Windfall Elimination Provision (WEP) Now a Hot Topic!

Alicia H. Munnell is a columnist for MarketWatch and senior advisor of the Center for Retirement Research at Boston College.

The real answer is that all state and local workers should be covered by Social Security.

One would think that, focusing on retirement issues all day long, I would know that the Windfall Elimination Provision (WEP) had become a hot topic. No such luck; it took me totally by surprise. Now you are shaking your head, and saying: “What the hell is the WEP?”

It is actually a well-intentioned attempt to solve an equity issue that arises out of the fact that about 25-30 percent of state and local workers are not covered by Social Security. This exclusion creates two types of problems. First, employees lacking coverage are exposed to a variety of gaps in basic protection – most notably in the areas of survivor and disability insurance. Second, uncovered state and local workers can gain minimum coverage under Social Security and – until the introduction of the WEP in 1983 – could profit from the progressive benefit structure, which was designed to help low-wage workers rather than workers whose second career entitled them to benefts.

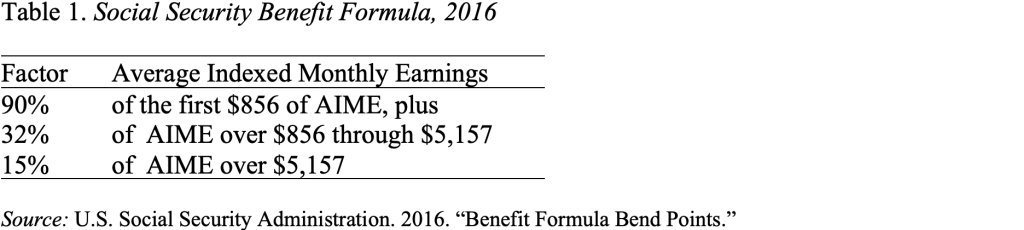

The Social Security benefit formula applies three factors to the individual’s average indexed monthly earnings (AIME). Thus, a person’s benefit would be the sum of 90% of the first $856 of AIME, 32% of AIME between $856 and $5,157, and 15 percent of AIME over $5,157 (see Table 1).

Since a worker’s monthly earnings are averaged over a typical working lifetime (35 years), a high-wage earner with a short period of time in covered employment looks exactly like a low-wage earner. Both would have 90 percent of their earnings replaced by Social Security.

Similarly, a spouse who had a full career in uncovered employment – and worked in covered employment for only a short time or not at all – would be eligible for the spouse’s and survivor’s benefits.

The WEP instituted a modified benefit formula for public employees who qualify for a Social Security benefit based on a brief work history and who have earned a pension in noncovered employment. The Government Pension Offset (GPO) reduces spouses’ benefits for those who have a government pension in uncovered employment.

The WEP reduces the first factor in the benefit formula from 90% to 40%; the 32% and 15% factors remain unchanged. The WEP therefore causes a proportionally larger benefit cut for workers with low AIMEs, regardless of whether they were a high- or low-earner in their uncovered employment. On the other hand, the WEP does guarantee that the reduction in benefits cannot exceed half of the worker’s pubic pension, which protects those with low pensions from uncovered work. The WEP does not apply to workers with more than 30 years of substantial employment under Social Security and the reduction in the 90% factor is phased out for workers with 21 through 29 years. It may not be perfect, but doesn’t sound crazy.

Over the last two decades, numerous bills have been introduced to repeal the WEP, but they have made little progress. That’s good, because some type of WEP adjustment is needed, not simply a repeal.

Recently, Kevin Brady (R-TX) introduced a bill with a new WEP formula. First, the regular Social Security factors would be applied to all earnings – both covered and uncovered – to calculate a benefit. The resulting benefit then would be multiplied by the share of the AIME that came from covered earnings. Such a change would likely produce smaller reductions for the lower paid and larger reductions for the higher paid. That sounds reasonable.

The question is whether it is worth the trouble of creating a whole new procedure when the real answer is to extend Social Security coverage to all state and local workers. Universal coverage would both offer better protection for workers and eliminate the equity problem.