holds less than 10 percent in bonds with the rest in global stocks. Shield your eyes, plug your nose, cover your ears, and stay the course.

Growth will feel painfully slow at first (we named our game Get Rich Slow for this reason). But compounding accelerates dramatically as balances build, and it’s hard to catch up if you skip the early years.

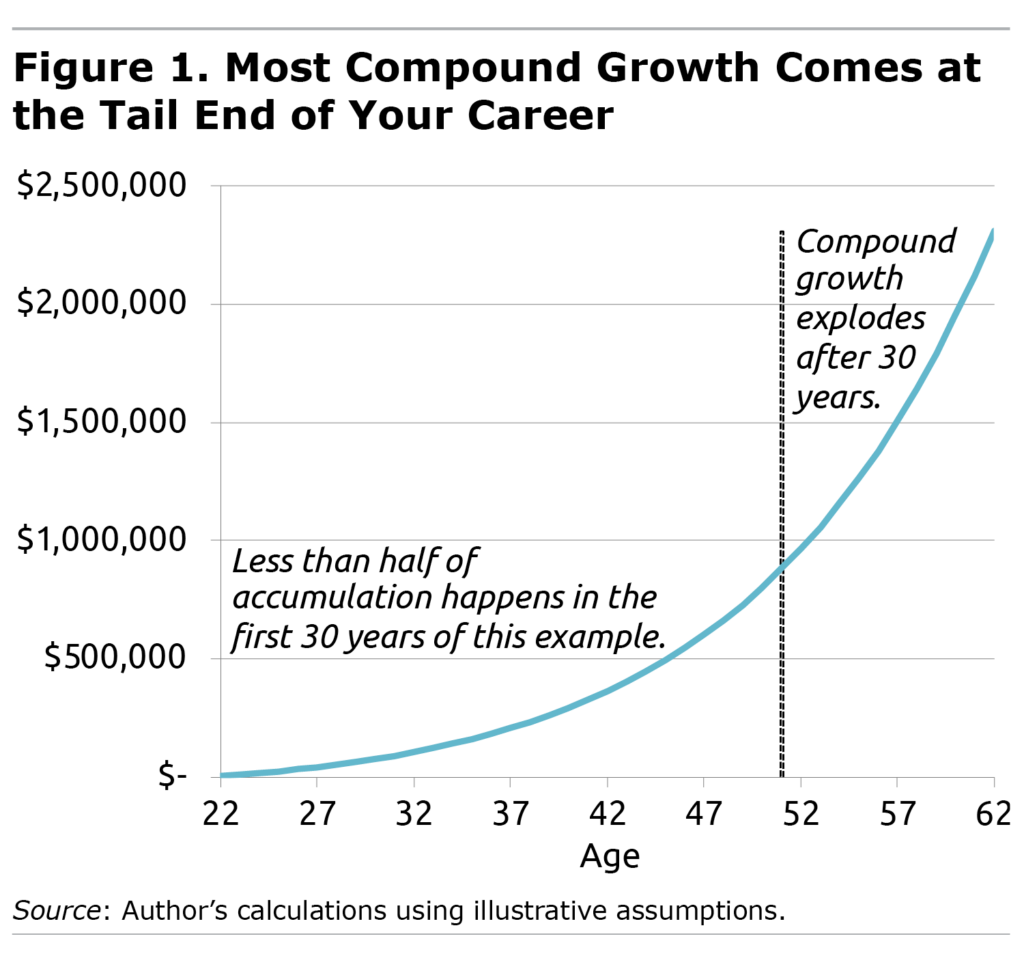

Say you’re 22 and contribute $5K per year, increasing your contribution by 5 percent annually, with a 7-percent nominal rate of growth (simple assumptions for the sake of illustration). At 31, your savings are still under $100K. At 45, they’re under $500K. Then compounding takes over: you have $1 million by 53 and $2 million by 61 (see Figure 1). None of that is possible without those early contributions.

The simple math is this. When you have $5K in your retirement account and it earns 7 percent, the growth is $350. Not exactly life changing. But when you have $2 million in your account and you earn 7 percent, the growth is $140,000.

The lesson from the CRR has never left me. If you are early in your career, or even if you are mid-career with 20-plus years until retirement, history says be aggressive and contribute early and often. It feels slow, but I’ve seen it work time and again, both in our research and in real life.

Luke Delorme, CFP® is Director of Financial Planning at Tableaux Wealth in Great Barrington, MA (www.tableauxwealth.com), reachable at luke@tableauxwealth.com. To stay current on the Squared Away blog, join our free email list.

This blog post is for informational and educational purposes only and should not be considered financial advice. Consult a qualified professional for advice specific to your situation.

Sound advice for the younger generation.

It truly is simple. Start young and dollar cost average with index funds via automatic payroll deductions. Don’t look at your balances with a stock market hit – as the article noted. View this as shares on sale.

40 years down the road you will be very happy.

I feel sad for folks who were consistent savers but parked it in old fashioned savings accounts or CD‘s.

The difference is truly staggering.

Do you have a recommendation for before or after tax? It seems like my children (mid 20’s) and their friends are choosing after tax? Back in the 90’s, when I started my 401k, I choose before tax. Now I owe a lot on what I have saved. The good thing is I can’t go and buy something big, like a summer home, because I’d have to pay all those taxes. So, there is sits growing and growing and growing……

Hi Colleen – great question. I get this one a lot.

There is no way to know for certain whether it is preferable to use pre-tax or after-tax (Roth) 401(k) contributions. It depends on our tax rate today as compared with the future. The future is unknowable because we don’t know how long we’ll live, what tax rates will be, and how much money we’ll have.

But…to the extent that current income is relatively low (as it tends to be for younger people), it makes a lot of sense to contribute to the Roth option. This also means you give up a tax benefit today, which is painful.

The practical answer for many people is to split contributions between pre-tax and Roth options. It’s what I do personally—I know it’s good to get $$ into Roth, but I also hate giving up the current tax break. So, I split it 50/50 pre-tax and Roth. It’s not too scientific!

What a GREAT idea, 50/50! Too late for me but I’ll run this by my sons. The best I can do is explain my scenario and compare it to what I see in their future. I can’t spend my money because I owe too much in taxes. When they get to 59.5 they can easily spend (and blow) their savings because they’ve already paid taxes. I grapple with this all the time.