Closing the Coverage Gap

The Problem

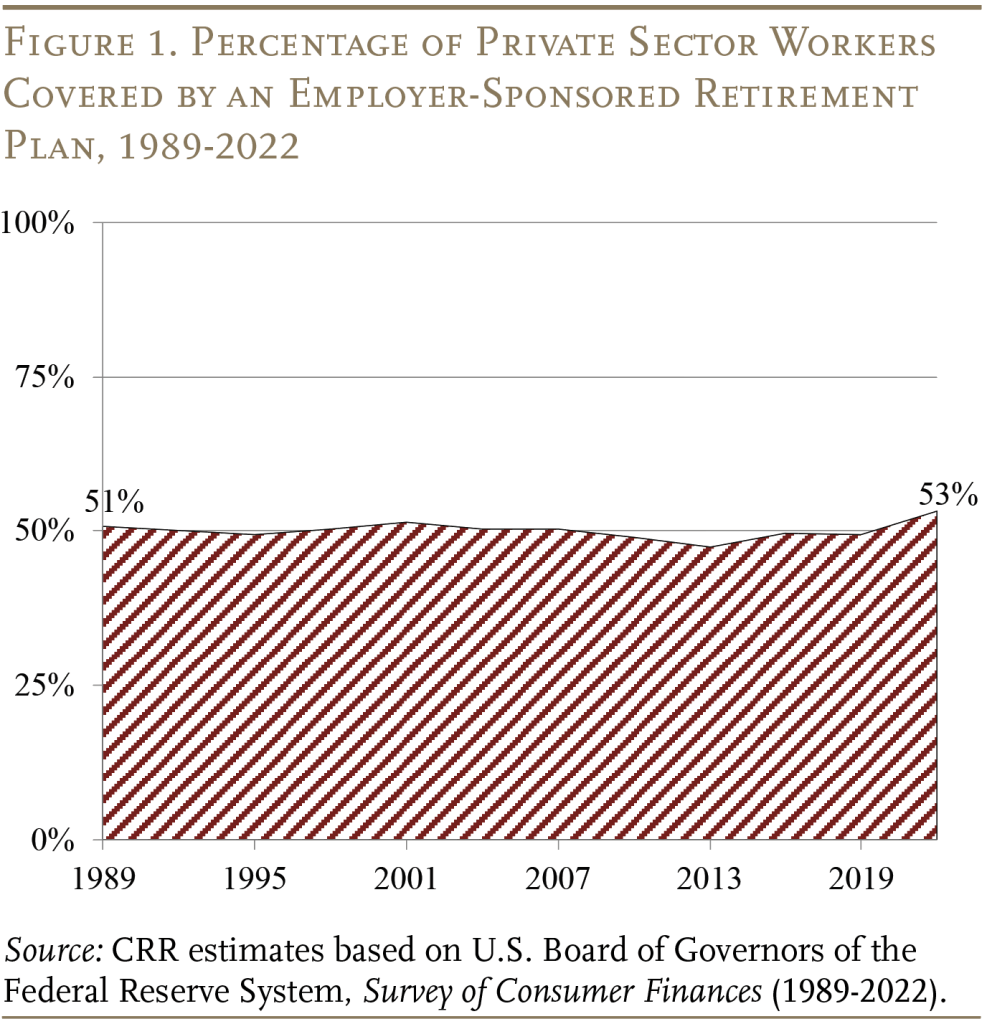

The main reason that U.S. workers end up with inadequate retirement savings is that, at any given time, only about half of private sector workers are covered by an employer-sponsored retirement plan (see Figure 1).

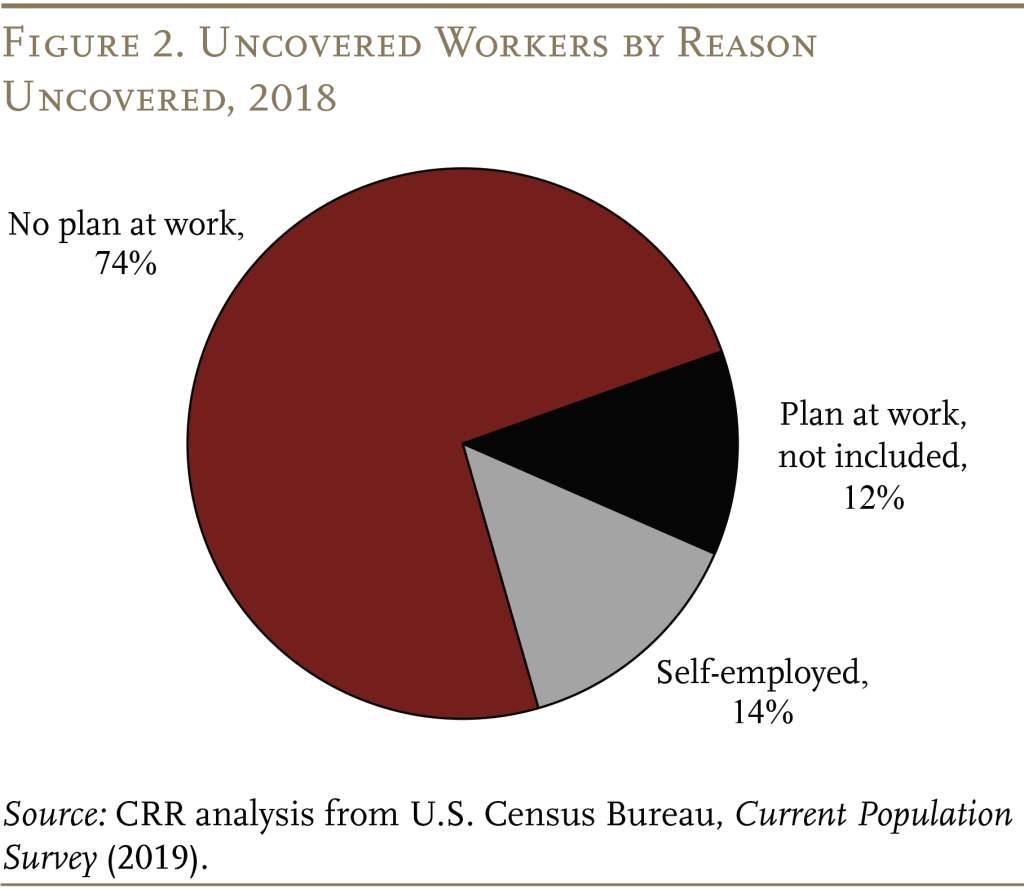

Workers can be uncovered in three ways: 1) their employer does not offer a plan; 2) their employer does offer a plan, but they are not included; or 3) they are self-employed. The first group accounts for three-quarters of all uncovered workers (see Figure 2). Initiatives to close the coverage gap generally focus on expanding coverage to the first group, but some also aim to eventually include the other groups.

Federal Initiatives

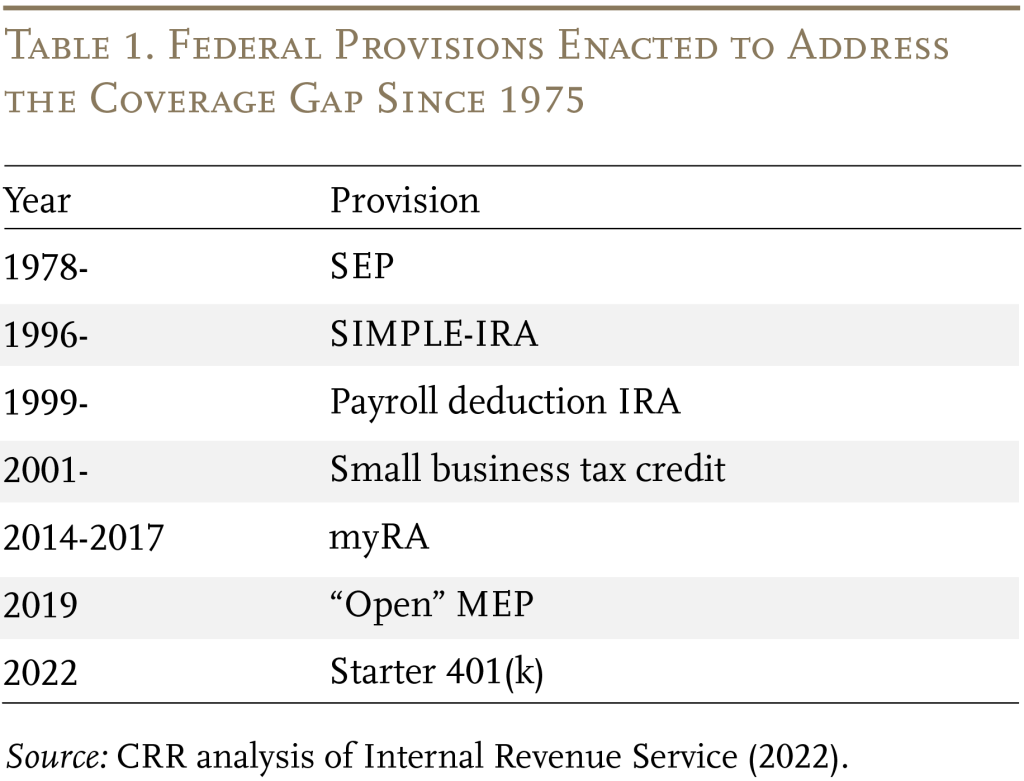

At the federal level, several initiatives to address the coverage gap have been enacted over the years (see Table 1). These programs have relied on the voluntary participation of employers and therefore have had little impact.

Learn More about Enacted Federal Provisions

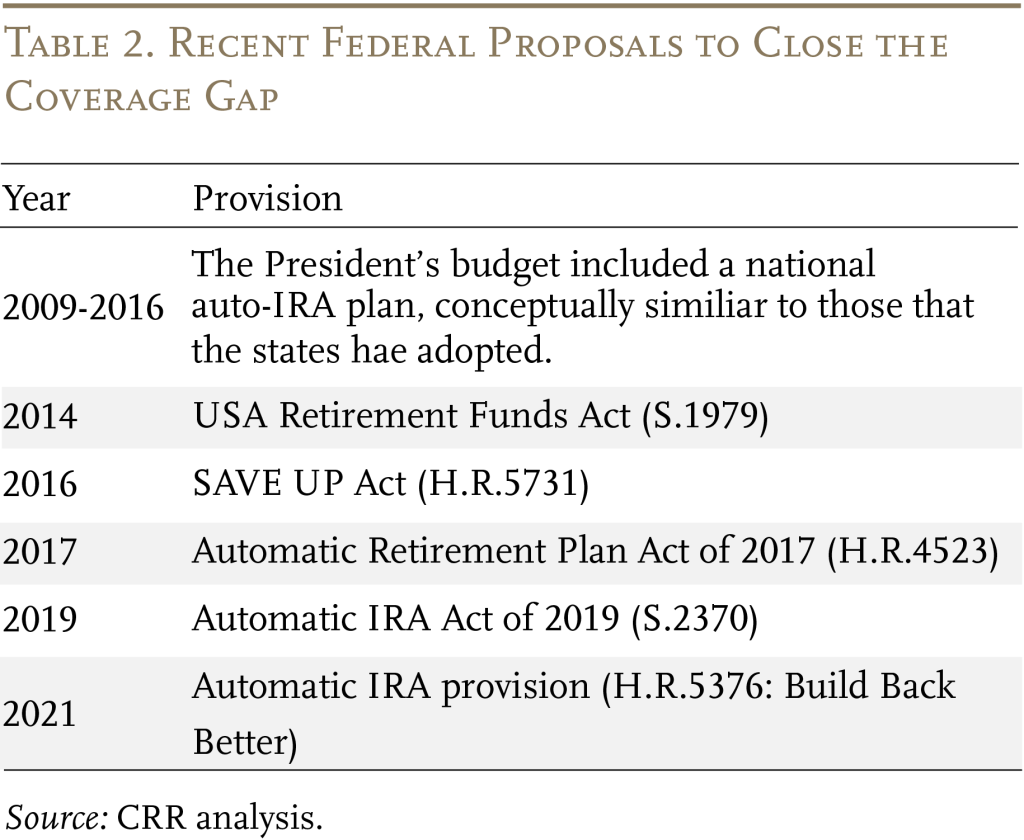

Legislative proposals for mandatory programs are more likely the answer (see Table 2).

Learn More about Federal Proposals

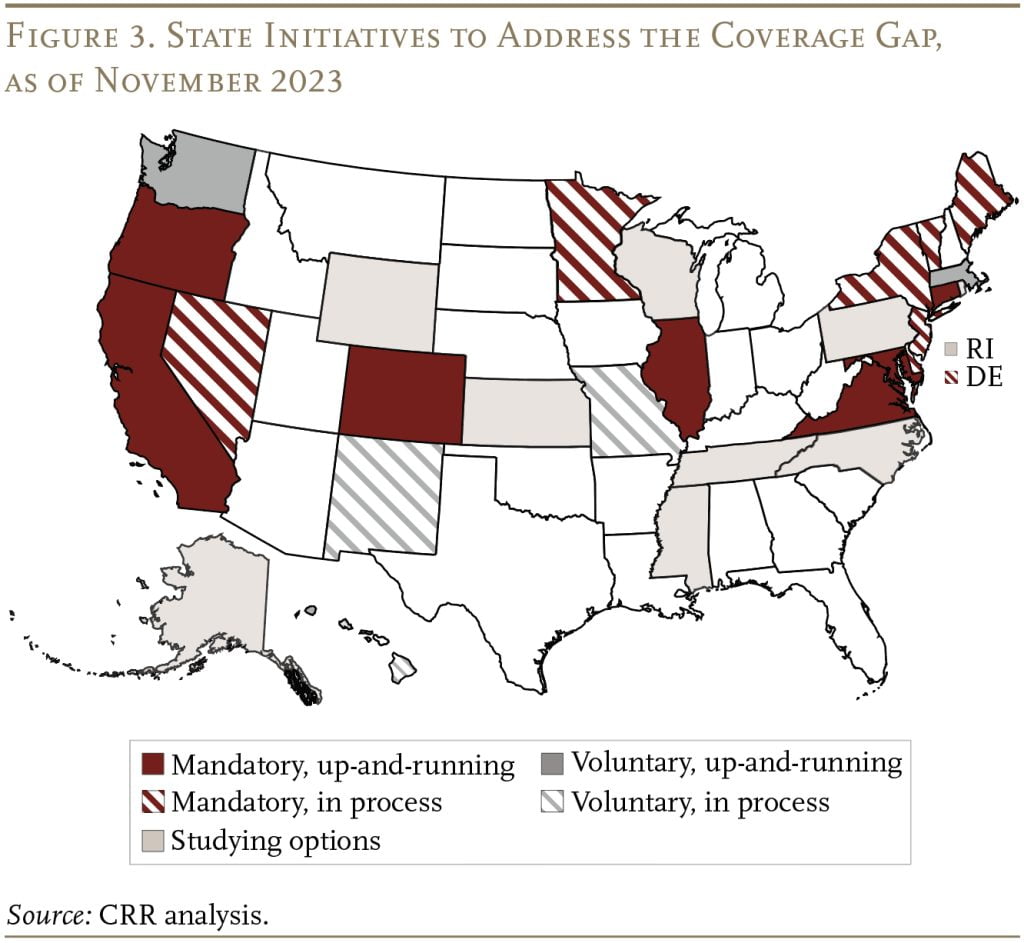

State Initiatives

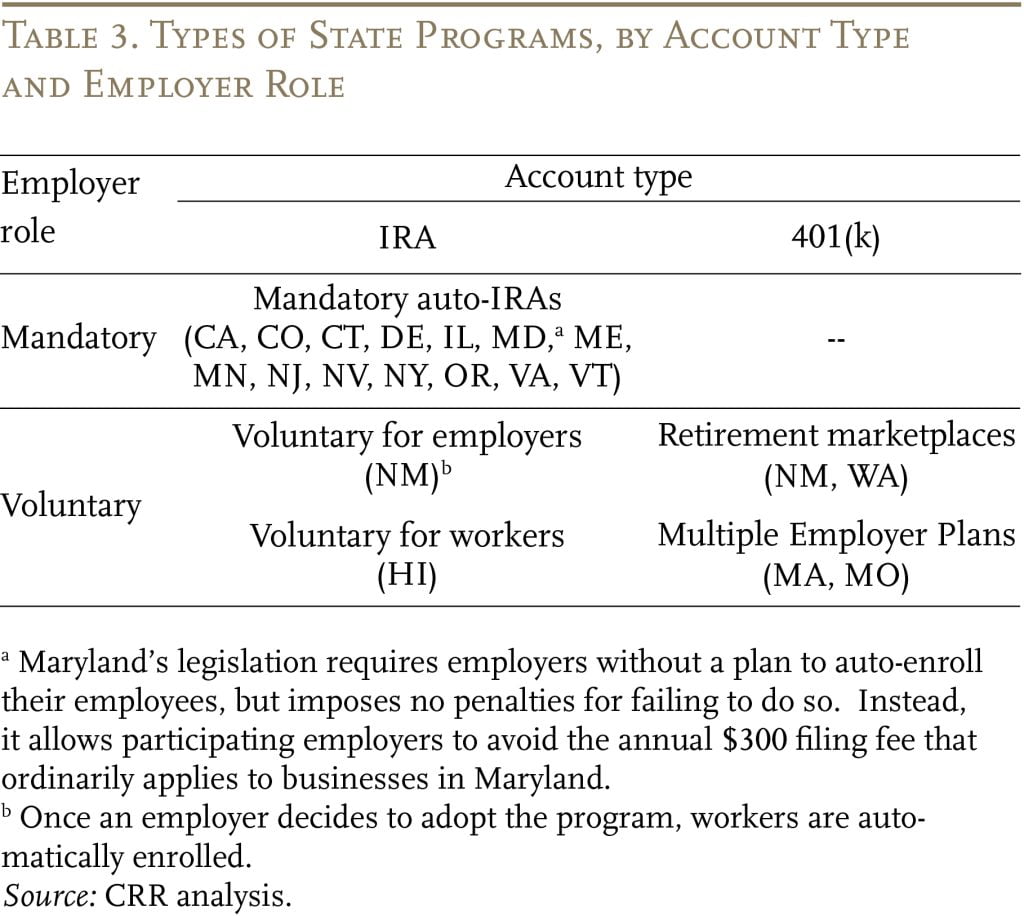

In the absence of meaningful federal action, states have seized the issue (see Figure 3). The inclusion of a mandate for employers is a significant differentiator for state programs. Mandatory auto-IRAs require employers without a retirement plan to auto-enroll their employees in an Individual Retirement Account (IRA). Voluntary programs, which involve “marketplaces,” multiple employer 401(k)s, and voluntary auto-IRAs, allow the employer to choose whether to participate (see Table 3).

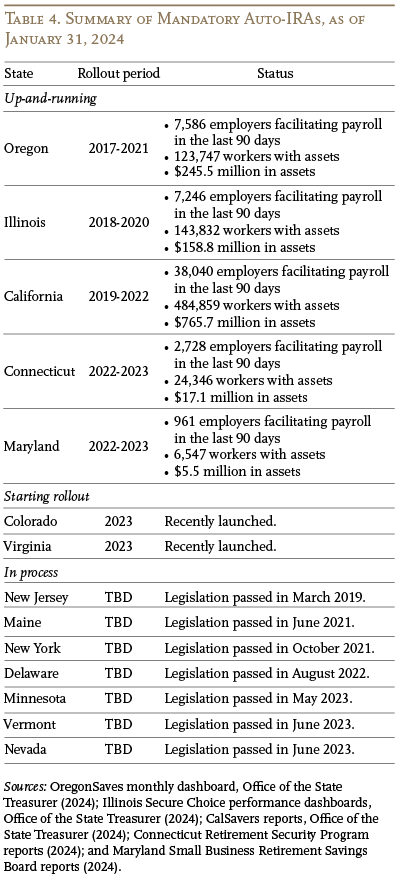

The mandatory programs are showing potential in the early phases (see Table 4). In contrast, voluntary programs have had virtually no impact, with less than a 1-percent take-up rate.

Other Resources

Georgetown University’s Center for Retirement Initiatives

Massena Associates

Pew Retirement Savings Policy Initiatives

Publications