Retirement Costs Vary Dramatically among States and Cities

Alicia H. Munnell is a columnist for MarketWatch and senior advisor of the Center for Retirement Research at Boston College.

Many are fine, but a handful face an almost insolvable problem.

The Center just released a brief that provides a comprehensive accounting of state and local government liabilities for pensions and other post-employment benefits (OPEB) and the fiscal burden that they pose on states, counties and cities. It also includes debt service costs to provide a full picture of government revenue commitments to long-term liabilities. To gauge the level of the burden, pension, OPEB, and debt service costs are compared to each jurisdiction’s own-source revenue. This work builds on the framework developed by Michael Cembalest at J.P. Morgan.

In accordance with new accounting guidelines, the analysis apportions the relevant liabilities of state-administered cost-sharing plans to local governments for a more accurate picture of where the burden lies. It also discounts promised pension benefits assuming a long-run rate of return of 6 percent, and applies a rigorous amortization plan (a closed 30-year amortization period with level dollar payments) that will really pay off the unfunded liability.

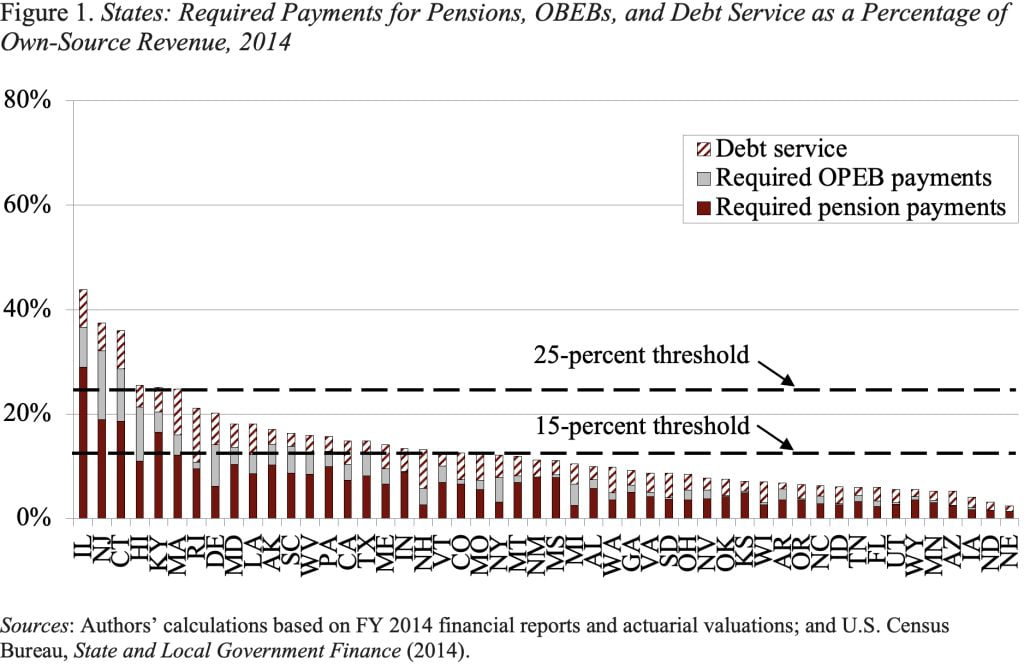

Figure 1 presents pension, OPEB, and debt service costs for states, ranked by the size of their total cost burden. About three quarters of the states have required payments below 15 percent of own-source revenue and 23 of those states face payments below 10 percent. On the other hand, five states – Illinois, New Jersey, Connecticut, Hawaii, and Kentucky – face payments in excess of 25 percent of revenue; and Massachusetts, Rhode Island, and Delaware face payments in excess of 20 percent.

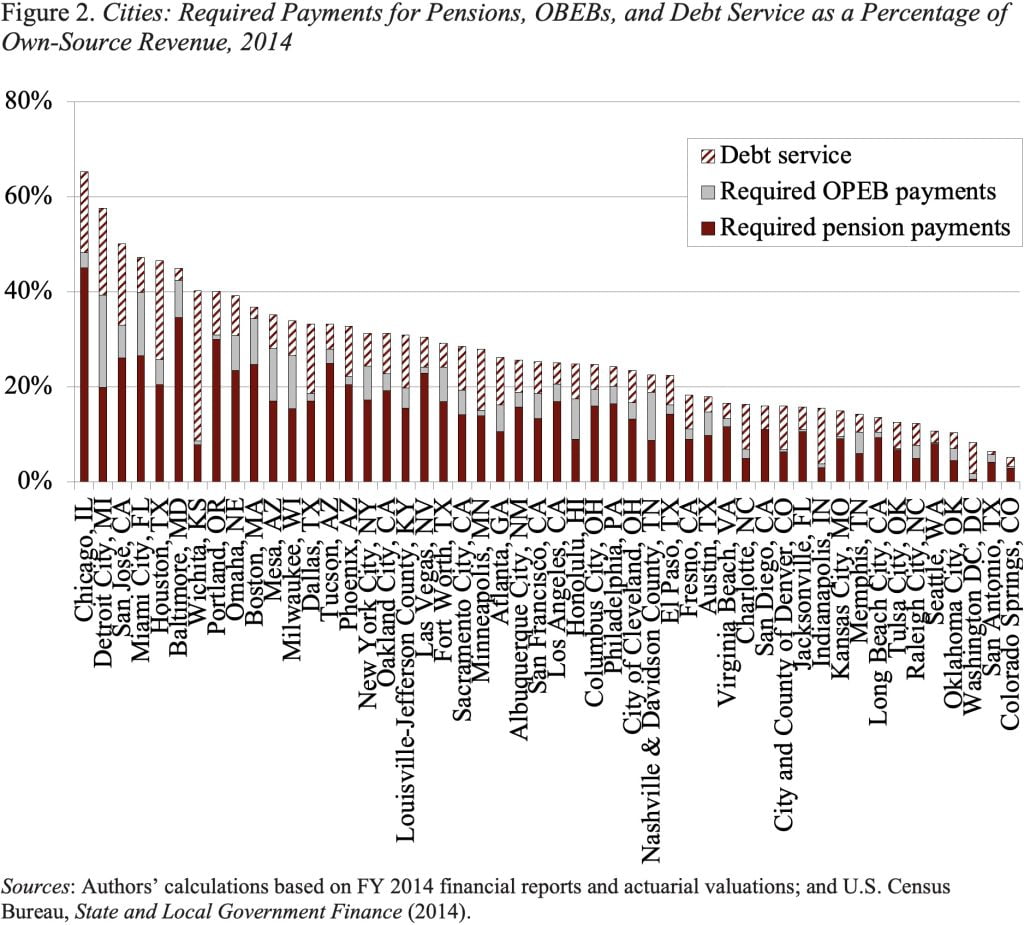

Figure 2 provides the results for the 50 largest of 173 sample cities. Costs are extremely high for Chicago, Detroit, San Jose, Miami, Houston, Baltimore, Wichita, and Portland – they all have costs in excess of 40 percent of own-source revenue. (Using own-source revenue as the denominator overstates the drain on the locality’s total resources, but provides a sense of the tax increase required if costs come in higher than expected.) On the other hand, many of the other large cities face a manageable burden.

The good news from this analysis is that the total costs for long-term commitments – pensions, OPEBs, and debt service – appear to be under control in many jurisdictions. However, a handful of states and cities face extraordinarily high costs. Given that these entities would need investment returns consistently in the 10-15 percent range for the next 30 years to solve their problems, they face only brutal options. They can raise taxes, but many of the states with the greatest burden already have relatively high taxes. They can cut other spending, but the magnitudes of the required cuts are very large – 10 to 20 percent. Or they can raise employee contributions even beyond what they are already contributing to their plans. Clearly, these governments face an enormous challenge.