Why Social Security Faces a Financial Reckoning Just a Few Years From Now

Alicia H. Munnell is a columnist for MarketWatch and senior advisor of the Center for Retirement Research at Boston College.

Did policymakers in 1983 do a good job fixing Social Security?

The impending exhaustion of Social Security’s retirement trust fund in 2033 has stimulated a lot of commentary. One strain focuses on actions taken in 1983 – the last time Congress addressed the program’s finances. In terms of outcomes, some commentators conclude that Congress did a good job in 1983, and others ask, “Why did Congress deliberately schedule Social Security insolvency?”

Let’s start by looking at the financial contours of Social Security’s finances. When Social Security was enacted in 1935, the legislation envisioned the buildup of a trust fund and a close alignment of contributions and benefits for any given cohort. The 1939 amendments, however, broke the link between lifetime contributions and benefits by tying benefits to average earnings, initially over a minimum period of coverage, and adding spousal and survivor benefits that were effectively unfunded. As a result, Social Security moved from a funded program to a pay-as-you-go system where current workers pay the benefits for current retirees. The costs of those benefits as a percentage of taxable payrolls depend crucially on the ratio of retirees to workers.

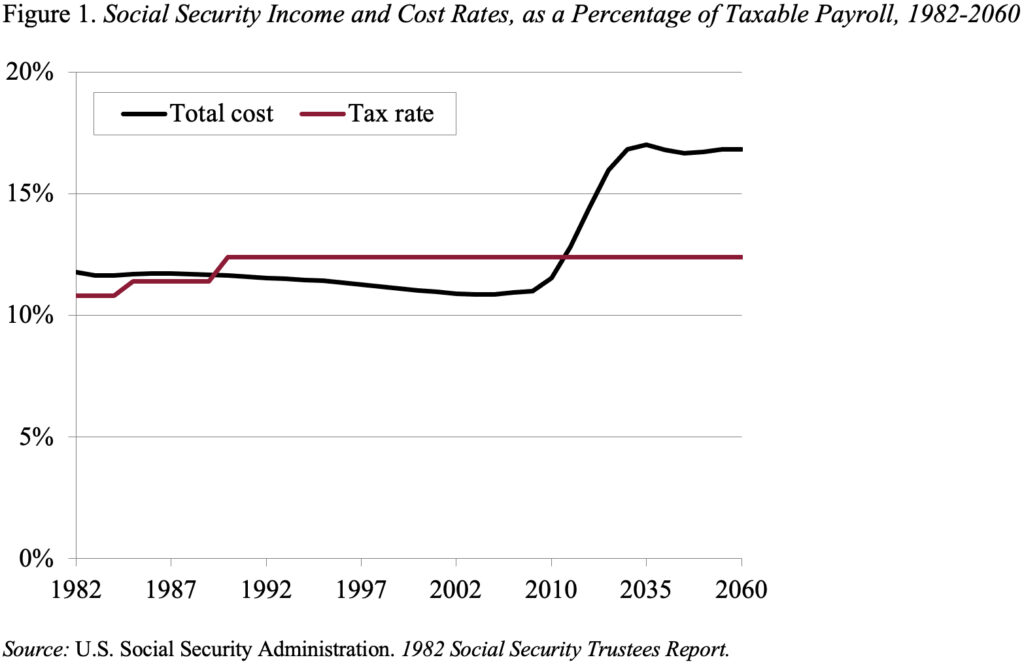

In 1982, policymakers were looking at a situation – not unlike today’s – where the cost of benefits exceeded the tax rate and, with the cost of benefits scheduled to rise, the gap between the cost and tax rate was projected to grow over time (see Figure 1). (The data in Figure 1 and in the following discussion include both the retirement and disability components of Social Security.) The increase in the cost of benefits reflected the combined effects of the retirement of Baby Boomers and a slow-growing labor force due to the decline in fertility.

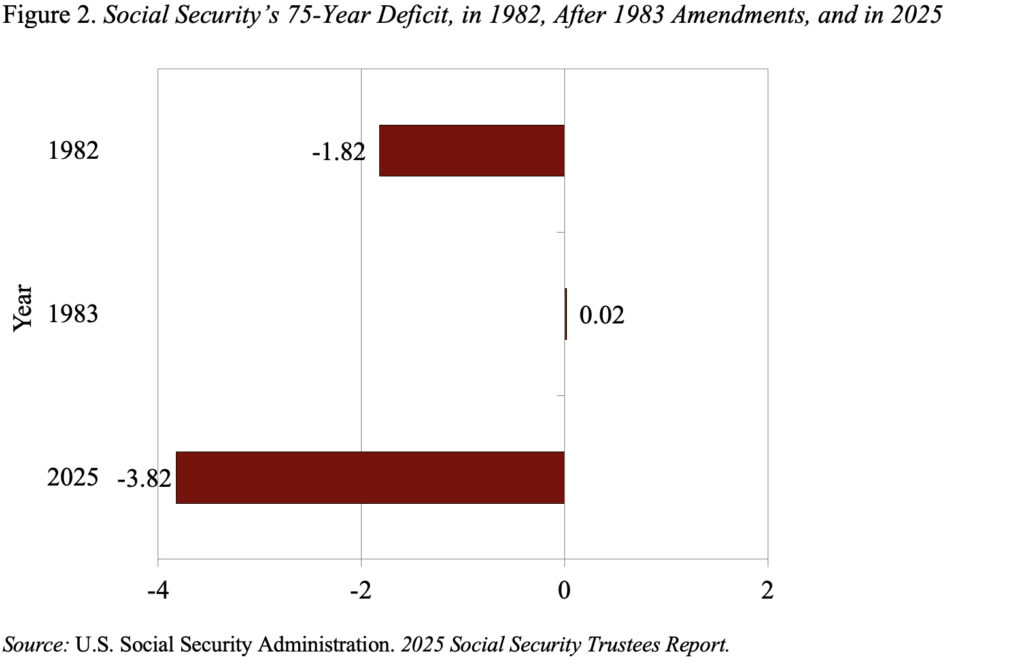

Social Security finances are assessed on a 75-year basis, so policymakers’ goal in 1982 was to eliminate the 75-year deficit. In 1982, the 75-year deficit was equal to 1.82 percent of taxable payrolls, roughly half the 75-year deficit reported in the 2025 Trustees Report (see Figure 2).

The 1983 Amendments addressed both the short-term financing crisis and some of the long-term challenges. Immediate changes included a six-month delay in the cost-of-living adjustment; acceleration of an already-enacted increase in the payroll tax rate; an extension of coverage to new federal employees and employees in non-profit organizations; and the taxation of benefits for high-income beneficiaries. These changes ensured that payments could be made without interruption. To address the longer-term issue of rising costs, Congress raised the age at which beneficiaries could receive full benefits from 65 to 67, beginning in 2000 and then phased in slowly through 2022.

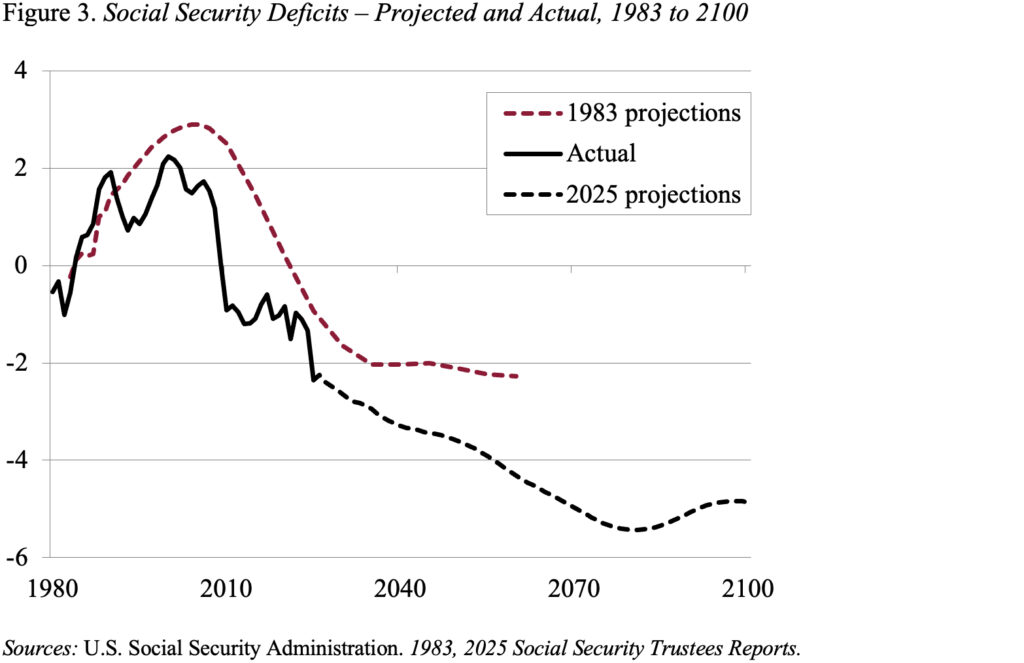

The Social Security Trustees projected that this package of adjustments would keep the system solvent for the next 75 years. As it turned out, early surpluses were smaller and subsequent deficits larger than anticipated (see Figure 3), and the trust fund is now scheduled for exhaustion in 2033.

But even if the projections had been accurate, the actuaries and the policymakers in the early 1980s knew that more tax increases or benefit cuts would be needed down the road. The surpluses during the early years before the Baby Boom retired would cover the later deficits, but eventually the trust fund would be exhausted, and further changes would be needed to cover the annual shortfalls.

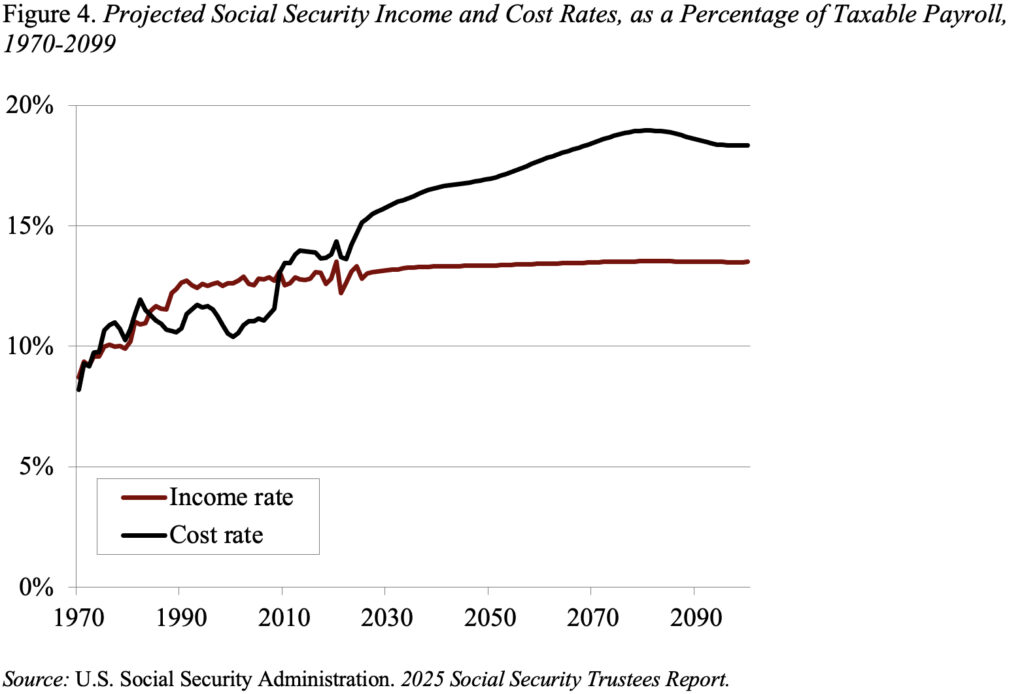

Because the trust fund will be depleted earlier than expected, policymakers need to quickly turn their attention to fixing Social Security. But they, like their 1983 counterparts, will not be able to solve the whole problem. Further adjustments will be needed in the future. That will not always be true; the projections show costs stabilizing around 2080, and thereafter a fix for 75 years could ensure a fix forever (see Figure 4).

The bottom line is that the people who brokered the 1983 amendments did a pretty good job. They did more than put out the fire; they also made a down payment on solving the longer-term costs of an aging society. To solve the program’s finances forever would have involved a massive hike in the tax rate on those early workers so that subsequent cohorts could have a fully financed program. Balancing the burden between current and future cohorts is a tricky question, both theoretically and practically. Policymakers in the early 1980s were searching for an equitable balance; they were not out to “deliberately schedule Social Security insolvency.”

That said, when the horse-trading begins after the 2026 elections on a package to restore financial balance to Social Security, one item that should be on the table is some form of automatic adjustment mechanism, since U.S. policymakers are terrible at addressing problems before we are about to fall off a cliff.