Social Security Is Already the Best Anti-Poverty Program We Have – Don’t Make This Radical Change

Alicia H. Munnell is a columnist for MarketWatch and senior advisor of the Center for Retirement Research at Boston College.

Changing Social Security to a flat benefit for all would put both workers and the poor at risk.

Social Security is this country’s most important and most popular program. However, changes will be needed soon, as the program will not be able to pay full benefits once the retirement trust fund is depleted in 2033. While many options have been suggested to solve the financing problem within Social Security’s current structure, a major report and two books (Biggs and Boccia & Nachkebia) have suggested radically changing the program. While the details differ, all three proposals would move Social Security from a wage replacement program to one that provides a flat benefit to all, aimed at reducing poverty.

A major redesign of Social Security is not only unnecessary but also risky for the poor. While the flat payment might start with no means-testing, pressure would rise over time to limit the outlays from general revenues. And the evidence in the U.S. is that means-tested efforts financed through general revenues are very vulnerable. The most recent and jarring evidence is the recent cuts to Medicaid and SNAP (formerly food stamps) in the One Big Beautiful Bill last year. But equally disheartening is the gradual erosion of the nation’s Supplemental Security Income (SSI) program, designed to alleviate poverty among those 65+ and with disabilities.

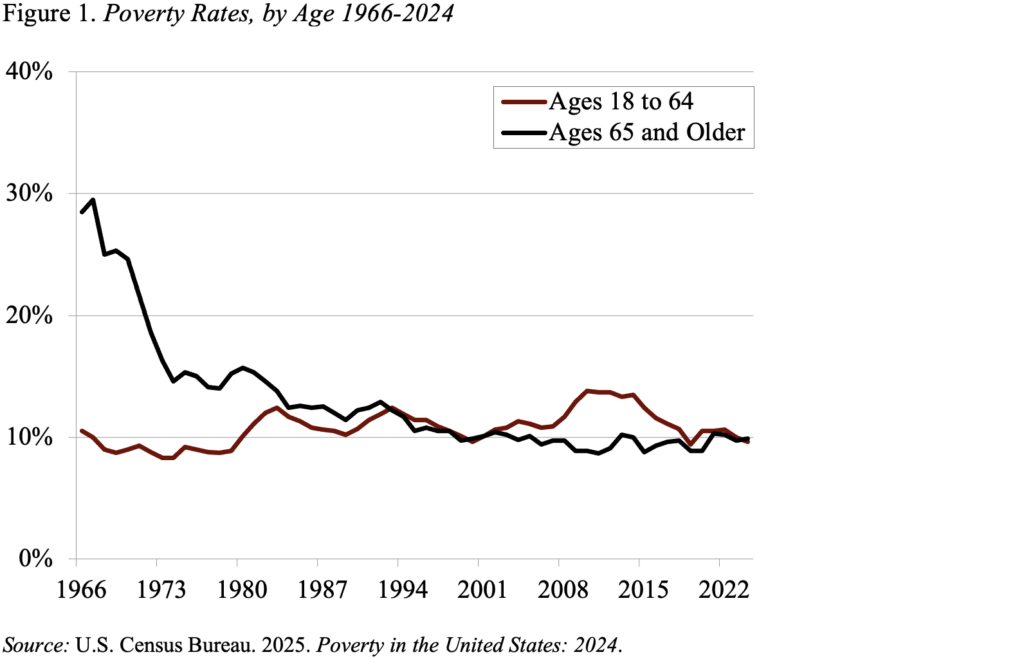

While poverty rates can be measured in several ways, they all basically tell the same story – poverty among those 65+ is about 10 percent. Most importantly, while poverty among older Americans in the 1960s was dramatically higher than that for other adults, today it is about the same (see Figure 1). This improvement is due to the growth of the Social Security program, which allows retirees’ incomes to keep pace with rising living standards by wage-indexing initial benefits and then price-indexing benefits in retirement.

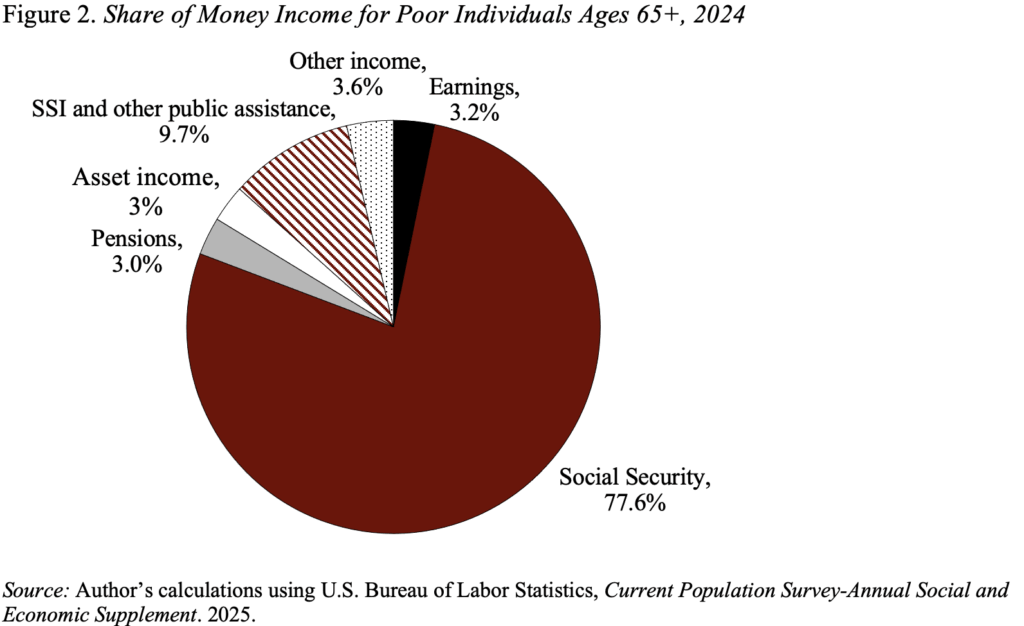

Indeed, Social Security is the major source of income for those 65+ with incomes below the poverty threshold (see Figure 2). Only 10 percent comes from SSI and other forms of means-tested programs.

That pattern of little support from means-tested sources reflects the fact that, in the U.S., programs designed solely for poor people are poor programs – their benefits erode over time; unchanging income and asset tests reduce the eligible population; and they are expensive to administer. In contrast, programs like Social Security – in which everyone participates and receives benefits – are the most reliable way to ensure income for those with low earnings.

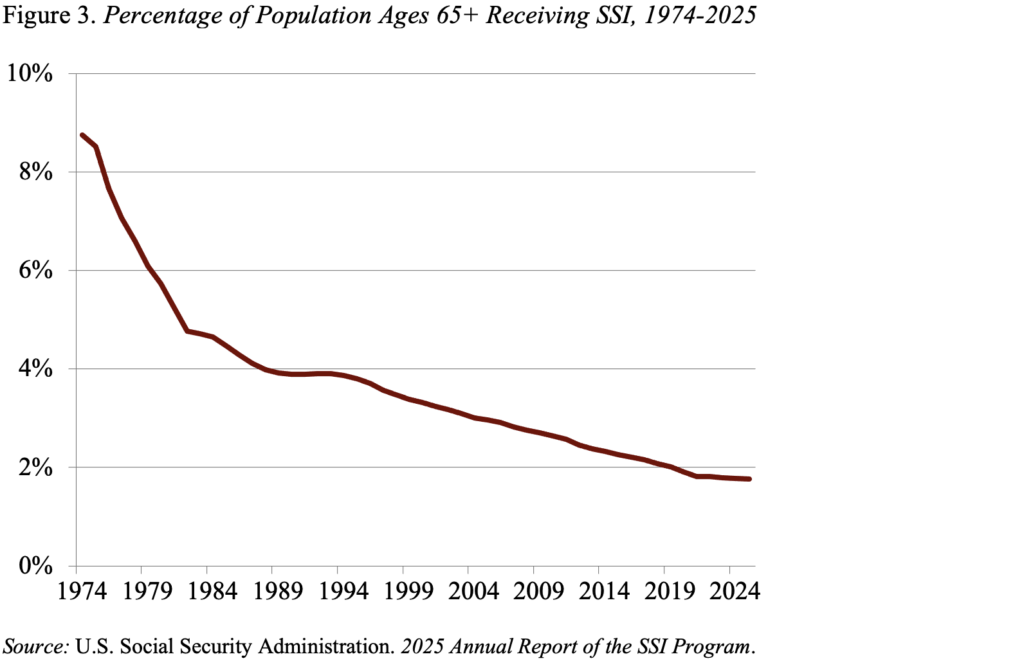

That said, Social Security alone is not enough for those with weak ties to the labor force. To meet that need, Congress enacted the SSI program in 1972 to nationalize the state welfare programs for adults 65+ and those with disabilities. But the program, which began paying benefits in 1974, has not been kept up to date, and the percentage of the 65+ population receiving SSI benefits has dropped from 9 percent to 2 percent (see Figure 3).

We do need to eliminate poverty for older Americans, but the answer lies in strengthening SSI, which has been allowed to wither on the vine. SSI provides very modest benefits because its asset limits and income disregards have not been updated in decades. More specifically, the assets limit, whereby beneficiaries can keep only $2,000 in savings, has been frozen since 1989. And, beneficiaries who work can keep only $65 of their earnings each month, after which benefits are reduced by $1 for every $2 earned, and Social Security beneficiaries can keep only $20 of their monthly check without a reduction in their SSI benefits.

Let’s update SSI and maintain Social Security’s current structure to best protect poor older Americans.