The Federal Deficit Is a Mess – but Fixing Social Security Could Help a Lot

Alicia H. Munnell is a columnist for MarketWatch and senior advisor of the Center for Retirement Research at Boston College.

It’s good policy and would restore confidence in America’s most important program.

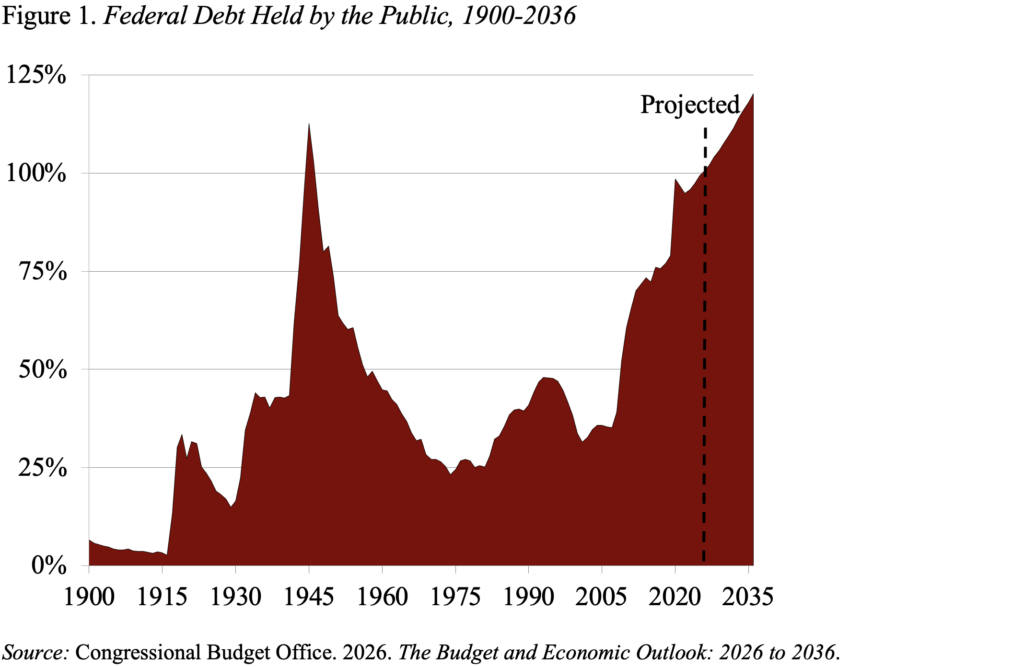

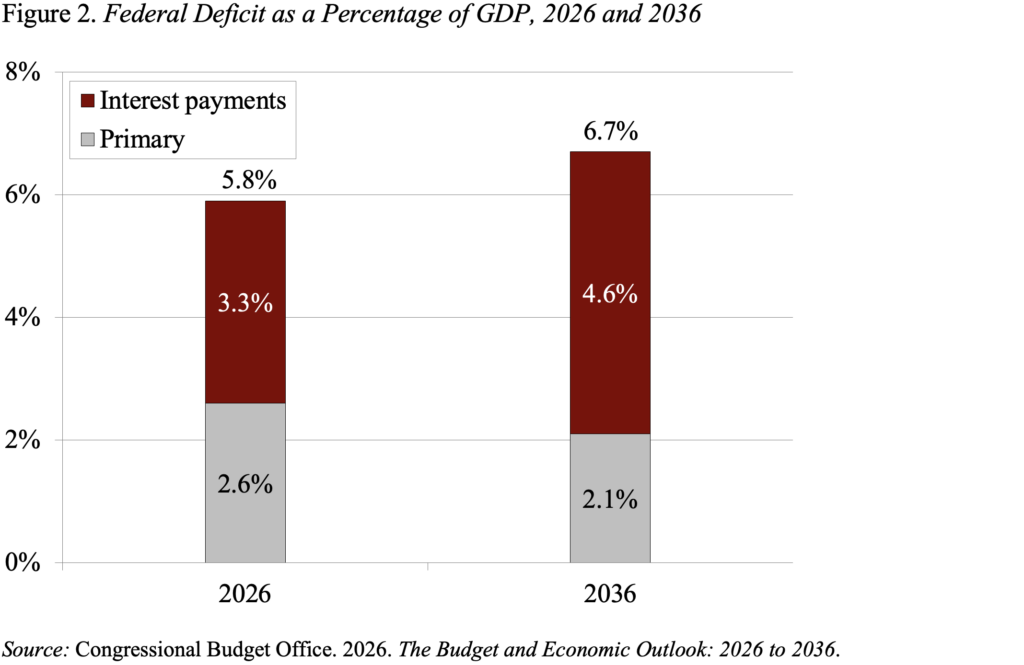

Recently, the Congressional Budget Office (CBO) released its budget projections. Unsurprisingly, the outlook is dismal. And it is somewhat more dismal than last year. The net result is that deficits as a percentage of GDP will rise from 5.8 percent in 2026 to 6.7 percent in 2036, and debt held by the public will rise from 101 percent in 2026 to 120 percent in 2036 (see Figure 1).

But in all this mess, I actually see something hopeful. And since my game is retirement, you should not be surprised that this ray of sunshine comes from Social Security. And it also comes from considering two different measures of the annual deficit: 1) the primary deficit – the shortfall between federal revenues and outlays on government programs – and 2) the total deficit, which includes interest payments on outstanding federal government debt (see Figure 2). The primary deficit could be considered a measure of how much our current behavior is out of whack, and the rest of the deficit reflects increased spending and tax cuts since 2001.

The encouraging part of this story is that the 2.6-percent primary deficit, declining to 2.1 percent in 2036, doesn’t seem that daunting to me. The basis for that optimism is that the CBO projections are based on the assumption that Social Security trust funds will be fully funded and thus able to pay full benefits scheduled under current law. That is, under existing legislation the CBO estimates do not recognize that Social Security would have to cut benefits once the trust fund is exhausted in the early 2030s. If CBO were permitted to recognize that current revenues will require benefit cuts, the projected primary deficit would be a lot lower.

The Social Security actuaries project that the costs of Social Security over the next 75 years average 6.1 percent of GDP and revenues 4.8 percent, leaving a deficit of 1.3 percent of GDP. Eliminating Social Security’s deficit would cut the federal government’s primary deficit in half.

It would also make Americans happy. Workers and retirees, the poor and the more affluent, and Republicans and Democrats enthusiastically support the Social Security program. Fixing Social Security sooner rather than later would keep more options open, distribute the burden more equitably across generations, and most importantly, restore confidence in the nation’s major retirement program.

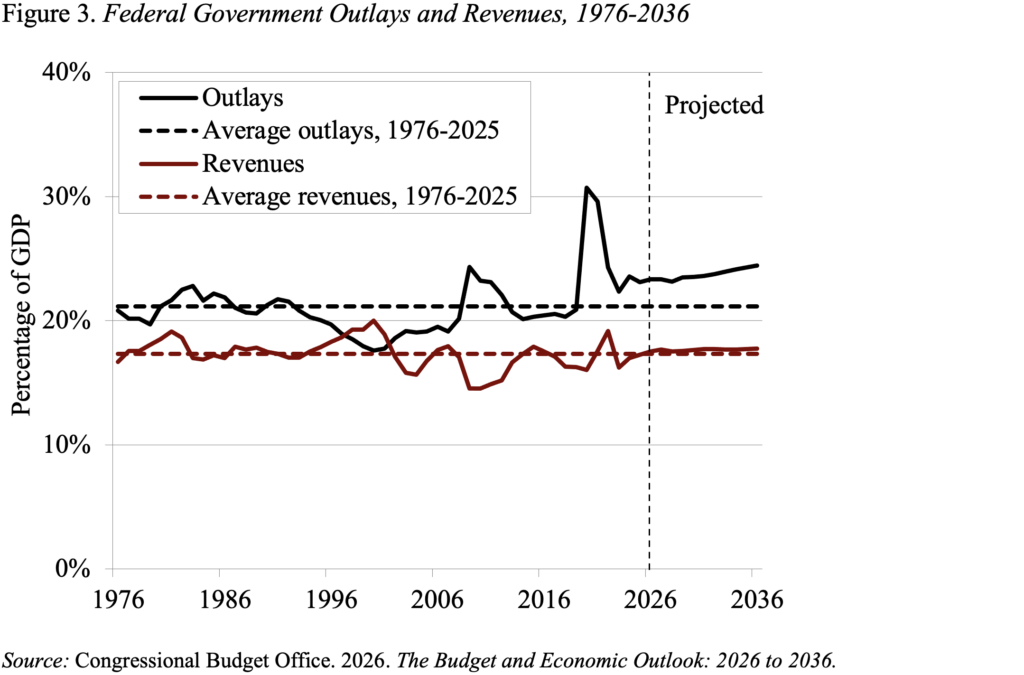

Of course, fixing Social Security solves only part of the primary deficit problem. The other half requires reining in our health costs that make Medicaid and Medicare so expensive. But we also need higher revenues as a percentage of GDP. Revenues as a percentage of GDP have remained absolutely flat despite the aging of the population (see Figure 3). That pattern makes no sense when more people need retirement income and health care – even if the healthcare costs were reasonable. Planning for a gradual increase in tax revenues would also make sense for the future.

In general, we need to fully eliminate CBO’s projected primary deficit. Of course, the government needs to support the economy during periods like the Great Recession and COVID, but then it needs to run some surpluses when times are good. With the CBO projecting unemployment rates under 5 percent, the primary deficit should be close to zero. Indeed, in the last 50 years, the primary deficit has averaged 0.5 percent of GDP when the unemployment rate was low. The first, most realistic step towards tackling the federal deficit is restoring financial balance to Social Security.