Annuities in 401(k) Plans Aren’t All They’re Cracked Up to Be

Alicia H. Munnell is a columnist for MarketWatch and senior advisor of the Center for Retirement Research at Boston College.

Emergency expenses are eating up a lot of retirees’ money.

A few months ago, a colleague asked me what I thought about annuities in 401(k) plans. Before Harvard reclaims my Ph.D., let me lay out the merits of annuities. Annuities are contracts that provide a stream of monthly payments in exchange for a premium. The annuity not only protects people from outliving their resources but also allows more annual income than most could provide on their own, because the provider pools the experience of a large group of people and pays benefits to those who live longer than expected out of premiums paid by those who die early. Annuities also protect purchasers against the market risk associated with investing in stocks and bonds, and make people feel more comfortable knowing they will have regular income to cover their necessary expenses.

That said, my response to my colleague’s query about annuities in 401(k)s was tepid – at best. First, by design, they reallocate money from the low paid – who die early – to the high paid – who live forever. Second, my favorite financial advisor never recommends annuities because they are generally not indexed for inflation. Third, no good studies exist on how much retirees need to hold in assets for emergencies.

Interestingly, the Center has just released a study on the emergency expenses of retirees. To be fair, the authors are concerned about the size and frequency of emergency expenditures and people’s ability to cover these expenditures. They are not really focused on how many people have the assets to buy an annuity once they put aside a reserve for emergencies. Nevertheless, the study’s overall findings are interesting, and they do shed some light on the 401(k)/annuity issue.

The data come from the 2000-2020 Health and Retirement Study (HRS) and the accompanying 2001-2019 Consumption and Activities Mail Survey (CAMS). Based on these data, the authors calculate how much retired households spend annually on unexpected expenses in three broad categories: 1) “rainy day” expenses on house, car, and appliances; 2) family-related outlays to parents or children or in response to death or divorce; and 3) healthcare costs, including long-term care.

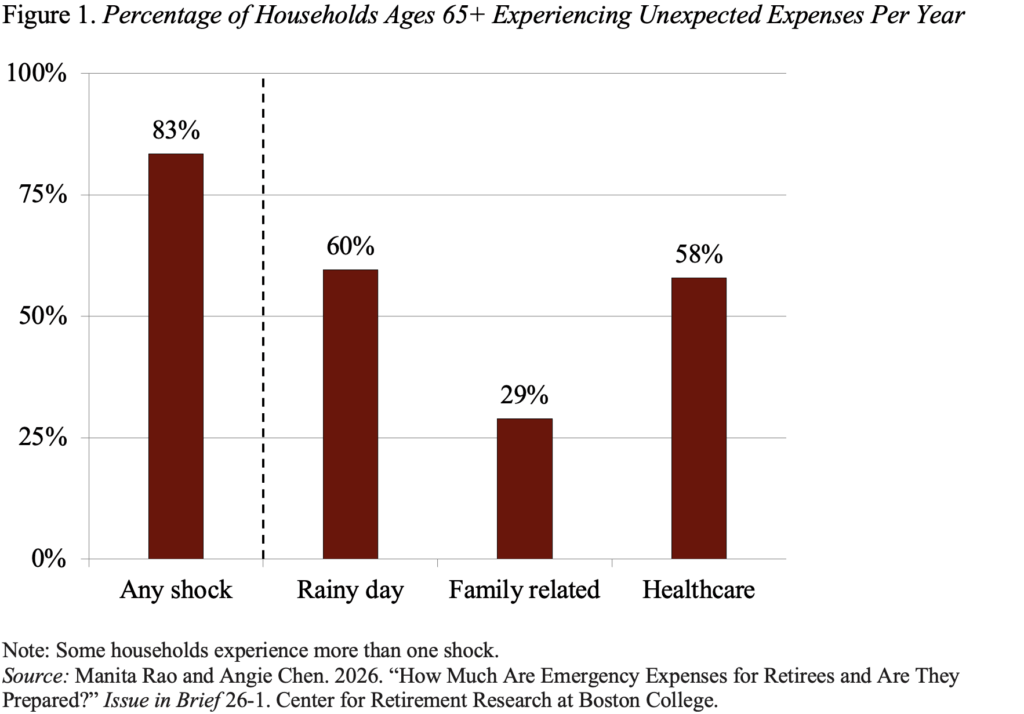

The results show that, in any given year, 83 percent of all households will experience some unexpected expense. About 60 percent of all households will face a rainy-day shock; 29 percent will have an unexpected family-related expense; and 58 percent will confront an unexpected healthcare expense (see Figure 1).

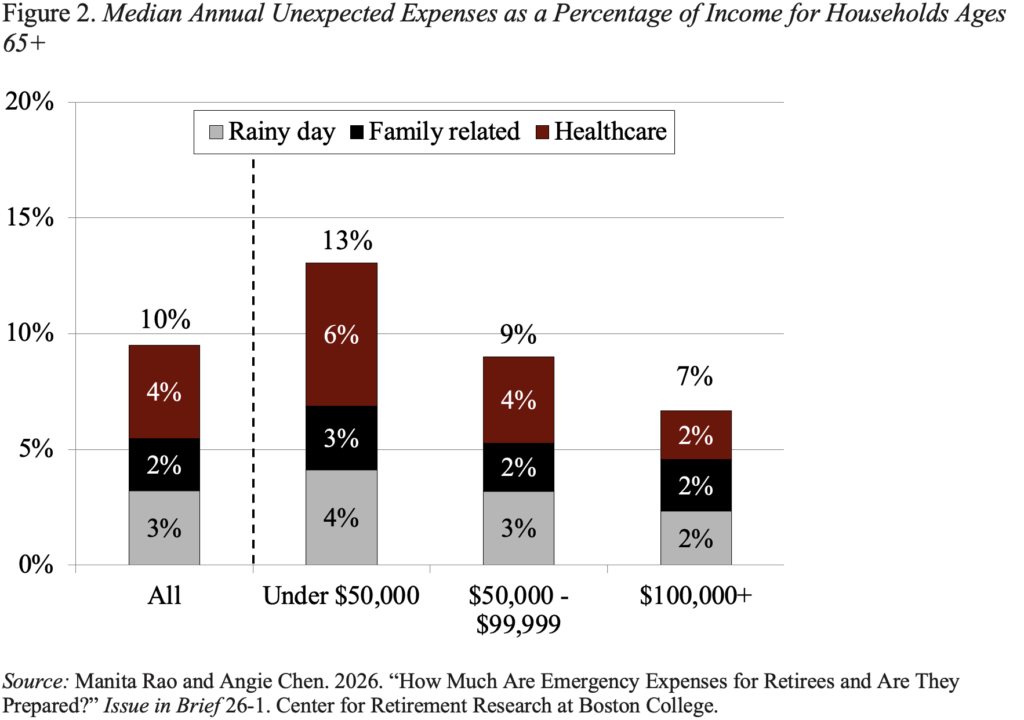

In terms of amounts, the findings also show that these unexpected expenses are significant. As shown in Figure 2, the typical household – in any year – is predicted to spend 10 percent of annual income on unexpected expenses. This number suggests that for a 25-year retirement, the typical household should put aside 2.5 times its average income as an emergency fund. Assuming an $85,000 average income, we are talking $212,500. For the top income group, the percentage of income is smaller (7 percent), but the income may be $250,000, so the required emergency fund could be $437,500.

The bottom line is, according to this much-needed new study, emergency expenditures are common and significant. In a given year, 83 percent of all households will face at least one type of spending shock, and on average, these unexpected expenses equal about 10 percent of annual income. To cover these expenditures over a 25-year retirement requires a fund of $200,000 to $400,000. The need for an emergency fund, combined with the fact that the very wealthy can self-insure against running out of money, limits the potential market for annuities. Data for 2022 indicate that only 28 percent of households have financial assets in the relevant range of $200,000-$5 million, where people can likely self-insure. With this limited market, annuities should not be a default investment in 401(k) plans.