Retirees Are Worried About the Cost of Healthcare – and Who Can Blame Them?

Alicia H. Munnell is a columnist for MarketWatch and senior advisor of the Center for Retirement Research at Boston College.

The increase in Medicare Part B premiums has sparked concerns about out-of-pocket healthcare costs.

The 10-percent increase in Medicare Part B premiums for 2026 has reignited concerns about how much Social Security and total income people will have after they cover their out-of-pocket (OOP) health spending. Fortunately, my colleague Matt Rutledge has updated earlier research to answer precisely that question.

Even though retirees ages 65+ have Medicare, they still face considerable costs. In the case of Medicare Part A, which covers inpatient hospital care and is financed primarily by payroll taxes, beneficiaries face cost-sharing. Medicare Part B, which covers physician and outpatient hospital services, and Part D, which covers prescription drugs, are partly financed by premiums and include further cost-sharing. Because Medicare’s OOP costs are often substantial, many enrollees buy supplemental coverage, which may include additional premiums. Finally, many services, such as dental, vision, and hearing, are not covered by Medicare.

To identify total out-of-pocket healthcare costs, Matt used the 2018, 2020, and 2022 Health and Retirement Study (HRS). The sample included respondents who were ages 65+ and were receiving both Social Security and Medicare. In terms of expenditures, the HRS captures prescription drugs, special facilities, surgery, and medical visits to doctors, hospitals, and dentists. It also includes self-reported premiums paid for Medicare Part D, Medicare Advantage, and private supplemental plans. Medicare Part B income-related premiums were estimated based on the individual’s income.

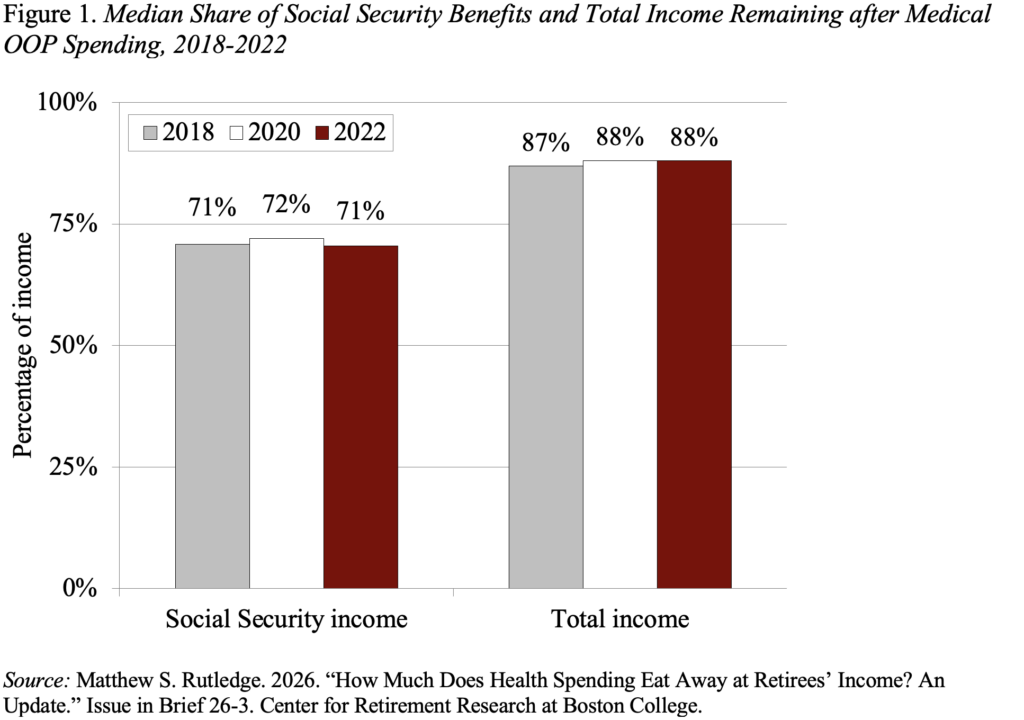

The central finding was the percentage of Social Security left after paying out-of-pocket health costs and how those results changed over the three surveys. As shown in Figure 1, the median percentage remaining in 2022 after medical OOP spending was 71 percent for Social Security benefits and 88 percent for total income. And these percentages were virtually unchanged over the three surveys.

In other words, OOP takes a big chuck of retirees’ resources, and the 10-percent increase in Medicare Part B premium suggests no relief on the horizon.

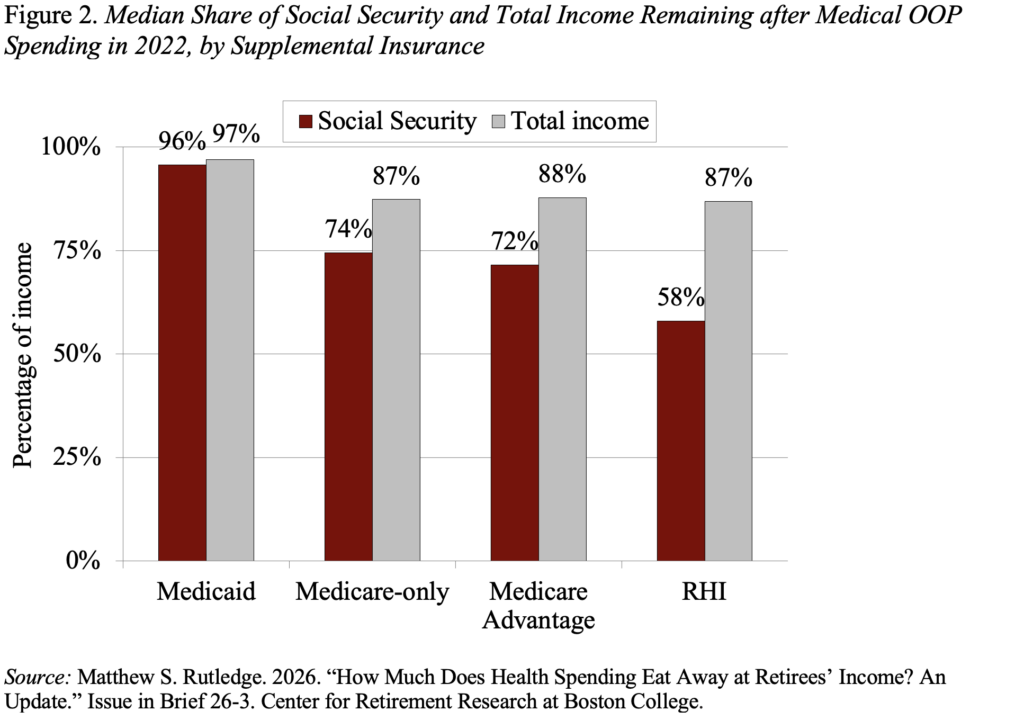

It’s also interesting to look at the relationship between supplemental coverage and the share of income remaining. As shown in Figure 2, enrollees in Medicaid had the highest share of resources remaining after OOP spending, because this program covers Medicare cost-sharing and premiums for low-income individuals.

Among the other three groups, OOP spending took its toll. It is helpful to look by source of income separately. With respect to Social Security, those with traditional Medicare and those with Medicare Advantage end up with 87-88 percent of their benefit, while those with employer-provided retiree health insurance (RHI) saw only 58 percent. Since all three groups have similar Social Security income and spend a similar amount on cost-sharing and uncovered services, the pattern simply reflects high RHI premiums. As a share of total income, all three groups have very similar post-OOP resources left available. This pattern reflects the fact that respondents with RHI have much higher total income than the other groups, with only about half of their income comes from Social Security.

The bottom line is that, while retirees have a variety of health insurance arrangements, OOP health spending took a substantial chunk out of Social Security benefits and total income – except for the poor covered by Medicaid. And, despite the pandemic and changes to policy and coverage markets, the situation showed no improvement across the 2018-2022 period. Moreover, the recent 10-percent increase in the premium for Medicare Part B suggests that out-of-pocket health costs could be more erosive going forward. Combine the possibility of further health policy costs and Social Security drawing ever closer to trust fund depletion, it is understandable why many retirees may feel that making ends meet is difficult.