Medicaid Coverage of Home Health Care is Growing: But Will the Trend Last?

Most seniors want to stay in their own homes when and if they need care. In response to this desire and the generally lower cost of home health and assisted living services compared to nursing home care, Medicaid has expanded its coverage of home-and-community-based services (HCBS) over time.

According to the Centers for Medicare & Medicaid Services, in 2023, 8.4 million Medicaid beneficiaries received assistance paying for care at home or in assisted living facilities – a substantial increase of 8 percent from 7.8 million in 2022. In comparison, 1.5 million beneficiaries received institutional care – mostly in nursing homes – a more modest 3-percent increase over 2022. However, the overall costs for institutional services grew by 17 percent compared to 13 percent for HCBS.

Growing HCBS Coverage

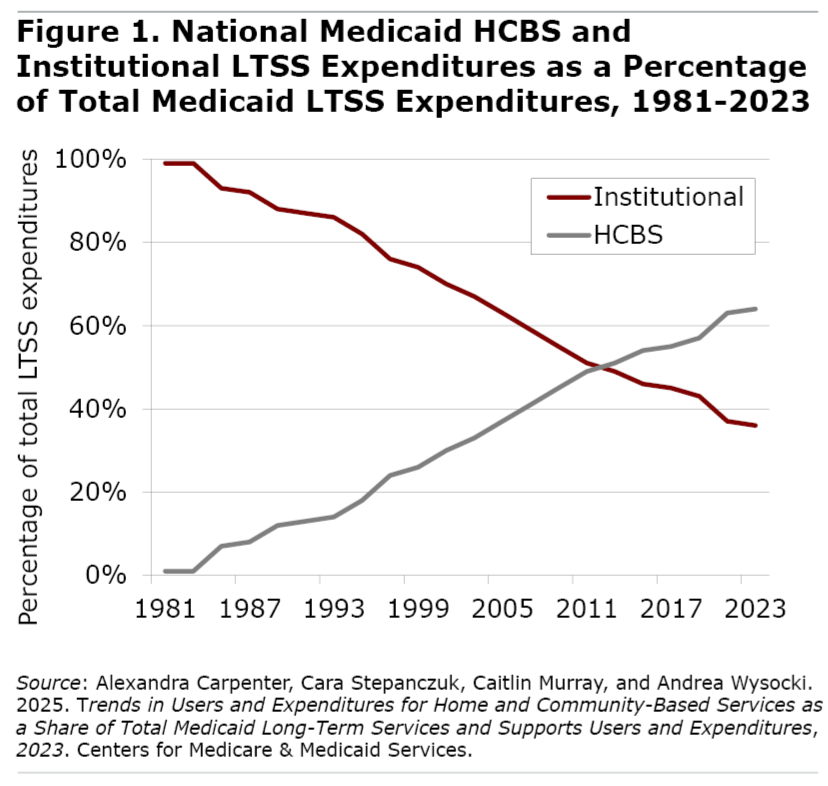

HCBS accounted for almost two-thirds of all spending on long-term services and supports (LTSS). For historical perspective, in 1981 only one dollar out of a hundred spent by Medicaid for LTSS went to HCBS, rising to half of LTSS spending by 2013 and continuing to grow thereafter (see Figure 1).

State Variation

Large variations exist in Medicaid coverage of HCBS by state in large part because such coverage is discretionary, in contrast to nursing home coverage, which is mandatory. Ninety-nine percent of Medicaid beneficiaries in Oregon and Wisconsin receiving LTSS were doing so at home or in assisted living facilities, in contrast with just 56 percent in Kentucky and 61 percent in Mississippi.

In terms of spending, Medicaid costs for HCBS constituted 95 percent of LTSS costs in Wisconsin as compared to just 36 percent in Arkansas. In other words, only 5 percent of Wisconsin’s expenditures on LTSS are going to nursing homes in contrast with 64 percent of Arkansas’ spending.

The Future?

Many people who work on long-term care policy are concerned that the $900 billion in Medicaid cuts in the “One Big Beautiful Bill” will reverse the trend towards more coverage of HCBS. While a lot of the bill’s cuts are aimed at younger beneficiaries, in large part by instituting work requirements, others, such as limitations on so-called provider taxes, are not. States will have to find ways to make up the shortfall in revenue or reduce services. One way may be to cut home health and assisted living coverage, since they are optional under the federal Medicaid rules.

For more from Harry Margolis, check out his Risking Old Age in America blog and podcast. He also answers consumer estate planning questions at AskHarry.info. To stay current on the Squared Away blog, join our free email list.

Keeping seniors at home is healthier and less expensive that warehousing them in nursing homes, but the U.S. must decide if it is going to allocate the money to do this. We need to pay home healthcare workers a living wage to encourage them to stick with this often-demanding work. We should also support family who provide this care, both financially and with emotional support and training.

The Partnership for long-term care state program provides two exemptions for Medicaid. First however much the long-term care insurance policy pays and benefits for your care you get to keep in cash and still qualify for Medicaid, you no longer have to spend down. Second Medicaid will no longer use a state recovery to force your estate to repay Medicaid, protecting the home. Most states have amended their Medicaid law to allow for the Partnership (see map https://is.gd/AndL0I ).