How Policy Risks Affect Retirement Planning for Older Americans

The brief’s key findings are:

- Planning for retirement is complicated by uncertainty over Social Security, Medicare, taxes, federal debt, and inflation.

- These policy risks have been rising since the start of 2025, as captured by a new survey of investors nearing, or in, retirement.

- The survey finds people are more concerned about their future; and they cite the prospects of Social Security cuts and high inflation as most harmful.

- In response to policy risks, some plan to delay retirement and shift to more conservative investments.

- Since hedging risks comes at a cost, the greater uncertainty of today’s policy environment clearly hurts older Americans.

Introduction

Planning for a secure retirement is an enormous challenge – the plan must cover all of a person’s remaining years and beyond, considering their legacy. Further complicating such planning are possible shifts in the public policy environment: changes to social insurance programs can undermine the foundations of a retirement plan; changes to the tax system can scramble a household’s finances; and a ballooning government debt can increase interest rates and slow the economy. The question is how the recent uptick in policy risk may affect the decisions and behavior of near-retirees and retirees.

This brief, which is the first of two drawn from a recent study, addresses that question by combining a comprehensive summary of the academic literature with a new survey of the changes in the views and actions of near-retiree and retiree investors since the start of 2025.1 The survey looks simultaneously across three policy areas: 1) Social Security; 2) Medicare; and 3) fiscal policy – primarily, the federal debt and taxes. The second brief will report on the results of a companion survey – one focused on financial advisors – to understand the advice these older investors might have received regarding the uptick in policy risk.

The discussion proceeds as follows. The first section reviews the literature on the measurement of policy uncertainty and its estimated impacts. The second section explores uncertainty in various policy areas, discussing the stakes in the current environment and how unsettled policy might affect households planning for retirement. The third section describes the 2025 Retirement Investor Survey and presents the results. The final section concludes that older Americans are keenly aware of the increase in policy uncertainty on many fronts and are taking defensive responses. These responses clearly harm older Americans because hedging risks comes at a cost.

What Is Policy Uncertainty and How Could It Affect Household Behavior?

The first step in this analysis is defining “policy uncertainty.” The issue is not about policy change, per se, but rather about the unpredictability of future policy. Even without any change to current policy, for example, a tight and polarized election forces households to consider a wider range of policies than if the election outcome were certain or the policy positions of the candidates were similar.

The most common approach to measuring such uncertainty is textual analysis of media coverage for terms associated with policy risk.2 An influential paper, for example, measured the frequency of articles in 10 leading newspapers that contained the three terms: “economic” or “economy”; “uncertain” or “uncertainty”; and one or more of “Congress,” “deficit,” “Federal Reserve,” “legislation,” “regulation,” or “White House.”3 The resulting index mirrored news events that one might expect to increase uncertainty, such as the 9/11 attacks or tight presidential elections.

Other approaches to understanding policy risk involve looking at actual variability in policy parameters and the impact of these changes on behavior. For example, one study found that increasing volatility in U.S. taxes reduced economic activity.4 An alternative approach is to rely on case studies. For example, on the eve of a tight German election, households increased savings by reducing consumption and working more.5 Another approach uses surveys to ascertain household perceptions of policy uncertainty and their likely responses.6

Such general policy uncertainty (not tied to specific programs) seems to have increased over the past few decades in the United States.7 This increase reflects both a larger role of government in the economy (increased taxes/subsidies, spending, and regulation) and greater political polarization, which leads to greater swings in policy when power changes hands.

The effects of policy uncertainty on the economy are broadly negative.8 In terms of the macroeconomy, uncertainty depresses economic activity, increases stock-market volatility, and reduces returns.9 Similarly, unemployment is found to rise in the face of greater uncertainty, while consumption and investment tend to fall.10

All this evidence relates to policy uncertainty in general. However, policy risk varies across programs.

How Does Policy Risk Vary Across Programs?

The three most important areas of policy risk for near-retiree and retiree investors are Social Security, Medicare, and fiscal policy.

Social Security

Since Social Security provides the majority of income for roughly half of U.S. retirees, any change to the program can have seismic implications for their household finances. And large changes are on the horizon, since Social Security’s retirement trust fund is projected to run out of money in 2033, after which current revenue is likely to cover about 75 percent of statutory retirement benefits.11

Concern about Social Security’s fiscal imbalance can lead households to take precautionary actions in terms of savings, work, and claiming ages, and the precise responses likely vary by type of household. For example, younger households are more sensitive than their older counterparts to changes in payroll taxes, and less sensitive to changes in benefits because they have more time to reoptimize.12 Similarly, lower-income households would be more sensitive to any changes than higher-income ones, as Social Security is a larger part of their lifetime resources.13

Precisely how households would actually respond, however, is unclear. For example, when presented with a specific policy response of a 30-percent benefit cut, many individuals say that they intend to reduce spending.14 On the other hand, when the policy response to Social Security’s shortfall is left unspecified, households have no clear idea how they would adapt. For example, one study found no intended change to savings in response to more alarming descriptions of Social Security’s fiscal problem.15

With respect to labor activity and claiming, the evidence is also ambiguous. One study found that households plan to work longer in response to a 30-percent Social Security benefit cut, thereby reducing the cut to their monthly benefit from 30 percent to 21 percent.16 On the other hand, another study found that some households plan to claim earlier than otherwise when press stories draw their attention to the “unsustainability” of current Social Security benefits.17 What is clear is that households’ attempts to protect themselves against Social Security policy risk is harming them. Studies find that knowing what reform will be adopted in advance is valuable, with individuals willing to forgo as much as 6 percent of expected benefits or 2.5 months of earnings to resolve the uncertainty.18

Medicare

If Social Security is the foundation of retirees’ resources, healthcare remains one of their biggest consumption items and two programs dominate government policy in healthcare: Medicare and Medicaid. While both programs are subject to considerable policy risk, this discussion is limited to Medicare, because older individuals account for only 10 percent of the Medicaid population.19

Unlike Social Security, the finances of Medicare are not structurally unsound.20 However, Medicare operates in a high-cost healthcare environment, so its outlays have historically risen far faster than GDP and have accounted for a growing share of the federal budget. Given the cost pressure, Medicare may become less generous in the future with either higher premiums or greater cost-sharing (co-pays, co-insurance, and deductibles).

Medicare cuts could have both financial and healthcare implications. For example, when Medicare reduced reimbursement rates, some studies found that the quantity of healthcare services provided declined, as hospitals reduced the number of beds.21 Some researchers even found that reduced reimbursement rates led to slower improvement in mortality.22 On the other hand, another study found changes in reimbursement rates only affected utilization of one procedure out of eight examined. One area where care may not be affected is Medicare Advantage, where cuts may reduce rents extracted by private insurers.23

Households may react to Medicare policy risk in many of the same ways as to Social Security reform options. Increasing either premiums or cost-sharing would reduce retirees’ resources available for other purposes. Thus, the prospect of such reforms may lead households to save more or work longer. Furthermore, such impacts are likely to affect lower-wealth households more, since healthcare costs account for a disproportionate share of their consumption.24

Fiscal Policy

The U.S. government borrows money when taxes fall short of outlays, and this borrowing adds to the already large national debt. Excessive debt can eventually lead to rapidly rising interest rates on Treasury securities, which cascade through to other forms of borrowing, or to a major increase in taxes or decline in public spending.

For retirees, the rising interest rates caused by increasing government debt are mitigated as they are less likely to borrow than younger households. They are nevertheless likely to be impacted in two ways. On the one hand, retirees will see the price of their existing bond holdings go down as interest rates rise. On the other hand, they will be able to buy bonds or annuities with better yields. Overall, younger retirees will be less likely to be negatively affected as they hold fewer fixed-income securities than older retirees.

In addition, if the government raises taxes or cuts spending to deal with the debt, it could directly affect people’s finances by decreasing their disposable income. For example, reducing the deduction for mortgage interest on housing or increasing income tax rates would reduce retirees’ after-tax income. Alternatively, if the federal government cuts spending by reducing transfers to other levels of government, states and localities may cut services or raise their income, sales, and/or property tax rates.

This discussion on the policy risk associated with Social Security, Medicare, and federal debt/taxes provides a basis for addressing the question: “How have recent changes in policy uncertainty affected today’s near-retirees and retirees?”

Results from the Retirement Investor Survey

The survey of near-retirees and retirees was conducted by Greenwald Research between July 7 and July 31, 2025. The sample consisted of 1,443 individuals ages 45-79 with over $100,000 in investable assets. The survey explored both how the participants perceived the nature and severity of the risk regarding Social Security, Medicare, and fiscal policy, and how they might act to hedge the risk.

Overall View of Policy Risk

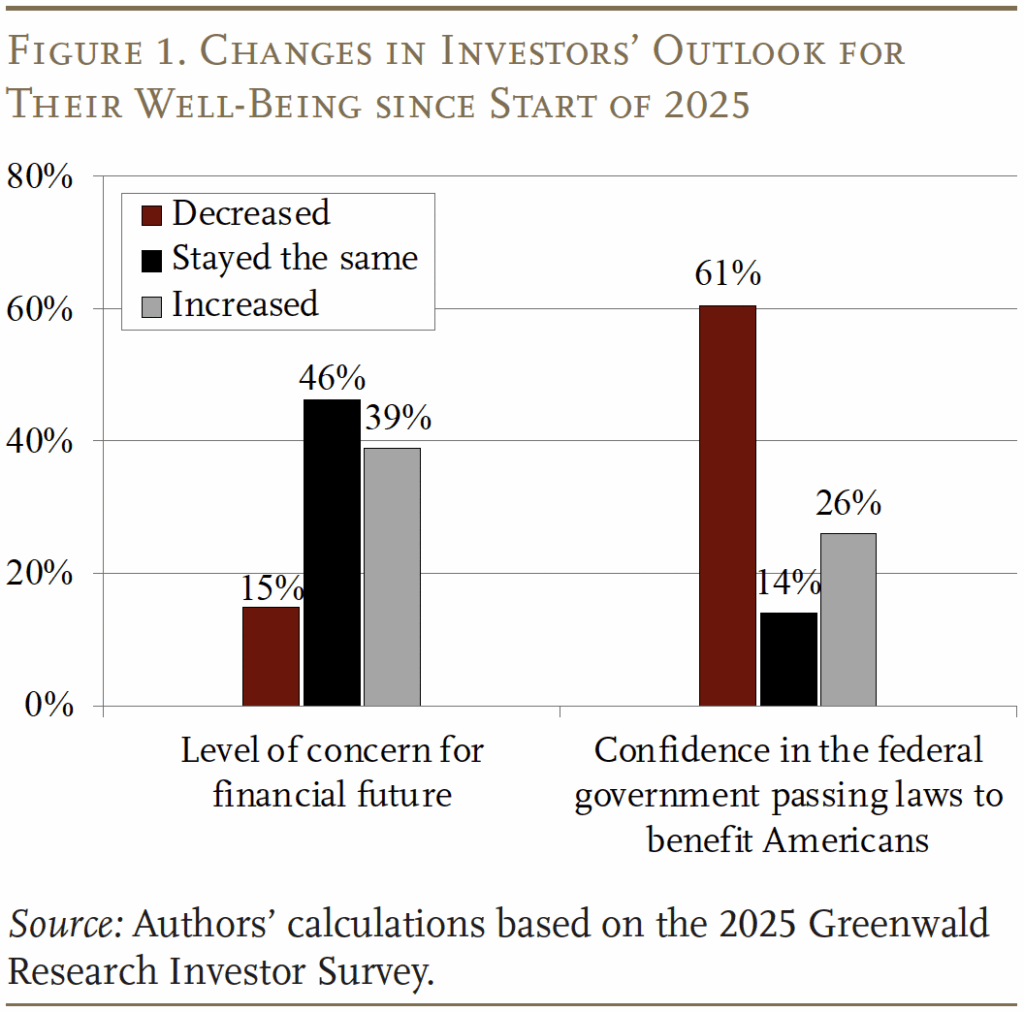

Since the beginning of 2025, policy has changed in drastic ways in terms of taxation (including tariffs), the federal debt, and Medicaid (due to the One Big Beautiful Bill Act). And long-term trends in Medicare and Social Security financing have become more concerning. It should therefore come as no surprise that respondents to the investor survey in July 2025 – referred to in figures and tables as “investors” – expressed concern about the direction and unpredictability of federal policy. Figure 1 shows that investors’ concerns for their financial future mounted (39 percent say concern increased versus 15 percent who say it decreased), while their confidence that federal policy will benefit Americans declined (61 percent decreased versus 26 percent increased).

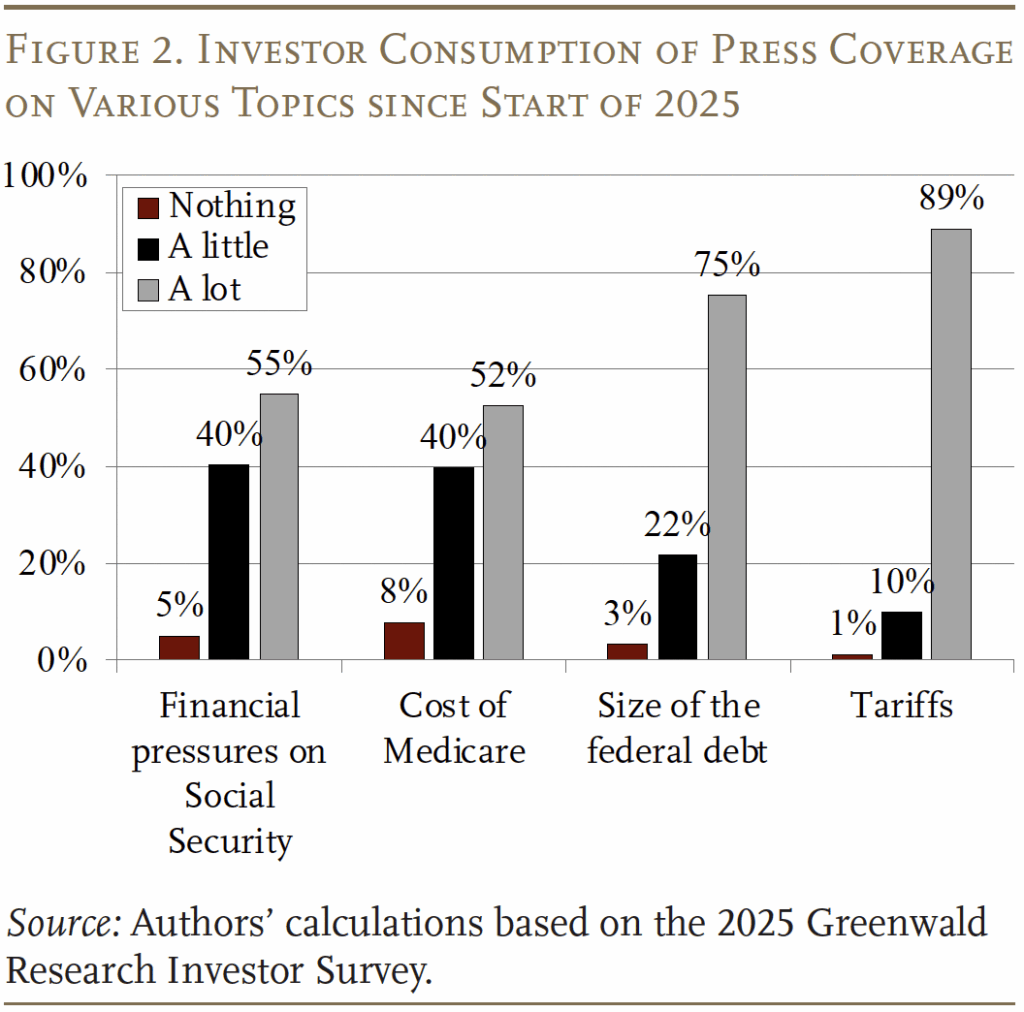

Near-retirees and retirees have also been exposed to a lot of media coverage of policy uncertainty (see Figure 2). Majorities report having seen stories on Social Security’s financial pressures (55 percent), the cost of Medicare (52 percent), the size of the federal debt (75 percent), and tariffs (89 percent).

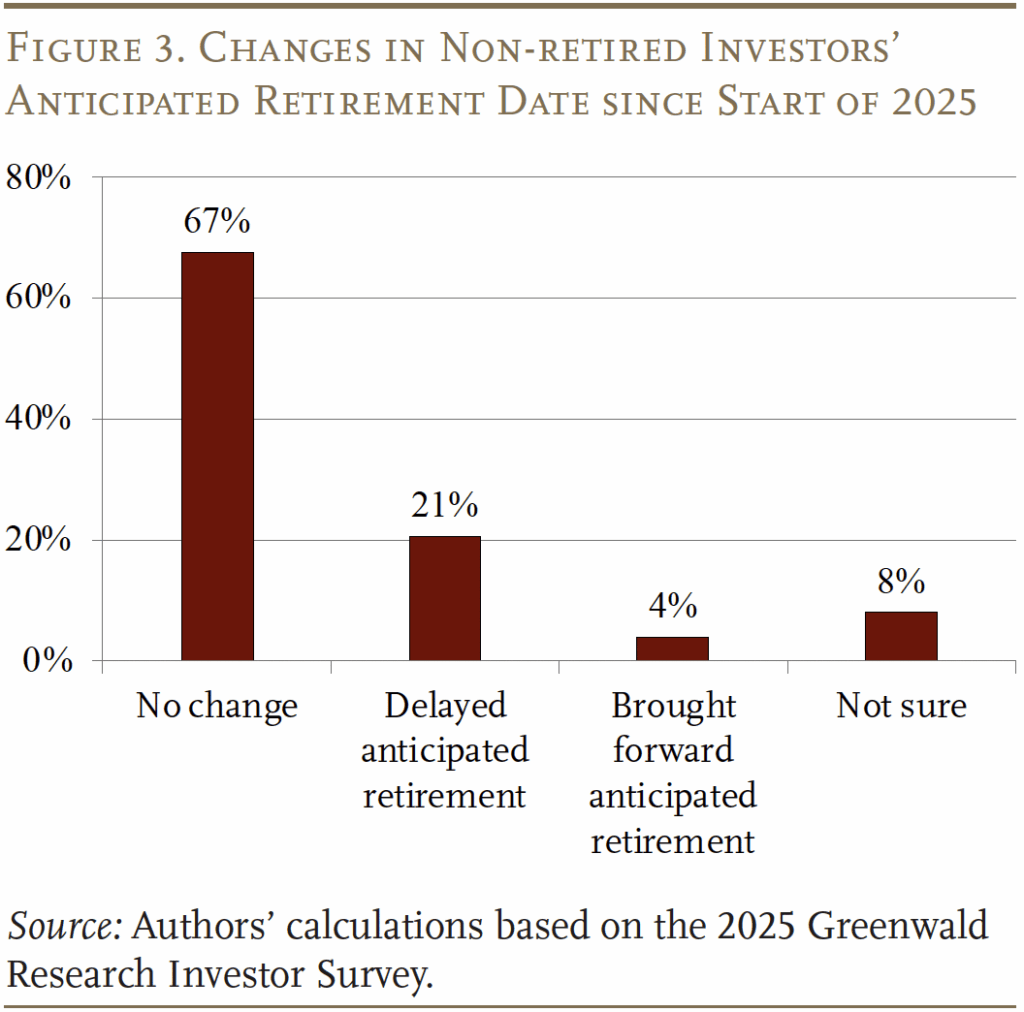

These investors have coped with this unpredictability in myriad ways. While 67 percent of pre-retirees have not changed their anticipated retirement date since the beginning of 2025, 21 percent plan to retire later than before, while only 4 percent plan to retire earlier (see Figure 3).

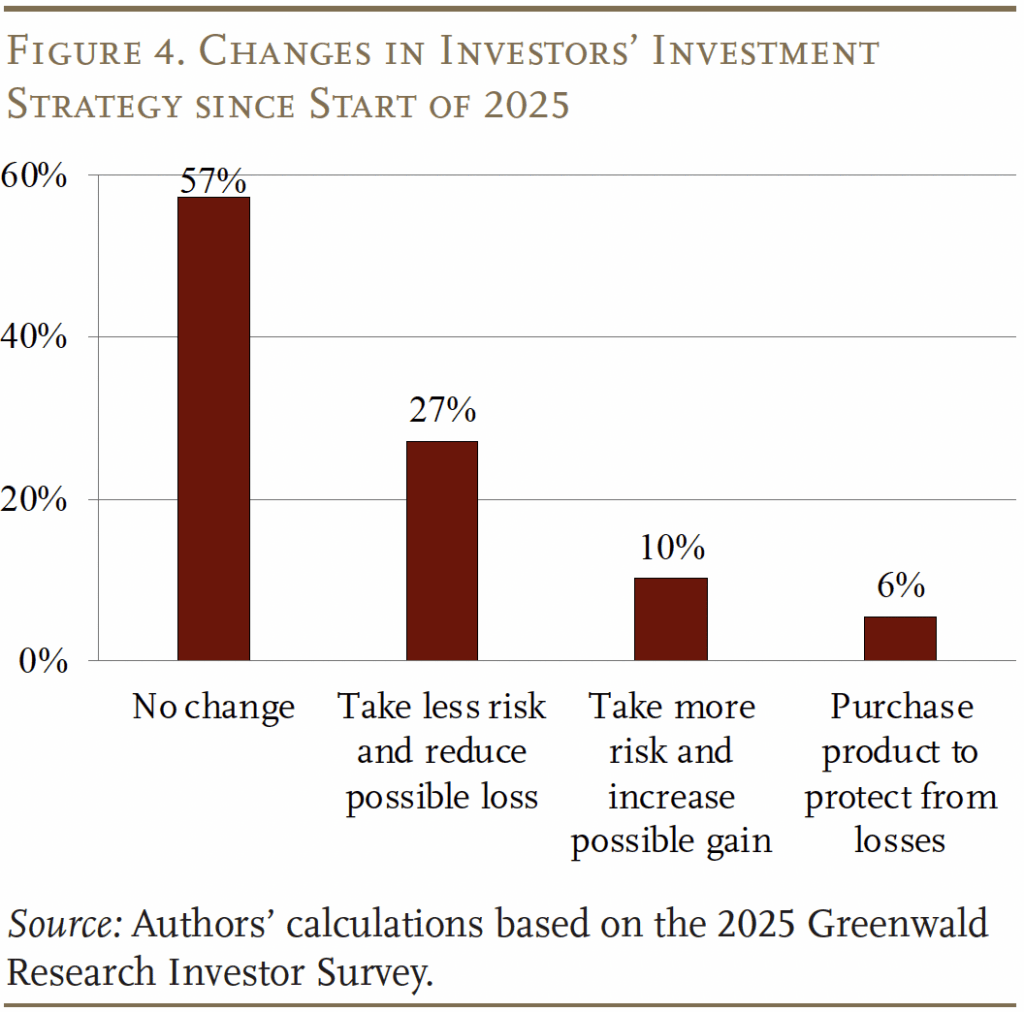

In addition, many respondents say that since the beginning of 2025 they have moved to a more conservative portfolio (27 percent) or bought a product to protect against losses (6 percent), although, as in the case of retirement, most have not made any changes (57 percent) (see Figure 4).

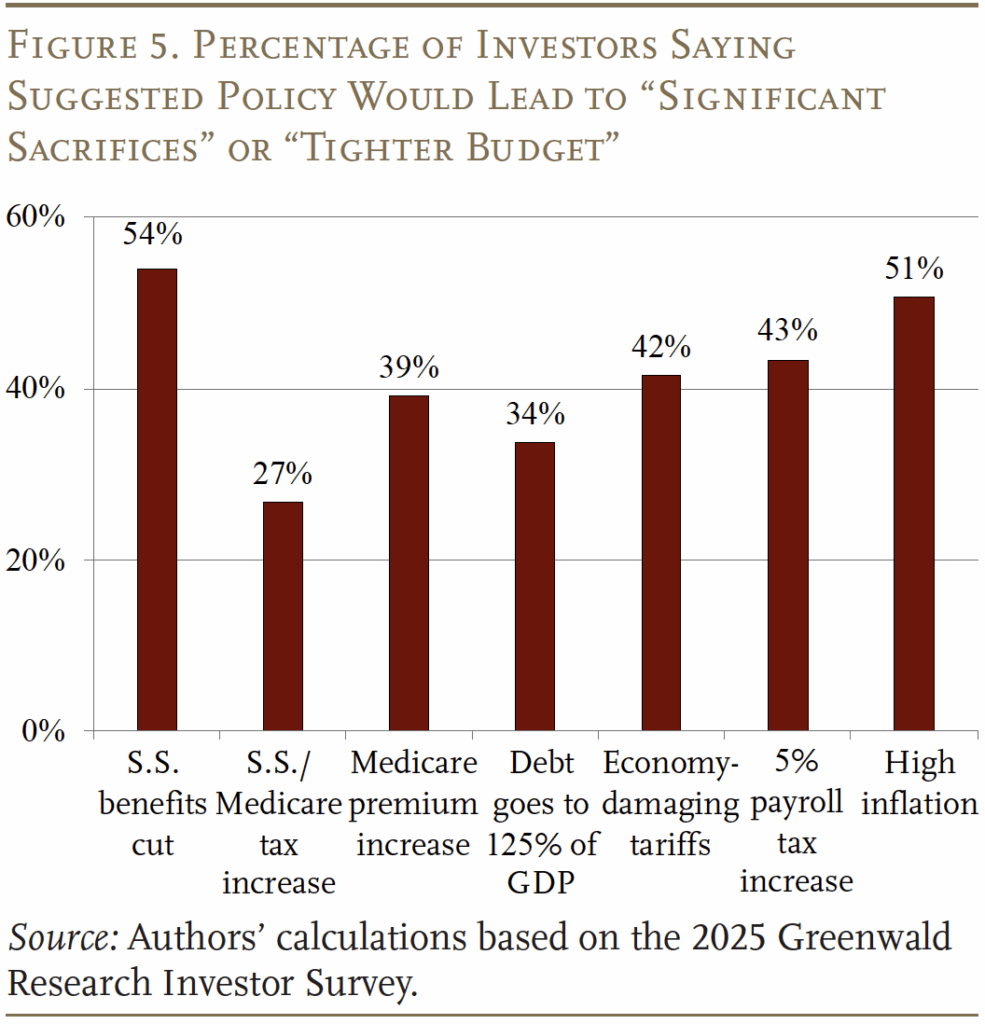

One question is whether the participants’ heightened anxiety is a generalized concern or associated with a specific program or policy. To gauge whether some risks are more important than others, the survey inquired about the hit to respondents’ lifestyles if a battery of different expected policy risks materialized. These negative scenarios, chosen to be plausible given recent history or expert projections, included: inflation hitting 7 percent for three years;25 Medicare premiums increasing by 10 percent per year for three years;26 high and varying tariffs hurting the economy;27 a 5-percentage point increase in the federal income tax rate;28 the federal debt increasing from 100 percent of GDP now to 125 percent in 2035;29 Social Security benefits being cut by 20 percent starting in 2035;30 and payroll taxes increasing by 4 percentage points.31

Views of Social Security Policy Risk

Despite being a relatively wealthy sample, responses indicate that Social Security is the most important policy area for near-retirees and retirees. Fifty-four percent say that a 20-percent cut to Social Security benefits starting in 2035 would entail significant sacrifices or a tighter budget, higher than any other reasonable risk the survey asked about (see Figure 5). Notably, this scenario is less extreme than the current policy trajectory, which envisions a larger cut, sooner – roughly 25 percent in 2033. However, the prospect of one possible solution to Social Security’s problems – raising the payroll tax – does not worry as many respondents – probably because older and retired respondents would have less, or no, exposure to higher payroll taxes. Notably, other than Social Security, the only area where a majority of respondents believe policy is likely to lead to severe changes in their lifestyle is inflation. This finding echoes the media coverage showing Americans deeply concerned with the cost of living.

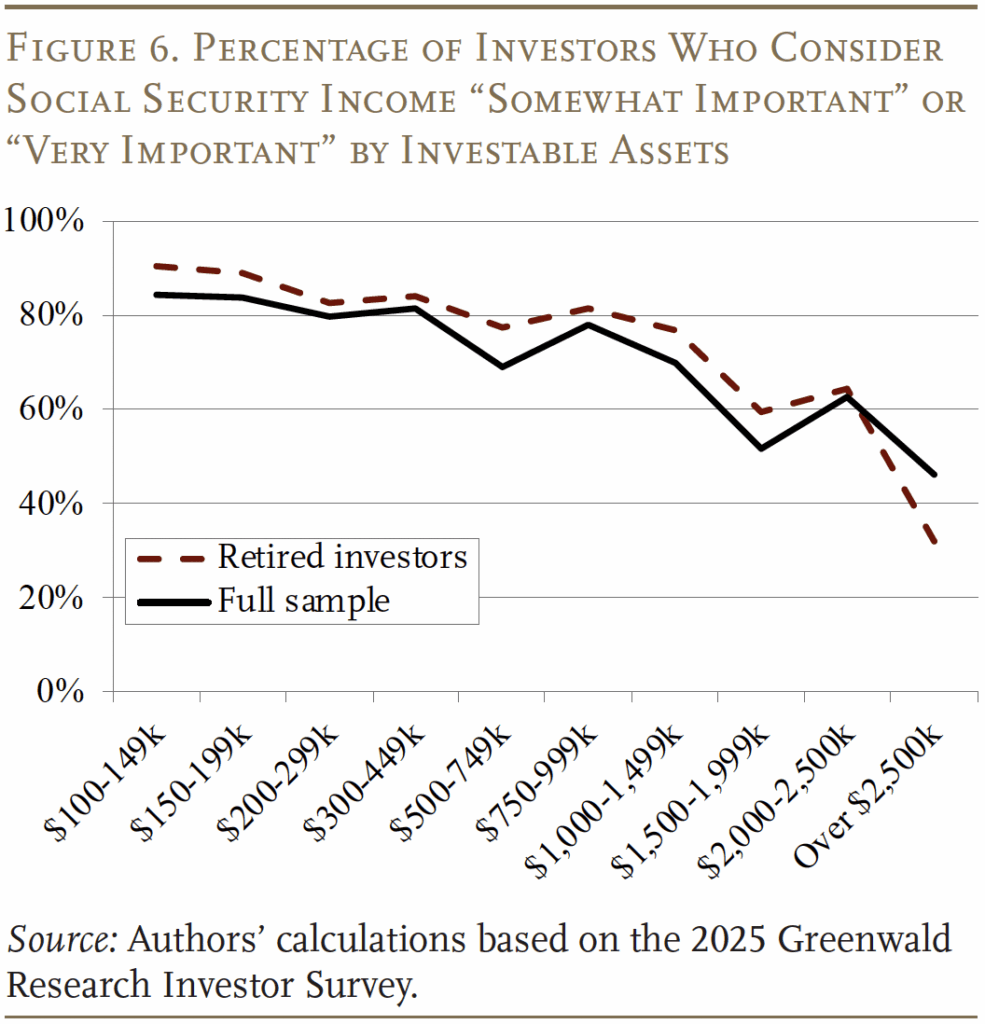

Even though Social Security benefits replace a larger share of lifetime earnings for those with lower earnings, more than half of people in almost every asset bracket say Social Security is somewhat important or very important (see Figure 6). And current retirees, who have the greatest personal experience with Social Security benefits, value Social Security the most.

Consistent with findings from past literature, regression results reveal differing responses to the resolution of Social Security’s financial problems. Indeed, a simple regression – reported in our full study – shows that households with more income/wealth are less likely to envision a “significant sacrifice” in response to a 20-percent cut in Social Security benefits in 2035 or to a 4-percent increase in the payroll tax. The equation controlled for gender, race, and college education.

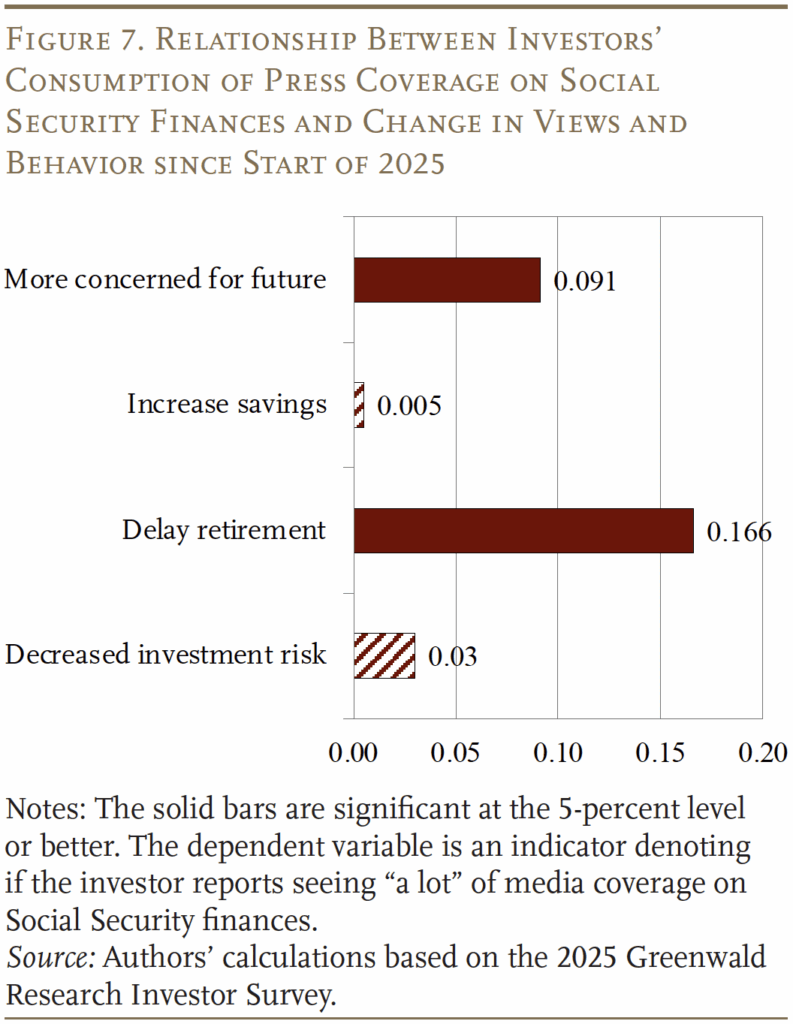

The more complicated regression relates press coverage exposure to policy risks, on the one hand, to various precautionary steps respondents say they have taken since the beginning of 2025, on the other. While the results cover several policy risks, the focus here is on Social Security. Again, these regressions control for various demographic characteristics and economic variables. The results show that the more respondents have heard of Social Security’s financial difficulties, the more concerned they tend to be about their own financial future, and the more likely they are to have decided to delay retirement relative to their pre-2025 plans (see Figure 7). For example, someone who consumes a lot of press coverage on Social Security is 9.1 percentage points more likely to report increased concern for the future compared to someone who consumes little or no press coverage on the program, and 16.6 percentage points more likely to decide to delay their retirement.

Another regression equation estimates the relationship between concern about specific policy adjustments that might happen, on the one hand, and the household’s coping mechanisms, on the other. In the Social Security context, the question is how a household’s concern about a hike in payroll taxes correlates with the precautionary steps taken since the beginning of 2025. The results show that, unlike the more general concern over Social Security’s finances, a contemplated rise in payroll taxes is not correlated with plans to delay retirement. This response is sensible since the payroll tax hike would discourage working longer.32

Overall, the results point to trepidation among near-retiree and retired investors regarding the future of Social Security. Their preferred responses, however, depend on whether the issue is settled through benefit cuts or tax increases: respondents react to Social Security’s general unsettled future but not to tax hikes specifically.

Views of Medicare Policy Risk

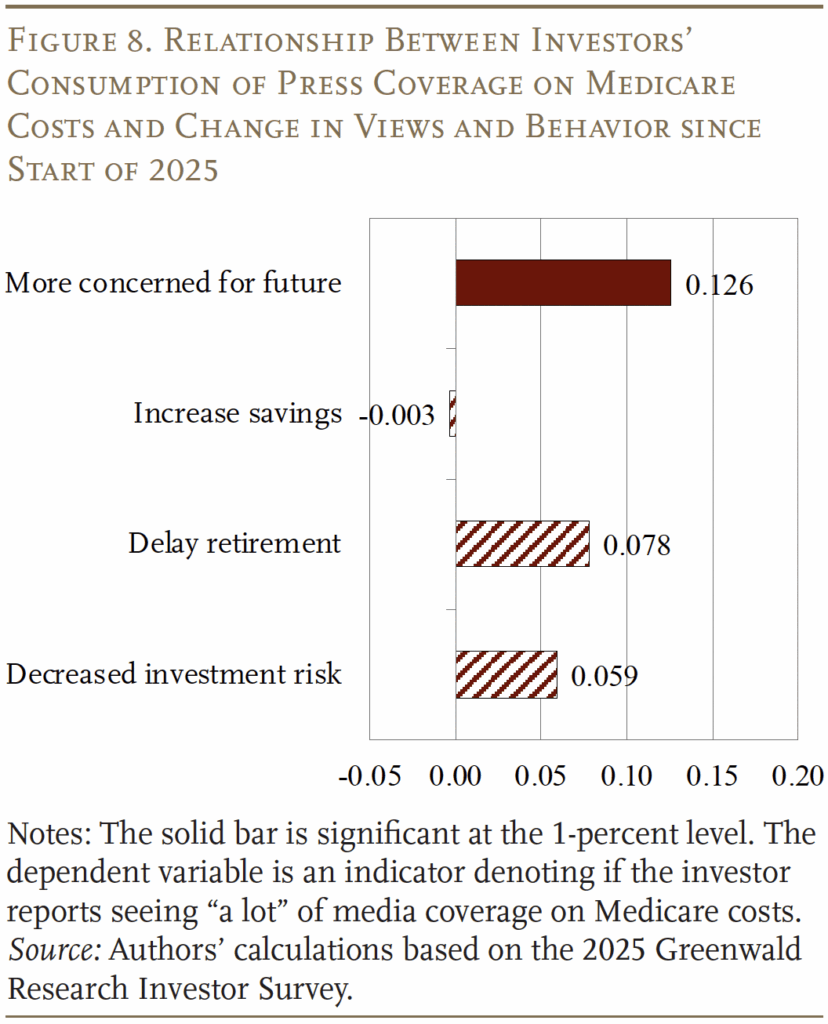

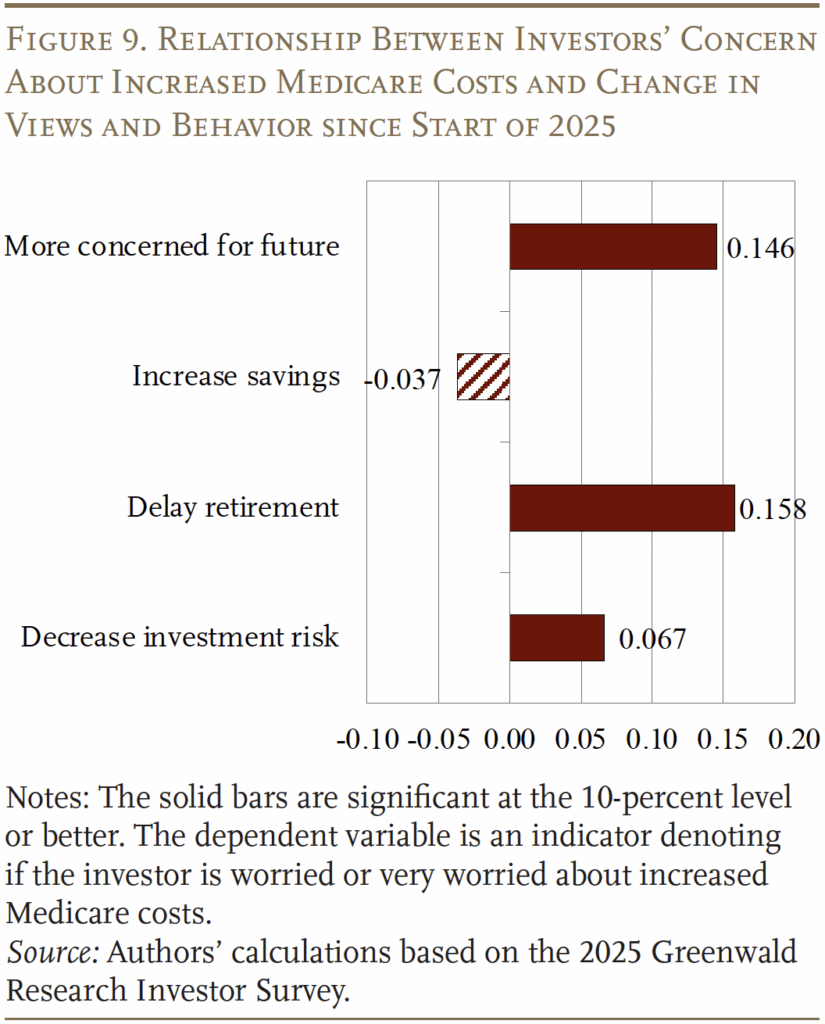

In contrast to Social Security benefit cuts, only 39 percent of respondents say that Medicare premiums rising by 10 percent per year for three years would result in tighter budgets or significant sacrifices (see Figure 5). This smaller share is reasonable since Medicare premiums make up relatively less of the budget for households with over $100,000 in investable assets. Nevertheless, as shown in Figure 8, exposure to information about Medicare cost increases is still associated with general financial concern. In fact, alongside general worries about Social Security’s finances discussed above, the unsustainable growth of Medicare’s costs is the only other policy where having heard a great deal about it is significantly associated with general concern over the individual’s future finances.

The two specific initiatives to address the rising costs in Medicare are raising premiums and increasing cost-sharing. Results presented in Figure 9 show that worry over this development is also associated with worries about the individual’s finances, as well as plans to delay retirement and shift to more conservative investments.

Thus, even though only a minority of respondents believe significant Medicare premium hikes would necessitate severe adjustments to their lifestyle, this policy risk is associated with a meaningful change in individuals’ plans over when to retire and how to invest.

Views of Fiscal Policy Risk

The survey considered two elements of fiscal policy that have been very much in the news – the size of the federal debt generally and the imposition of tariffs. Near-retirees and retirees do not view either policy to be as threatening as Social Security benefit cuts (see Figure 5). Specifically, only 34 percent say an increase in the debt-to-GDP ratio to 125 percent would lead to significant budgetary adjustments for their household, and 42 percent say the same about high and unpredictable tariffs hurting the economy. Similarly, 43 percent would feel significantly impacted by a 5-percentage point increase in their federal income tax rate.

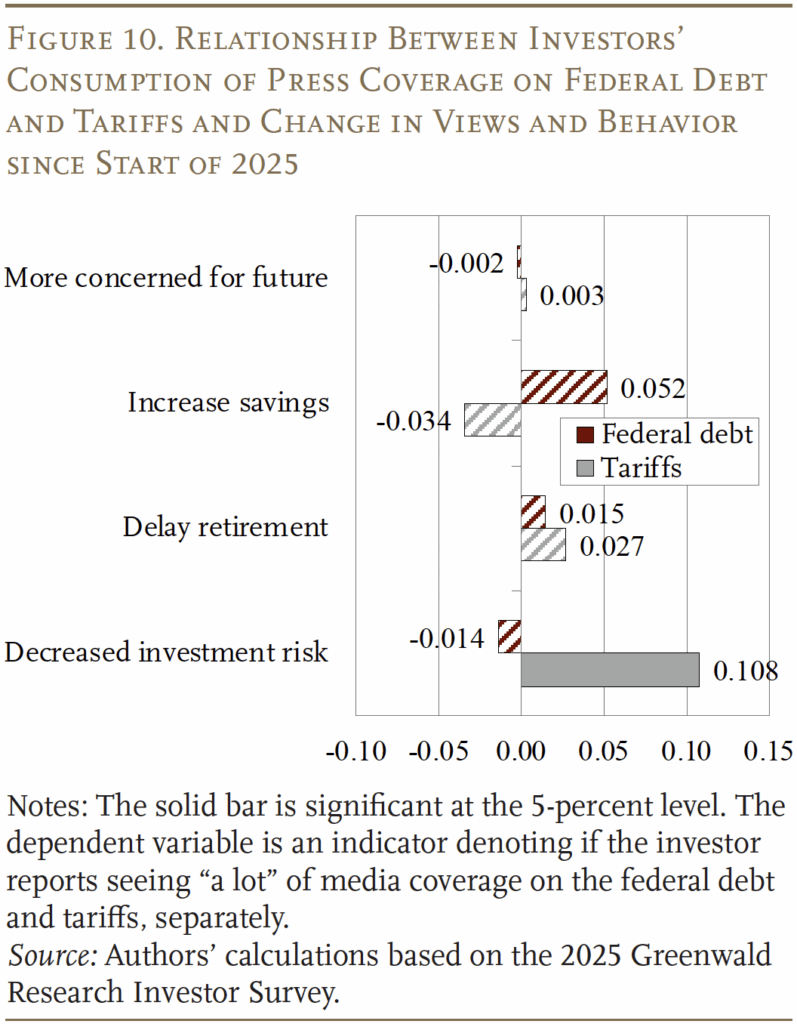

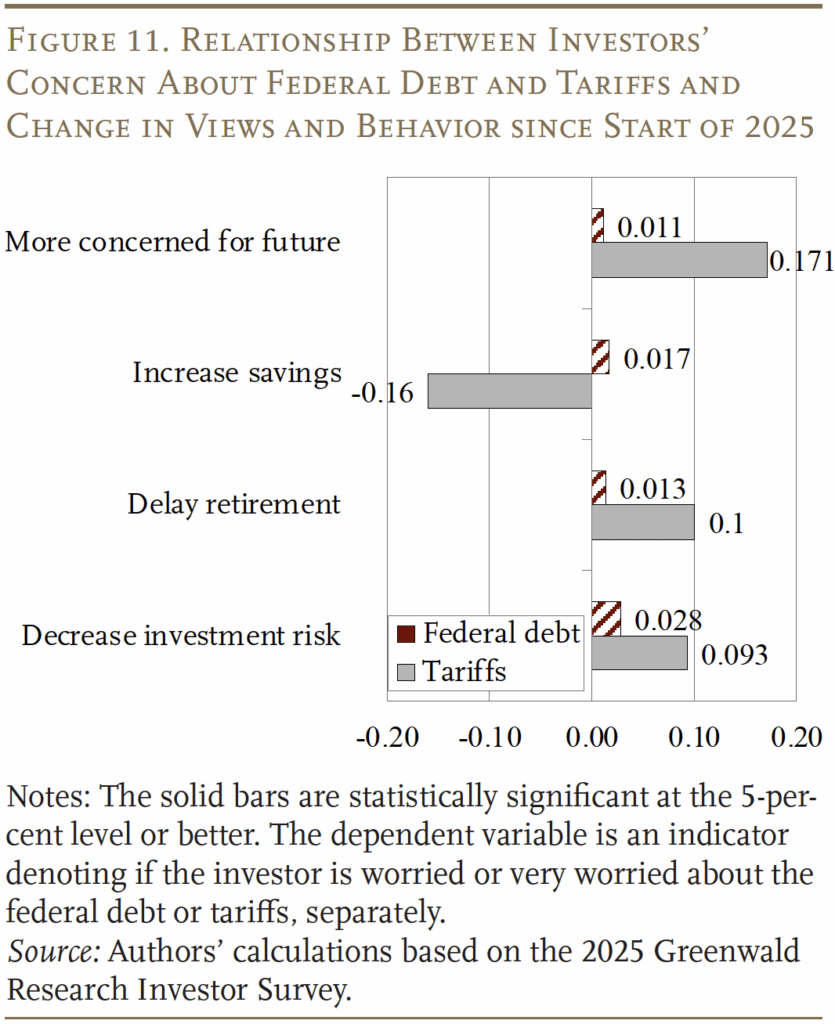

Respondents display no correlation between their general concern for the future and exposure to news about either the federal debt or tariffs, although exposure to news on tariffs is associated with decreased risk-taking in investment (see Figure 10). This lack of response across most dimensions may reflect the fact that such news coverage is nearly ubiquitous. Indeed, the vast majority of respondents say they have seen a lot of coverage of these two issues (see Figure 2). Even though respondents indicate that news about these fiscal events is not creating increased concern, worry over tariffs is strongly correlated with financial worries, plans to delay retirement, and a more conservative investment portfolio in 2025 (see Figure 11 on the next page). Moreover, tariffs are associated with a strong decline in savings, possibly because they drive up current costs.

Overall, the results on fiscal policy point to individuals reacting quite strongly to tariffs, but the overall debt elicits muted responses, maybe because it is a relatively predictable and ponderous quantity.

Conclusion

While policy uncertainty has been much studied, big questions remain about the dramatic uptick in policy risk. The survey results presented here suggest that near-retiree and retiree investors are significantly more concerned since the start of 2025 about their well-being; and they plan delays in retirement and shifts to more conservative investments, and are betting on higher taxes in the future.

Uncertainty about the future of Social Security is the major concern, even for this sample of relatively wealthy households. Of the ways of squaring the circle of Social Security’s finances – benefit cuts or payroll tax hikes – respondents are mostly focused on cuts, since, given their age, they would have little exposure to higher taxes. Aside from Social Security, the only area where a majority of respondents believe policy is likely to lead to severe changes in their lifestyle is inflation – a finding that echoes the media coverage showing Americans deeply concerned with the cost of living.

Overall, the risk that policy poses to near-retirees and retirees seems substantial, imposing considerable costs on households as they take precautionary actions as well as harming the economy. The open question is whether policymakers are capable of taking steps to set policy on a more predictable trajectory.

References

Agarwal, Vikas, Hadiye Aslan, Lixin Huang, and Honglin Ren. 2022. “Political Uncertainty and Household Stock Market Participation.” Journal of Financial and Quantitative Analysis 57(8): 2899-2928.

Alexopolous, Michelle and Jon Cohen. 2015. “The Power of Print: Uncertainty Shocks, Markets, and the Economy.” International Review of Economics & Finance 40: 8-28.

Baker, Scott R., Nichola Bloom, and Steven J. Davis. 2016. “Measuring Economic Policy Uncertainty.” The Quarterly Journal of Economics 131(4): 1593-1636.

Basu, Susanto and Brent Bundick. 2017. “Uncertainty Shocks in a Model of Effective Demand.” Econometrica 85(3): 937-958.

Bazzoli, Gloria J., Richard C. Lindrooth, Romana Hasnain-Wynia, and Jack Needleman. 2004. “The Balanced Budget Act of 1997 and U.S. Hospital Operations.” Inquiry 41(4): 401-417.

Boudoukh, Jacob, Ronen Feldman, Shimon Kogan, and Matthew Richardson. 2013. “Which News Moves Stock Prices? A Textual Analysis.” Working Paper 18725. Cambridge, MA: National Bureau of Economic Research.

Congressional Budget Office. 2025. Data on the Long-Term Budget Outlook: 2026-2056. Washington, DC.

Dafny, Leemore S. 2005. “How Do Hospitals Respond to Price Changes?” American Economic Review 95(5): 1525-1547.

Delavande, Adeline and Susann Rohwedder. 2017. “Changes in Spending and Labor Supply in Response to a Social Security Benefit Cut: Evidence from Stated Choice Data.” Journal of the Economics of Ageing 10: 34-50.

Federal Reserve Bank of St. Louis. 2025. “Inflation, Consumer Prices for the United States (FPCPITOTLZGUSA).”

Fernandez-Villaverde, Jesus, Pablo Guerron-Quintana, Keith Kuester, and Juan Rubio-Ramirez. 2015. “Fiscal Volatility Shocks and Economic Activity.” American Economic Review 105(11): 3352-3384.

Gabor-Toth, Eniko and Dimitris Georgarakos. 2018. “Economic Policy Uncertainty and Stock Market Participation.” CFS Working Paper Series 590. Frankfurt, Germany: Center for Financial Studies.

He, Daifeng and Jennifer M. Mellor. 2012. “Hospital Volume Responses to Medicare’s Outpatient Prospective Payment System: Evidence from Florida.” Journal of Health Economics 31(5): 730-743.

Leduc, Sylvain and Zheng Liu. 2016. “Uncertainty Shocks are Aggregate Demand Shocks.” Journal of Monetary Economics 82: 20-35.

Luttmer, Erzo F.P. and Andrew A. Samwick. 2018. “The Welfare Cost of Perceived Policy Uncertainty: Evidence from Social Security.” American Economic Review 108(2): 275-307.

Munnell, Alicia H. 2025. “Medicare Finances: A Perspective on the 2025 Trustees Report.” Issue in Brief 25-16. Chestnut Hill, MA: Center for Retirement Research at Boston College.

Munnell, Alicia H. and Gal Wettstein. 2026. “How Policy Risks Affect Retirement Planning.” Special Report. Chestnut Hill, MA: Center for Retirement Research at Boston College.

Neuman, Tricia, Juliette Cubanski, and Meredith Freed. 2022. “Monthly Part B Premiums and Annual Percentage Increases.” San Francisco, CA: Kaiser Family Foundation.

Parkin, David, Alistair McGuire, and Brian Yule. 1987. “Aggregate Health Care Expenditures and National Income: Is Health Care a Luxury Good?” Journal of Health Economics 8(2): 109-127.

Quinby, Laura D. and Gal Wettstein. 2021. “Does Media Coverage of the Social Security Trust Fund Affect Claiming, Saving, and Benefit Expectations?” Working Paper 2021-10. Chestnut Hill, MA: Center for Retirement Research at Boston College.

Rudowitz, Robin, Jennifer Tolbert, Alice Burns, Elizabeth Hinton, Anna Mudumala, Priya Chidambaram, and Maiss Mohamed. 2025. “Medicaid 101.” In KFF’s Health Policy 101, edited by Drew Altman, 1-27. San Francisco, CA: KFF.

Shen, Yu-Chu and Vivian Y. Wu. 2013. “Reductions in Medicare Payments and Patient Outcomes: An Analysis of 5 Leading Medicare Conditions.” Medical Care 51(11): 970-977.

Shoven, John B., Sita Slavov, and John G. Watson. 2021. “How Does Social Security Reform Indecision Affect Younger Cohorts?” Working Paper 28850. Cambridge, MA: National Bureau of Economic Research.

Skopec, Laura, Joshua Aarons, and Stephen Zuckerman. 2019. “Did Medicare Advantage Payment Cuts Affect Beneficiary Access and Affordability?” American Journal of Managed Care 25(9): e261-e266.

The Tax Foundation. 2025. “Historical US Federal Individual Income Tax Rates & Brackets, 1862-2025.”

U.S. Social Security Administration. 2025. The Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds. Washington, DC: U.S. Government Printing Office.

White, Chapin and Tracy Yee. 2013. “When Medicare Cuts Hospital Prices, Seniors Use Less Inpatient Care.” Health Affairs 32(10): 1789-1795.

Endnotes

- Munnell and Wettstein (2026). ↩︎

- For example, Boudoukh et al. (2013) and Alexopolous and Cohen (2015). ↩︎

- Baker, Bloom, and Davis (2016). ↩︎

- Fernandez et al. (2015). ↩︎

- Agarwal et al. (2022) use a large set of U.S. gubernatorial elections in a similar way. ↩︎

- Leduc and Liu (2016). ↩︎

- Baker et al. (2016). ↩︎

- Theoretical modeling demonstrates how policy uncertainty can lead to economic contraction, particularly when the central bank’s monetary policy is at the “zero lower bound,” which precludes further rate reductions (see Fernandez et al. (2015) and Basu and Bundick (2017)). ↩︎

- Boudoukh et al. (2013); Alexopolous and Cohen (2015); Fernandez et al. (2015); and Baker, Bloom, and Davis (2016). ↩︎

- Leduc and Liu (2016). ↩︎

- U.S. Social Security Administration (2025). ↩︎

- Gabor-Toth and Georgarakos (2018) and Agarwal et al. (2022). ↩︎

- Shoven, Slavov, and Watson (2021). ↩︎

- Delavande and Rohwedder (2017). ↩︎

- Quinby and Wettstein (2021). ↩︎

- Delavande and Rohwedder (2017). ↩︎

- Quinby and Wettstein (2021). ↩︎

- Luttmer and Samwick (2018) and Shoven, Slavov, and Watson (2021). ↩︎

- Rudowitz et al. (2025). ↩︎

- While Medicare Part A does have a trust fund, it is small and mostly irrelevant to the sustainability of the Medicare program as a whole (Munnell 2025). ↩︎

- Dafny (2005) and White and Yee (2013). However, see Bazzoli et al. (2004) for conflicting results; and He and Mellor (2012) find that the impact of Medicare cuts on hospitals depends on the share of Medicare patients they serve. ↩︎

- Shen and Wu (2013). ↩︎

- Skopec, Aarons, and Zuckerman (2019). ↩︎

- Most evidence suggests that healthcare is a necessity, not a luxury good (e.g., Parkin, McGuire, and Yule 1987). ↩︎

- Inflation topped 7 percent annually between 1978 and 1981 (Federal Reserve Bank of St. Louis 2025). ↩︎

- Medicare premiums increased by more than 10 percent annually seven times between 2002 and 2022 (Neuman, Cubanski, and Freed 2022). ↩︎

- High and varying tariffs have already been instituted and changed multiple times since April 2025. ↩︎

- The top income tax rate rose 4.6 percentage points, from 35.0 to 39.6 percent, as recently as 2012-2013 (The Tax Foundation 2025). ↩︎

- The federal debt, which was 99 percent of GDP in 2025, is projected to increase to 118 percent in 2035 and 142 percent in 2045 (Congressional Budget Office 2026). ↩︎

- Unless current law is changed, the Social Security actuaries project that retirement benefits will be cut across the board by about 25 percent in 2033 (U.S. Social Security Administration 2025). ↩︎

- The combined actuarial deficit for Social Security’s retirement and disability insurance programs was 3.82 percent of payroll over the 75-year projection period in 2025 (U.S. Social Security Administration 2025). ↩︎

- This regression includes only respondents who are not yet retired. ↩︎

Munnell, Alicia H. and Gal Wettstein. 2026. "How Policy Risks Affect Retirement Planning for Older Americans" Issue in Brief 26-6. Chestnut Hill, MA: Center for Retirement Research at Boston College.